7 golden savings tips without compromising your lifestyle

Much of the discourse in the personal finance space is on investing. But the question is, how will you invest, if you are not able to save enough? Regular savings habit is part of our ancient culture. But in today’s day and age, with rising cost of living, dramatically better improved lifestyle and with consumerism part of our culture saving more is a challenge. In this article, we will discuss some golden savings tips that can help you, without having to compromise your lifestyle.

Prepare a monthly budget:

Preparing a monthly budget is half the battle won. Budgeting should not be a theoretical exercise and certainly not based on gut feel. When you prepare your monthly budget start with what is absolutely necessary, e.g. food, rent, utility bills, transportation costs, children’s school fees, insurance premium, home loan EMIs etc. You should keep money aside for these essential expenses. The balance is discretionary spending. You should try to minimize your discretionary expenses and maximize your savings. How can you do that? Sit down with your monthly bank or credit card statement, and study your spending habits. You should question all material expenses and eliminate wherever possible. Alternatively set yourself a savings target and stick to it assiduously.Plan your purchase:

Do you remember that our parents used to have a shopping list, whenever they went for grocery shopping. The shopping list is of great value, if you are trying to minimize your spending especially when you are shopping in a supermarket. With a shopping list you shop with a sense of purpose and only buy items that you need. Without a shopping list, you are likely to buy any item that catches your fancy, as you amble down the aisles in your supermarket. The ambience and product placements in supermarkets are designed to make you spend more and feel good about it. Just as an example, the music in the supermarket often has a slow rhythm. The idea is to make you walk leisurely, so that your wandering eye can catch some attractively packaged stuff that most probably we do not need. Smart product placement often makes you spend more. The most expensive brands are kept at the eye level and the less expensive brands are kept in the upper or lower shelves. Naturally the most expensive brands will catch your attention and make you buy it. Many supermarkets have consumer durables next to fruits and vegetables. If you think about, it does not make logical sense. But there is a science behind the product placement. The bright colours of fruits and vegetables serve to brighten up our mood. The happier we are, the more we are likely to spend on a consumer durable item that we may do not need. If you have a shopping list, you will buy only the items that you need and leave.Avoid debt:

You should avoid debt. Debt comes in many forms e.g. credit cards, buying expensive items in equated monthly instalments etc. You should remember whenever you take debt, in whatever form, you have to incur interest expense. Very often we do not factor it in our purchases. You should use your debit card, instead of credit card for your purchases. If you use credit cards, you should ensure that you pay the full amount due on a monthly basis. Setting up an ECS to pay the full amount due on your credit card on a monthly basis before the due date, will prevent you from incurring interest expense and late payment fees. You should avoid EMI payment schemes for your purchases. If you cannot pay in full, probably you cannot afford to purchase the product. You should wait till you have saved enough to purchase it by paying the full amount or opt for a lesser priced product. You should not be enticed by promotions like “zero interest” EMIs for purchase of certain items. There is no such thing as a free lunch. For such items with zero interest EMIs, you are likely to get a discount if you pay upfront. There is the opportunity loss of not getting the discount, if you go for the EMI option. If you already have debt, you should make it a priority to pay it in full, before you spend on non essential items.Be patient when buying expensive gadgets:

When it comes to buying gadgets like smart phones, tablets etc very often we want to buy the latest model. But remember the latest model is often the most expensive one too. You should ask yourself, do you desperately need the latest model. If you can afford to wait for a year or even few months, you can get the same model at significant discount. However, I do realize that it is easier said than done. When it comes to electronic gadgets, people are led by “herd mentality”. You should, however, remember that smart savers are never influenced by what their peer group is doing, because most people in the peer group are not smart savers.Shop online:

Shopping online can get you large discounts and help you save more. Why is online shopping cheaper? Real estate cost of brick and mortar stores are getting expensive by the day, especially in big cities. Online retailers buy their merchandise directly from the source, instead of going through intermediaries. Some online retailers are well funded by venture capitalists. They can afford to adopt predatory loss pricing to capture the target customer segment. Whether loss pricing amounts to restrictive trade practises is a debate that is going on, at the end of the day the customer is the winner. Online retailing is picking up in India at an accelerated pace. However, some customers still have a mental block when it comes to online shopping. They are worried about quality, reliability and customer service issues. In most cases it is only a perception issue. Regular online shoppers vouch for quality, reliability and good customer service of products purchased. Some shoppers like to touch and feel the product before buying. You can visit a brick and mortar store to get a closer feel of the product. But you can always order it online and save costs. Online shoppers can follow some simple tips to make the online shopping safe and enjoyable experience.- You should start your online shopping in a trusted familiar site, rather than shop with a search engine like Google. Searching for a product on Google may throw up very enticing offers, but you cannot be sure about the trustworthiness of many websites. On the other hand if you shop from well known online sites like EBay, Amazon, Flipkart, Myntra, Snapdeal etc, likelihood of things going wrong is quite less.

- Always compare prices of the same item on different websites before purchasing, to get the best deal. Different online shopping sites run different promotions and chances are you can get a better deal if you explore multiple options

- Always check the shipping charges before placing your final order. Otherwise, you may be hit with a nasty surprise when you get the final bill.

- Always check for SSL encryption when using your credit card for online purchases. SSL encryption is depicted by the icon of a padlock on the address bar.

- Only fill out the mandatory personal information, when making an online purchase. There is no benefit in filling out non-essential personal information like date of birth, spouse’s names etc. On the other hand, such information in the hands of cyber thieves can be very dangerous.

- At the cost of sounding like flogging a dead horse, you should always use strong passwords, with combinations of upper case and lower case, numbers and symbols.

- When on the move, you can also use your mobile phone for online shopping. When shopping using your mobile phone, you should use the mobile apps of the online retailers instead of going to their mobile websites. This will ensure online shopping on mobile a more efficient experience.

Park your savings in liquid funds:

You should consider liquid funds as an alternative to savings bank. While having an emergency fund parked in savings bank is essential from a financial planning perspective, if you can wait for a day to withdraw the funds, liquid funds are an excellent alternative to your savings bank account. While savings bank interest is usually around 4%, liquid funds provide returns in the region of 8 – 9%. The extra income is very useful from a long term perspective, because you can re-invest it in high yielding assets like equities and earn higher returns over a long time horizon. While liquid funds are subject to market risks, the nature underlying instruments in a liquid fund ensures a very high degree of safety. Withdrawals from liquid funds are processed within 24 hours on business days. Some liquid funds offer cash withdrawal facilities with ATM cards, but most do not. You can read more about liquid funds in our article, Liquid Funds: A good option to park your surplus cash Part 1. When planning your investment in liquid funds, you should note that redemption requests are not processed during public holidays or weekends. Therefore, you should have enough funds in your savings bank account to meet exigencies over weekends and public holidays. Having said that, most of us keep funds in our savings bank that we will not need in the next few weeks or even months. Liquid funds are an excellent destination to park those funds. You can read about top liquid funds for investment in our article, Top liquid funds for parking your surplus cashStart investing systematically:

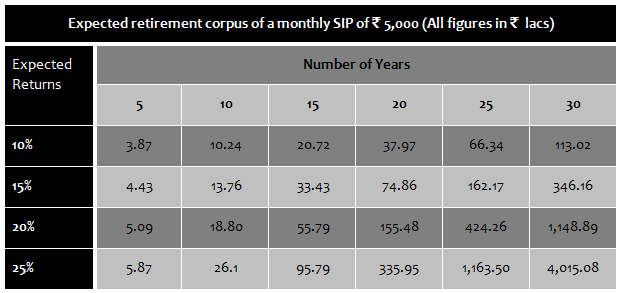

How is systematic investing a savings tip? It is, in fact one of the best savings tips. It forces you to save more, by leaving a smaller surplus in your bank for discretionary spending. After a careful analysis of your expense, you should prepare your monthly budget as discussed earlier and set yourself a savings target. Based on your savings target, you should start a monthly systematic investing plan and set up an ECS with your bank account at the start of every month. That way you will prioritize long term investment over discretionary spending. With a systematic investment plan over a long time horizon you will benefit from the power of compounding of your investment returns and create wealth. The table below shows a scenario analysis of the corpus built over various periods of time at different investment return rates, with a monthly SIP amount ofर5000/-

The table above clearly illustrate the advantage of starting early. For example, in the above table if you started investing through SIP at the age of 30, you would generate a corpus of nearly

र11 crore at your retirement (assuming 20% expected returns), by investing onlyर5000/- per month. If you do not have an SIP, you may end spending it on some discretionary item like expensive clothes, phones, restaurants etc, which gives you instant gratification but is not particularly beneficial for your wealth creation objective. When you are investing in an SIP, you should make sure that the asset class that you are investing in, is consistent with your risk profile. Equity as an asset class gives the highest returns over a long time horizon.

RECOMMENDED READS

LATEST ARTICLES

- Why you need to have hybrid mutual funds in your portfolio: Different types of funds Part 2

- Why you need to have hybrid mutual funds in your portfolio: Misconceptions Part 1

- Which is the best time to invest in mutual funds

- Economic slowdown: Is it real and what should you do

- Importance of liquidity in investing: Mutual funds are ideal solutions

Locate ICICI Prudential Mutual Fund Distributors in your city

An Investor Education Initiative by ICICI Prudential Mutual Fund to help you make informed investment decisions.

Quick Links

Follow ICICI Pru MF

More About ICICI Pru MF

You haven't found the answer for your queries? Do post your queries to ICICI MF.

POST A QUERY

POST A QUERY