We follow a blended approach for Sundaram Large and Midcap Fund

BFSI Industry Interview

Krishna Kumar joined Sundaram Asset Management Company in 2003 as the Head of Research. During his tenure he has handled various roles within Fund Management and was elevated to the post of Chief Investment Officer, Equities in April 2015. He brings over 20 years of experience in Indian equity markets.

Krishna Kumar assumed management of Sundaram Mid Cap in 2012 and also manages Sundaram Large & Mid Cap, Sundaram Small Cap, Sundaram Diversified Equity, Sundaram Micro cap Series III-IV & VIII-XII & XIV-XVII among others.

Krishna Kumar is an Engineering graduate from Regional Engineering College, Trichy and holds a Post Graduate Diploma in Business Administration with specialization in Portfolio Management from Loyola Institute of Business Administration, Chennai.

2018 was a difficult year for stocks but the Nifty seems to have stabilized from November onwards. The market’s reaction even to BJP’s defeat in the recent Assembly elections was surprisingly mild. What is your outlook on equities for 2019, especially in view of the upcoming Lok Sabha elections?

While the run up and outcome of the general elections could add to volatility, steady earnings revival could mitigate the impact. Macros look good, earnings are expected to grow at 20%+ for the next two years, driven largely by the rebound in the banking sector. Capital formation also seems to be picking up.

The valuation of the Indian market trading at 16X FY2020E EPS appears reasonable, especially when viewed both against recent or historical valuations (19x/ 16x 12-month forward P/E) and earnings growth expectations. Mid cap and small cap indices which were trading at a premium to Nifty are trading at a good discount now despite having reasonable visibility on growth.

How do we think the interim budget affects the market?

The government continued to maintain a balance between fiscal prudence, growth stimulus and need to alleviate the stress in agricultural households in the interim budget. Concerns for the bond market include the Internal & Extra Budgetary Resources (IEBR) for the current year that has seen an upswing from budgeted levels, the slower deposit growth in the system and the dropping SLR ratios of banks that are funding credit growth. Improving appetite externally for Indian debt could be helpful.

From an equity portfolio perspective, consumption gets a leg up – FMCG, food and discretionary products like brown goods, durables, two wheelers, entertainment, retail and branded apparel. Consumer financiers could continue to be in a sweet spot.

The shape of upcoming Brexit is still unclear. What will be the effect on Indian companies which have significant investments in these markets such as Tata companies and companies with operations in these markets in the pharmaceuticals and automobile sectors? Also, please share your views on the likely impact of Brexit on global equities in general and particularly Indian stock market?

India has negligible direct impact considering the trade and investment linkages. We are yet to get colour on the final Brexit deal. One may have to wait for clarity there, but India is relatively well insulated from this event.

Please share your views on the other risk factors weighing on the market in 2019 e.g. US / China trade issues, US interest rates, crude oil price etc?

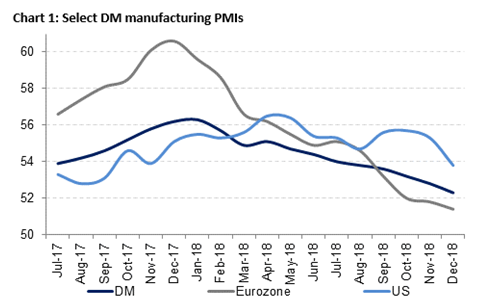

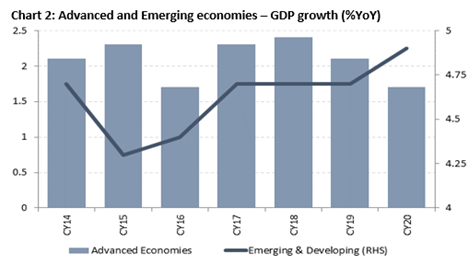

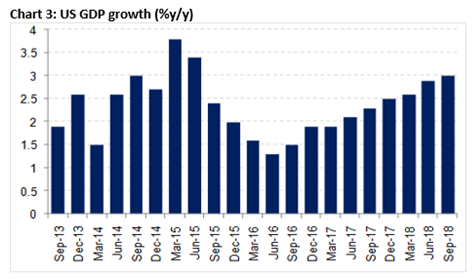

Markets have been impacted incrementally by concerns about global growth outlook. Global growth rate which was around 3.8% in 2018 is expected to come down to 3.5% this year wherein developed markets are expected to grow slower at 2.0% as against 2.3% last year. This is reflected in in Chart 1 (Softening PMIs). At the same time, emerging and developing economies are expected to maintain a growth rate of around 5% (Chart 2). Flat yield curves in the US have further fueled this view and US growth is expected to come down to 2.4% from the present level of 3.0%. As seen in Chart 3 below, the US economy might be near peaking due to waning effects of tax cut benefits seen in CY2018. Further escalation in China-US trade issues may exacerbate the likely slowdown in global growth.

In this background, we expect a dovish shift in central banks’ stands, especially the US Fed to be more patient on rates and more flexible on balance sheet size while emerging markets could see easing. China stimulus in terms of monetary and fiscal easing would further help emerging economies. The ECB could introduce a new bank funding facility by mid-year. An increasingly dovish FOMC policy stance should also help to weaken USD. This should provide an additional boost to emerging markets beyond the rate impact. We expect global liquidity to be stable, DXY to be in a range and this provides a positive framework for good inflows to emerging markets, particularly a high growth economy like India.

The last 12 months were very difficult for the midcap and small cap segments of the market. Can we assume the midcap stocks (in general) have bottomed out? What is your outlook on midcaps for 2019 and (beyond in the medium term), especially in light of the view that midcaps comprise around 40% of your fund’s (Sundaram Large and Midcap Fund) portfolio? Will you advise investors to increase exposure to midcaps now?

The sentiment has been quite weak in the mid and small cap space and continues to be so. Valuations now are quite reasonable having come off 30% on an average for many stocks. The near-term election related uncertainty is also not helping. Our firm belief that midcaps are a key part of an investor’s long-term portfolio as they add higher alpha to returns. Given the current valuations, we feel that investors can add to midcaps with a 2-year view.

Sundaram Large and Midcap Fund had a strong performance track-record over the last 5 years creating high alphas for investors. Trailing 5 year returns fund beat the benchmark returns by more than 4%. At the same, over the last 1 year, when the going was very difficult for midcaps, your fund was able to limit the downside and has been one of the best performing funds in the large and midcap category. For the benefit of investors among our readers, please explain key elements of your investment strategy which enabled this strong performance across varied market conditions?

We follow a blended approach for Sundaram large and Midcap Fund. Sectors/ themes are selected using a top-down approach with a focus on the long-term, while the stocks that make up the portfolio are selected using a bottom-up approach. The large cap portion of our portfolio is well-controlled, some holdings are from the high end of the spectrum, while some others are smaller large caps. When it comes to midcaps, we prefer the larger midcaps to the smaller ones, companies with an asset size of $3-4billion. The large cap exposure is about 50-60% and midcap about 40-50%, with some reserves in cash. With our slight large cap tilt, and preference for larger midcaps, we were able to limit the downside for investors.

You are overweight on sectors like Banks, FMCG, Cement and Construction with respect to your benchmark index, while you are underweight on IT, Automobiles etc. Which are the industry sectors where you see strong earnings growth opportunities over the 3 years or so?

Our sector picking is done with a long-term view and we are of the opinion that banking, consumption, and construction will pay-off in the long term. We are positive on the consumption story – especially consumer discretionary, with a bias toward automobiles, consumer durables, branded apparel, retail and entertainment sectors. In the financial space, we see growth in the retail credit space, being positive on the corporate credit component. Also, financial services such as insurance, wealth management have some short-term softness, but have the potential to deliver in the long-term. We also see investment pick-up in core sectors – cement, engineering and construction.

What will be the key drivers of your market cap and sector strategies going forward? Will we see incremental allocations (in percentage terms) to midcap stocks in Sundaram Large and Midcap Fund?

We intend to run a portfolio with midcap exposure typically at about 45% but the range could be 35-50% across periods. The intent is to give investors a fund that generates stable outperformance with lower volatility. Valuations and growth continue to be our key pivots of the strategy in terms of sector strategies. The fund will be a 40-stock portfolio with high conviction ideas that play on the India growth story.

Last year mutual fund houses, including Sundaram have classified their schemes in different categories as per SEBI’s directive. In our view, this reclassification provides much greater clarity to investors about the characteristics of different schemes. While the differences between large cap, midcap and small cap are quite clear, many retail investors get confused between “multicap” and “large & midcap” categories. For the benefit of new / less experienced investors, please explain the difference between the two. Also, who should invest in “large and midcap funds”? What is your minimum recommended investment tenor to get the best returns from these funds?

The primary difference between large and midcap funds and multicap funds is in their allocation to the different market capitalizations. Large and midcap funds must have 35% in large caps, and 35% in midcaps, whereas there is no such category restriction on multicap funds. They can even have lesser than 35% allocation to any of these categories and hold a mix of stocks from all market caps. Any equity investment has to be viewed with a 3-year tenure.

What is advice for retail investors who want to invest in equity for their long term financial goals? How should investors go about their investment planning if the market turns volatile again this year or in the future?

For investors with long-term goals, near-term market volatility shouldn’t drive their investment decision. They can start STPs in a healthy mix of large, mid and small cap funds for wealth creation, and own a balanced fund (aggressive hybrid equity now) to add a little stability. As they near their goals later, they can move to investments to funds with lesser volatility, such as a liquid fund.

Recent Interviews

-

In Conversation by Advisorkhoj with Ms Saloni Kapadia Fund Manager The Wealth Company Mutual Fund

Jul 23, 2026

-

In conversation with Mr Gautam Kaul Senior Fund Manager Fixed Income with Bandhan Mutual Fund

Jul 23, 2026

-

Partner Connect by Advisorkhoj with Mr Suresh Royal Rupee MFS Pvt Ltd Tirupathi

Jul 20, 2026

-

In Conversation with Mr Ritesh Pathak Deputy CBO Retail Sales & Passive with Motilal Oswal MF

Jul 13, 2026

-

Partner Connect by Advisorkhoj with Mr Ramu Chellimilla & Mr B G Srinivas Invictus FinServ LLP Secunderabad

Jul 1, 2026

Fund News

-

SBI Mutual Fund SIF launches Magnum Equity Ex Top 100 Long Short Fund

Aug 7, 2026 by Advisorkhoj Team

-

Axis Mutual Fund launches Axis Nifty Energy Index Fund

Aug 7, 2026 by Advisorkhoj Team

-

Kotak Mahindra Mutual Fund launches Kotak Diversified Equity All Cap Omni FOF

Aug 5, 2026 by Advisorkhoj Team

-

Franklin Templeton Mutual Fund launches Franklin India Short Term Fund

Aug 5, 2026 by Advisorkhoj Team

-

Edelweiss Mutual Fund launches Edelweiss Nifty REITs and Realty Index Fund

Aug 5, 2026 by Advisorkhoj Team