In the current market context too the 12 20 80 asset allocation framework is ideal to capitalize on the upside potential of Indian equity markets

BFSI Industry Interview

Mr. Chirag Mehta has been elevated to the position of Chief Investment Officer of Quantum Asset Management Company with effect from April 01, 2022. Chirag has been serving as Senior Manager, Alternative Investments. He joined Quantum in 2006 and has more than 18 years of cumulative experience in managing commodities and specializing in the field of alternative investment strategies. He has been the fund manager of Quantum Gold Savings Fund, Quantum Equity Fund of Funds, Quantum Multi Asset Fund of Funds, and Quantum India ESG Equity Fund. Chirag has been formerly ranked as the 4th best Fund Manager in the world under the age of 40 by Citywire in 2017. He is a qualified CAIA (Chartered Alternative Investment Analyst) and has also completed his Master’s in Management Studies in Finance.

What are your views on the global economy, especially inflation risks and the impact of US interest rate hikes on global equity and debt markets?

In response to multi-decade high inflation in the developed world, which is partly due to the easy money policies implemented post the pandemic and partly due to the supply disruptions of the Russia-Ukraine war, we have seen aggressive monetary tightening by global central banks in 2022, abruptly taking rates up from zero or sub-zero to levels not seen in almost a decade and a half. This is bound to a) shock the economy which has been banking on lower interest rates to sustain the growth momentum, and b) threaten the unsustainable debt that exists today. An economic slowdown or recession in 2023 seems inevitable now, which will be negative for equity markets. A debt crisis also cannot be ruled out at this point considering that inflation is still far from central bank targets, and they seem focussed on not letting high inflation become entrenched. The war and resulting energy crisis continue to complicate the inflation story.

The question now is to what extent are central bankers prepared to sacrifice growth and financial stability? Till clarity emerges on that front, global financial markets will continue to be pushed and pulled in either direction, with a downward bias. A sustainable move upwards will be seen when either the global economy manages to land softly, which is less probable, or the interest rate cycle turns to support deteriorating growth, which seems more likely. The latter could set on a “risk on” rally until then brace for some volatility.

What are your views on Indian equities from a long-term perspective?

Domestic demand coming back in a big way post-pandemic, favourable demographics, structural drivers like digitization and formalization, supportive government policy measures like PLI, political stability, moderate inflation, and an uptick in equity savings have set the stage for a cyclical recovery which is apparent in revival in real estate, pick up in IT hiring, resilient corporate earnings, strong tax collections, higher Capex and credit growth.

To make things sweeter, we are relatively better placed compared to other emerging and developed economies on the growth and inflation fronts, which should help us attract foreign investment flows.

India (currently the world’s largest democracy and fifth largest economy) is on course for a real rate of growth of > 6.0% p.a. in GDP and nominal growth of 11% to 12% p.a. - which has been the pillar for resilient long-term performance over last 20-30 years which looks set to continue for at least another decade or two.

How should investors approach this market given the risk factors?

Despite India’s long-term growth story being intact, equity markets are vulnerable to external macroeconomic risks like a global slowdown, relative valuation correction, or on account of geopolitical tensions. Diversification of the portfolio to include other low-correlation asset classes is thus imperative. Gold has historically done well in times of economic or geopolitical turmoil when equity markets took a beating, making it an ideal asset class to diversify the current macroeconomic risks. A 20-80 gold-equity asset allocation along with an emergency corpus can be a good starting point for most investors.

Please describe in brief your 12 - 20 - 80 asset allocation strategy for the benefit of retail investors and mutual fund distributors. How will the asset allocation strategy benefit investors in the context of the current economic / market context and in the long term?

Economies go through ups and downs and these often are unforeseeable. Assets in our portfolio, due to their differing risk and return characteristics, respond differently to these ups and downs. For instance, equities run up when the economy is doing well; and gold tends to shine when the economy is down in the dumps.

In essence, because it is difficult to predict the future of the economy, it is also difficult to determine the resulting best-performing asset class. That's where asset allocation and diversification come in handy

Asset allocation is a time-tested approach to portfolio management. It means spreading your investments among multiple asset classes.

In the 12-20-80 asset allocation strategy, we suggest that investors allocate the bulk of their money (80%) to a diversified equity portfolio to benefit from the growth and capital appreciation offered by Indian equities over the long term, while also keeping 12 months (this can be 24 or 36 months as suitable) of emergency funds handy, and 20% allocation to portfolio diversifier gold to stabilize the equity market ups and downs.

By investing in more than one asset category, you'll reduce the risk that you'll lose money and your portfolio's overall investment returns will have a smoother ride. If one asset category's investment return falls, you'll be able to counteract your losses in that asset category with better investment returns in another asset category.

In the current market context too, the 12-20-80 asset allocation framework is ideal to capitalize on the upside potential of Indian equity markets while being able to persist amid the uncertainty and volatility created by higher inflation, tighter monetary policy, global economic slowdown, etc. with the help of back-up cash, which ensures you don’t get pushed into redeeming your equity investments to meet liquidity needs, and gold which with its generally a negative correlation to equities can limit portfolio losses when equities falter in the recessionary environment.

Please explain the rationale of the 20 – 80 asset allocation between gold and equit?

Based on the past performance, Gold generally has an inverse relationship with risk assets like stocks and often negatively correlates with a strong global economy. It has historically been an effective portfolio diversification tool in times of economic, health, or geopolitical crises. If we recap, gold gave positive returns in 2001, 2008, 2011, and 2020 domestic equities corrected sharply.

And now as we step into 2023 gold remains relevant even amid higher interest rates and a stronger dollar as global inflation is at multi-decade highs, the global economy is set to slow down and a major geopolitical crisis plays out, all hurting risk appetites and in turn risk assets.

This mix of competing for macroeconomic and geopolitical factors and their unpredictable impact on financial markets isn't special to the last few years. It's the way things have always been and will continue to be. Yet investors time and again rush to gold in times of stress or crisis only to discount the precious metal when the dust settles, unappreciative of the always-lingering risks and gold’s ability to thrive amid those.

A 20-80 gold-equity portfolio has potential to generate reasonable long-term returns while levelling the ups and downs, making it an ideal asset allocation for long-term investors.

What type of funds should form the core of the equity portfolio in this strategy?

Equity is an inflation-beating asset class and is ideal for generating wealth in the long term. One can allocate 80% of a portfolio to a diversified equity portfolio.

If you choose to build your portfolio in Actively Managed Funds, you can diversify using 70:15:15 allocation with three equity funds - Quantum Long Term Equity Value Fund (15%), Quantum India ESG Equity Fund (15%), and Quantum Equity Fund of Funds (70%).

For passive investing, you can allocate 85% in the Quantum Nifty 50 ETF Fund of Fund and 15% in the Quantum India ESG Equity Fund.

How can investors or mutual fund distributors construct a portfolio with Quantum MF schemes to implement the 12 - 20 - 80 asset allocation strategy? Please provide your general guidance to investors / MFDs?

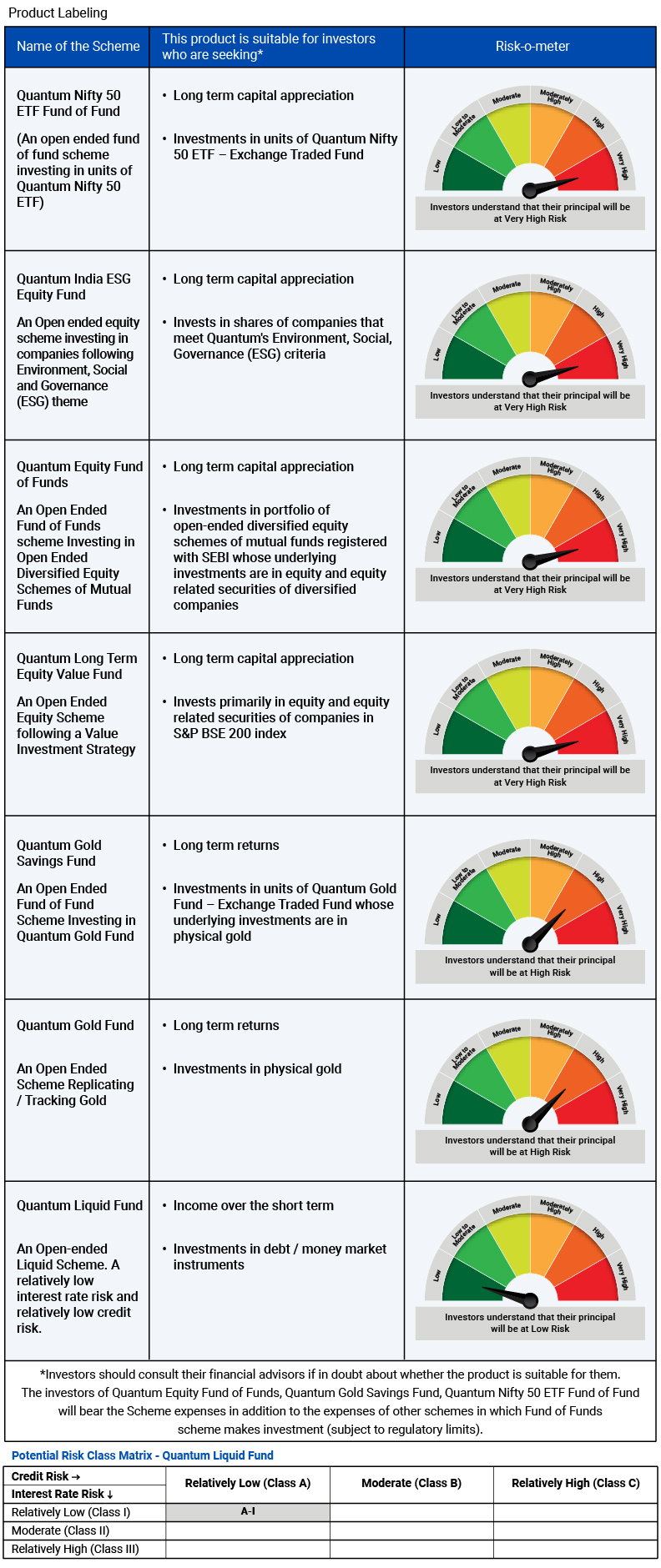

To start with, before you can begin investing in any asset class, you should keep a financial backup or “Emergency Money” ready to see you through 12 months of expenses. Ideally, park this money in a safe place like a bank account or a Liquid Fund scheme such as the Quantum Liquid Fund that offers you the option to redeem (up to Rs.50K) whenever you need it. Since this fund takes minimal credit risk and has a portfolio of AAA/A1+ rated PSU bonds and high-quality government securities with a duration not exceeding 91 days, it has a relatively low-interest rate risk (classified as A-1 as per the PRC matrix). This qualifies as a Safety or the Foundation block of your portfolio.

After setting aside 12 months of safe money, whatever money is left could be split between 80% to Equities and 20% to Gold. When you look at investing 20% in gold, you should ideally choose efficient forms like the gold fund of funds or gold ETFs. This helps negate any worry about its purity, price, or storage hassles as against physical gold which has pricing markups and locker charges.

Quantum Gold Fund ETF is backed by pure Gold of 99.5% finesse. As a step ahead, the fund also undertakes regular independent purity tests of all gold bars. Generally, gold has an inverse relationship with equities and performs better when equity mutual fund performance is under stress and forms an ideal portfolio diversifier. Thus, Gold forms your Risk Diversifying Block.

Finally, a majority portion goes to the Growth block where one invests 80% to an equity bucket that is diversified across styles of equity management, market cap segments, and strategies.

When valuations appear elevated and there is uncertainty in the market, you can reduce downside risk with a portfolio that is at a discount to its intrinsic value based on the historical average. Such a fund is our flagship fund that has a big track record of 15 years. 15% of your equity portfolio can be in the Quantum Long Term Equity value fund that is based on the belief of India’s long-term growth potential

Then consider allocating another 15% to the ESG mutual fund that incorporates the three non-financial parameters of the environment, social, and governance which have a material impact on the future of earnings potential and valuation, making them important considerations for investors. Invest in Quantum India ESG Equity Fund, one of the earliest funds in the ESG space that has showcased resilience even during Covid-induced economic deceleration. The fund uses its own proprietary ESG scoring methodology developed through years of research in the ESG space.

Finally, a greater chunk of your portfolio (approximately 70%) can be invested in Quantum Equity Fund of Funds which simplifies your equity mutual fund selection needs by investing in 5-10 well-researched diversified funds of third-party equity mutual funds.

If you wish to opt for the passive investing route, you can allocate 85% of equity allocation to the Quantum Nifty 50 ETF Fund of Fund and 15% to the Quantum India ESG Equity Fund.

* Investors will bear the recurring expenses of the Scheme in addition to the expenses of Quantum Nifty 50 ETF.

The data in this presentation are meant for general reading purpose only and are not meant to serve as a professional guide/investment advice for the readers. This presentation has been prepared on the basis of publicly available information, internally developed data and other sources believed to be reliable. Whilst no action has been suggested or offered based upon the information provided herein, due care has been taken to endeavour that the facts are accurate and reasonable as on date. Quantum AMC shall make modifications and alterations to the performance and related data from time to time as may be required as per SEBI Mutual Fund Regulations. Readers are advised to seek independent professional advice and arrive at an informed investment decision before making any investment. None of the Sponsors, the Investment Manager, the Trustee, their respective Directors, Employees, Affiliates or Representatives shall be liable for any direct, indirect, special, incidental, consequential, punitive or exemplary damages, including lost profits arising in any way from the data/information/opinions contained in this presentation. The Quantum AMC shall make modifications and alterations to the performance and related data from time to time as may be required.

Please visit - www.QuantumMF.com to read scheme specific risk factors. Investors in the Scheme are not being offered a guaranteed or assured rate of return and there can be no assurance that the schemes objective will be achieved and the NAV of the scheme may go up and down depending upon the factors and forces affecting securities market. Investment in mutual fund units involves investment risk such as trading volumes, settlement risk, liquidity risk, default risk including possible loss of capital. Past performance of the sponsor / AMC / Mutual Fund does not indicate the future performance of the Scheme. Statutory Details: Quantum Mutual Fund (the Fund) has been constituted as a Trust under the Indian Trusts Act, 1882. Sponsor: Quantum Advisors Private Limited. (liability of Sponsor limited to Rs. 1,00,000/-). Trustee: Quantum Trustee Company Private Limited. Investment Manager: Quantum Asset Management Company Private Limited. The Sponsor, Trustee and Investment Manager are incorporated under the Companies Act, 1956.

Mutual fund investments are subject to market risks, read all scheme related documents carefully.

Recent Interviews

-

In Conversation by Advisorkhoj with Ms Saloni Kapadia Fund Manager The Wealth Company Mutual Fund

Jul 23, 2026

-

In conversation with Mr Gautam Kaul Senior Fund Manager Fixed Income with Bandhan Mutual Fund

Jul 23, 2026

-

Partner Connect by Advisorkhoj with Mr Suresh Royal Rupee MFS Pvt Ltd Tirupathi

Jul 20, 2026

-

In Conversation with Mr Ritesh Pathak Deputy CBO Retail Sales & Passive with Motilal Oswal MF

Jul 13, 2026

-

Partner Connect by Advisorkhoj with Mr Ramu Chellimilla & Mr B G Srinivas Invictus FinServ LLP Secunderabad

Jul 1, 2026

Fund News

-

DSP Mutual Fund launches DSP Nifty 10 Yr Benchmark G SEC ETF

Aug 10, 2026 by Advisorkhoj Team

-

Bandhan Mutual Fund launches Bandhan Contra Fund

Aug 10, 2026 by Advisorkhoj Team

-

Aditya Birla Sun Life Mutual Fund SIF launches Apex Equity Long Short Fund

Aug 10, 2026 by Advisorkhoj Team

-

Aditya Birla Sun Life Mutual Fund SIF launches Apex Equity Ex Top 100 Long Short Fund

Aug 10, 2026 by Advisorkhoj Team

-

SBI Mutual Fund SIF launches Magnum Equity Ex Top 100 Long Short Fund

Aug 7, 2026 by Advisorkhoj Team