6 common retirement planning mistakes one should avoid

Retirement planning is one of the most ignored aspects of financial planning in India. But with changing socio economic conditions in our country, retirement planning now is more important than ever before. In this blog we will discuss 6 common retirement planning mistakes that individuals must avoid, in order to achieve financial independence and be free from financial stress during their retirement years.

Not starting retirement planning early enough:

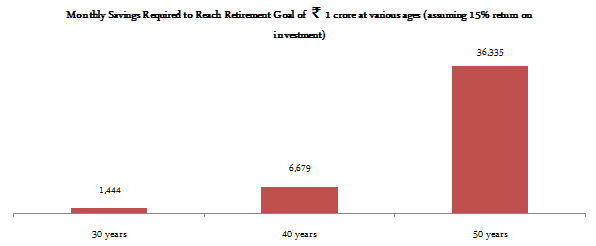

Most individuals do not think about retirement planning early in their careers, but start to worry about it only when they are nearing retirement. Starting to invest for your retirement from early age has great benefits. The earlier you start the better are the chances for creating wealth as you get more return for more time on your investments. Many investors are not aware of the power of compounding. If an investor wants to set a goal of creating a retirement corpus ofर1 crore at age 60, he or she can achieve it with a much smaller amount simply by starting earlier, as shown in the chart below.

We can see from the chart above that starting early has major benefits. Starting too late, on the other hand, will put your retirement planning at serious risk.![]()

Ignoring the impact of inflation in retirement planning:

Another common mistake is to ignore or even underestimate the impact of inflation on expenses. Inflation cannot be wished away as it reduces the value of savings. The chart below shows the annual (December to December) CPI inflation rates in India from 1984 to 2014.

The chart above shows that except for a 5 – 6 years period from 2000 to 2006, the annual inflation rate in India has been mostly above 6%. The geometric mean annual inflation rate over the last 3 decades has been 7.8%. This means than an expense of![]()

र1,000 in 1984 would be nearlyर10,000 today. Now, if we extrapolate this 20 years forward, an expense ofर10,000 today, would be nearlyर45,000 20 years from now. Even if we expect inflation to moderate in the long term to an average of 5 – 6%, living expenses will be at least 3 to 5 times higher 20 or 30 years later. In other words, if you are 30 years old and your monthly expense isर20,000, you should expect your monthly expense at the same lifestyle to be overर1 lac by the time you retire. When you set a retirement goal for yourself, you should always factor in the effect of inflation.Misconception with regards to risk in retirement planning:

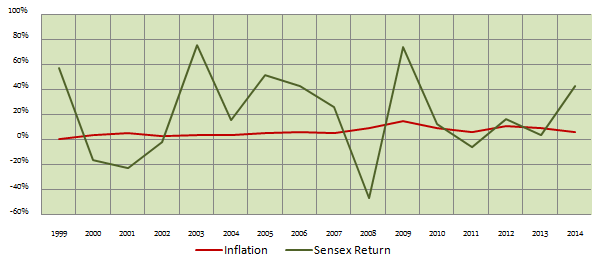

Most investors believe that investing in risk free or low risk investment options is the best retirement planning strategy. Accordingly, they opt for investment options like PPF, VPF, NSC and life insurance endowment plans. Investing in low risk investment options can actually result in taking a risk with your retirement plan. Risk free or low risk investment options often fail to beat inflation, which leaves the investor short of his retirement needs. Let us take for example life insurance endowment plans. Historically, returns of life insurance endowment plans have been around 6%, which is well below the average historical inflation rate discussed above. Post tax returns of other risk free investment options have also struggled to beat inflation. Equity as an asset class has historically been able to beat inflation in the long term and create wealth for the investor. The chart below shows the Sensex returns and the annual inflation rates from 1999 to 2014.

We can see from the chart above, that while Sensex returns have been volatile, it has managed to beat inflation. The compounded annual growth rate of the Sensex from 1999 to the end 2014 is around 16%, while the geometric mean average inflation rate during this period was 6.5%. Long term investors must not equate volatility with risk. Investors should understand that volatility is a short term phenomenon and does not impact the long term objectives. For long term investors, not meeting the financial goal is the real risk. It is essential that equities form a significant portion of your investment portfolio to help you meet your retirement goals.![]()

Not having enough health insurance:

Healthcare costs in India are increasing at a distressing rate. Based on some estimates, the annual healthcare inflation is in the range of 15 – 25%. A hospitalization for a serious illness can costर5 lacs or above. While health insurance or Mediclaim is essential for all, it is even more relevant for senior citizens, because health risks increase substantially with advancing age. In the absence of Mediclaim, a serious illness in your family can cause financial distress at a time when you least expect it. While many companies offer group health insurance cover for their employees, there are companies which do not. Even if employees are covered under the group insurance plan of their employers, they should check what kind of benefits their employer’s group health insurance policy offers, total amount of cover, and nature of illnesses covered. Employees who are covered under their company’s group health insurance policy lose their health cover on retirement. This puts them and their dependents at serious risk. IRDA's portability guidelines cover policy transfers from group to retail, allowing retiring employees to switch to the retail policy of the insurer offering the group insurance plan to their former employer. However, the premiums and the policy terms may change once you switch to the retail plan. Alternatively senior citizens can consider buying an individual or family floater Mediclaim from an insurer of his or her choice.Not being debt free early enough:

We should understand that, debt in any form has a cost associated with it. Home loans, vehicle loans, credit card loans etc, have interest cost which comes out of our savings. For unsecured debt, like credit card loans the interest cost can be quite high. Many investors over extend themselves buying a house and the home loan EMIs constitute a large chunk of their incomes. Interest costs comprise the major part of the home loan EMIs in the early and mid part of the home loan term. The higher the interest and the longer we pay it, the more we put our long term financial goals at risk. We should strive to be debt free early in life, so that we can free up our savings to work towards our retirement planning.Completely avoiding risk after retirement:

While the conventional financial wisdom dictated that we avoid risks after retirement and allocate our accumulated corpus to safe investments like fixed income, longer life span and high inflation necessitates a rethink of this approach. Retired lives can now easily 25 years or even more. On account of high inflation and increased longevity, you can run out of your funds if they are deployed in low yielding assets. Let us try to understand with the help of a couple of examples. Suppose you have accumulated a retirement corpus ofर50 lacs. After retirement you deploy your funds in risk free assets like fixed deposits giving you post tax return of 7%. Let us assume your monthly expense isर50,000 and the inflation rate is around 7%. You will run out of your funds in only 8 years. Even if you accumulate a corpus ofर1 crore and deploy it in risk free assets with a post tax yield of 7%, with a monthly expense ofर50,000 and inflation of 7%, you will run out of your funds in 16 years. If you live till 85 to 90, you will have to financially dependent on someone else for the last 10 to 15 years of your life. Now let us see what if you deploy 25% of your corpus in high yielding assets like equity and the balance in low risk debt investment. Assuming you get 20% return on your equity investment, aर1 crore can last more than 23 years. Therefore, it is prudent not to completely avoid equity after retirement. You should set your asset allocation depending upon your financial situation.

Conclusion

In this article, we have discussed some common retirement planning mistakes that we should avoid. Retirement planning is a very important part of financial planning. We should take retirement planning seriously from an early stage of our careers, so that we can have a happy and fulfilling retirement.

RECOMMENDED READS

LATEST ARTICLES

- Why you need to have hybrid mutual funds in your portfolio: Different types of funds Part 2

- Why you need to have hybrid mutual funds in your portfolio: Misconceptions Part 1

- Which is the best time to invest in mutual funds

- Economic slowdown: Is it real and what should you do

- Importance of liquidity in investing: Mutual funds are ideal solutions

An Investor Education Initiative by ICICI Prudential Mutual Fund to help you make informed investment decisions.

Quick Links

Follow ICICI Pru MF

More About ICICI Pru MF

POST A QUERY