|

Please note the above is a suggested fund allocation only and not as an investment advice / recommendation.

To qualify as emergency money, it should meet the following criteria:

Liquid, i.e., it should be available when required Safe, which means this money cannot be invested in highly volatile instruments. Low correlation with other assets – Investors should not risk it and try to earn high returns.

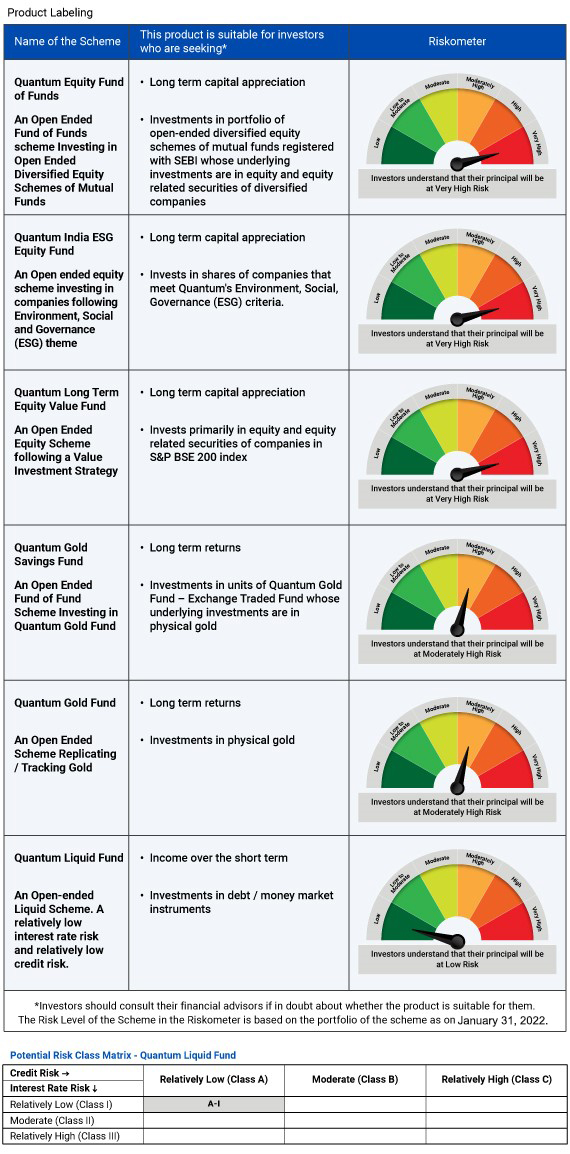

Ideally, investors need to park this money in a safe place like a bank account or a Quantum Liquid Fund scheme that qualifies as a Safety or the Foundation block of their portfolio.

Advantages of investing in Quantum Liquid Fund

Option to withdraw (up to Rs.50K) whenever investors need it. Works on the 'SLR' principle, prioritizing safety and liquidity over returns. Portfolio comprising of AAA/A1+ rated PFI/ PSU securities and government securities with a duration not exceeding 91 days, Does NOT invest in Private Papers / Corporate Instruments Relatively low interest rate risk (classified as A-1 as per the PRC matrix).

Risk Reducing Block:

Investors can capitalize on Gold’s risk-reducing characteristics and allocate 20% of their portfolio to the yellow metal through innovative forms such as Quantum Gold Fund ETF and Quantum Gold Savings Fund. Gold generally tends to perform better when equities are under stress thus helping your investors lower downside risks.

Advantages of investing in Quantum Gold Fund

Ease of investing in Quantum Gold Fund (ETF) through a DEMAT account Backed by pure gold of 99.5% finesse sourced from LBMA accredited refiner All gold bars held by the fund go through an independent purity test Option to invest in Quantum Gold Savings Fund through an SIP (Systematic Investment Plan) of as low as Rs. 500

Growth Block – Allocate 80% to an equity bucket:

Even within equity as an asset class, investors need to diversify across market capitalization such as large–cap, small-cap, mid-cap, etc. As different investment styles and market cap perform differently as per different cycles. For instance, the year 2021 saw value investment style outperforming the growth style of investment. During the Covid-19 induced market collapse, value fund managers got a great opportunity to acquire high-quality stocks at attractive valuations, thereby generating risk-adjusted returns when markets recovered. Last year also saw mid and small cap funds performing well and though large cap funds showcased relatively lesser returns, they performed on par with relatively less volatility over the longer period.

Therefore, an equity portfolio should also be diversified as per investment styles and market cap.

Diversify the balance 80% across an equity bucket that is market cap, sector, or style agnostic comprising of Quantum Long Term Equity Value Fund, Quantum Equity Fund of Funds and Quantum India ESG Equity Fund.

Quantum Long Term Equity Value Fund – Salient Features

15-year track record following the Value style of investing Long term believer of India's growth story Bottom-up stock selection comprising of stocks tuned to grow with market recovery Potential to limit downside risks

Quantum India ESG Equity Fund – Salient Features

Value & sector agnostic diversified portfolio One of the first ESG fund launched in India incorporating Environmental, Social and Governance parameters Does not rely on third party research, uses in-house comprehensive & robust proprietary framework Potential to protect returns in down markets

Quantum Equity Fund of Funds – Salient Features

Underlying investment is in third-party Funds with performance across market cycles Benefit of indexation for long-term investment Ease of tracking just one folio and one NAV Robust qualitative and quantitative research Periodical review meetings of chosen funds

Thus, by using one asset allocation solution with three underlying assets in Equity, Debt and Gold, you can be on their way to overcoming market uncertainty, cope better with inflation and achieve their long-term financial goals.

|