Mutual funds are ideal investment options for Retirement Planning

The goal of retirement planning is to achieve financial independence and to be able to maintain your current lifestyle even during your retirement years. Average investors in India have traditionally invested in employee provident fund, public provident fund (PPF), post office monthly income scheme (MIS) and traditional life insurance savings plans to meet their retirement needs. But small savings schemes (e.g. PPF, NSC etc) and traditional life insurance savings plans (e.g. endowment plans or pension plans) are likely to fall short of meeting retirement needs in the future due to increased life expectancy, higher inflation levels and rising cost of healthcare.

Effect of inflation

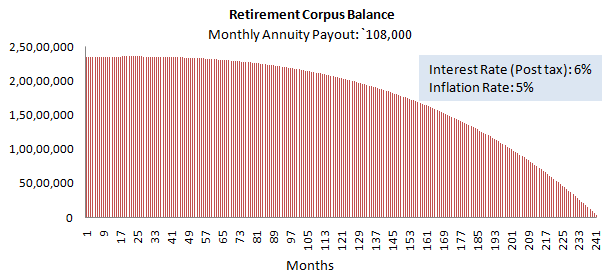

Inflation erodes the value of money over time and makes saving for retirement a tough challenge. If you are 30 years old and your monthly expense is `25,000/-, your expense will become almost `1.1 lacs a month at a 5% inflation rate by the time you retire in 30 years. How much retirement corpus you need to build just to maintain your current standard of living after your retirement? Let us assume you can earn post tax interest of 6% on your retirement corpus and the inflation rate is 5%. If you live for 20 years after your retirement, you will need a corpus almost `2.4 crores to generate monthly annuity payments of `1.1 lacs adjusted for inflation so that you can maintain your current standard of living.

Traditional savings schemes may not be sufficient to meet retirement needs

Continuing with the above example, if you get 8.7% interest on your investment, which is the highest you can earn on the post tax basis on your small savings investment (e.g. PPF), you need to save at least `1.6 lacs a year over 30 years to build a corpus of `2.4 crores in order to meet your retirement needs. The maximum amount you can deposit in PPF in a year is `1.5 lacs. The other savings schemes give lower returns on a post tax basis and therefore you need to save even more. Furthermore, over the last 20 years or so, the interest rates of provident fund, PPF and other small savings schemes have been steadily declining. The chart below shows how PPF interest rates have declined over the past 15 years.

PPF interest rate has now been linked with the 10 year Government bond yield. 10 year bond yields are currently near historic highs. Bond market experts believe that interest rates will start softening from next year and therefore we may see lower PPF interest rates in the future.

Bank or Post Office Fixed Deposits give 8 – 9% interest, but the interest income is taxable as per the tax rate of the investor. For the investor in the highest tax bracket, the effective post tax return from fixed deposits is in the range 5.5% - 6.2% only. The returns of traditional life insurance savings plans like endowment plans are tax free, but the effective returns are even lower at around 6 – 7%. The bonus rates of Life Insurance Corporation of India’s (LIC) endowment plans have been declining for the past 10 years. The bonus rate for `1,000 of sum assured of LIC’s endowment plans, which was `65 in 2003, has now declined to `42 in 2014. If the downward trend continues, the effective returns from the traditional insurance savings plans will be even lower in the future. The current inflation rate (as on August 2014) is 7.8%, which is higher than the post tax returns of most traditional savings schemes. It is true that the current inflation rate is unusually high, but when inflation goes down, so will the interest rate. Thus, we have seen that, it is difficult to beat inflation and accumulate sufficient retirement corpus through the returns generated from traditional savings schemes.

Equities as an asset class can beat inflation in the long term

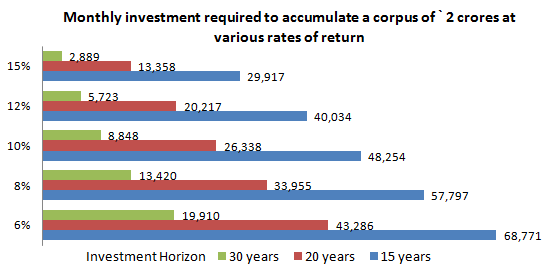

Equities, on a historical basis notwithstanding bear market periods in the interim, has consistently beaten inflation and generated superior returns compared to other asset classes over a long time horizon. Over the last 15 – 20 years the Sensex has given returns of 10 – 15%. Going back to our earlier example, if you get an average 12% return on your equity investment, you need to save only `80,000 a year over 30 years to build a retirement corpus of `2.4 crores in order to meet your retirement needs. The chart below shows the monthly investment required to accumulate a corpus of `2 crores at different rates of return over different time horizon.

The chart above shows that by making a monthly investment of only `3,000 – 6,000 you can accumulate a corpus of over `2 crores over 30 years, if you get a return of investment of 12 – 15%. The only asset class that give such high rates of returns over long time horizon on a consistent basis is equity. In fact top performing equity mutual funds have given more than 15% annualized returns over the past 15 to 20 years. As such in developed economies like the US, most households invest in retirement plans through equity mutual funds.

Mutual funds are the ideal investment option for retirement planning

There are a number of benefits of retirement planning through mutual funds:-

Capital appreciation over a long time horizon:

As discussed above, equities can provide superior capital appreciation in the long term, compared to other asset classes. Over the last 10 years, the Sensex has given annualized returns of nearly 17%. Even over the last 15 years, the Sensex has given annualized returns of nearly 13%. Top performing mutual funds have consistently beaten the market and given even higher returns. Systematic Investment Plans in top performing diversified equity funds have given 17 – 25% annualized returns over the last 15 years.Tax Efficiency:

Equity mutual funds are more tax efficient than most of the savings schemes. Long term capital gains for equity mutual funds are tax exempt. Dividends of equity mutual funds are also tax free. Long term capital gains of debt funds are taxed and 20% with indexation. With high levels of inflation capital gains tax with indexation can be reduced significantly.Systematic Investment Plan:

Systematic Investment Plan (SIP) is an excellent investment option for retirement planning. SIPs allow investors to start retirement planning early in their working lives. The earlier you start the more you can benefit from the power of compounding for wealth creation. SIPs also enable investors to stay disciplined in saving and investing. These are very flexible instruments. There are no restrictions and penalties on regular SIP payments and withdrawals, unlike PPF or pension plans. SIP is an ideal mode to build your retirement corpus.Variety of options to suit different investors’ needs:

Mutual funds offer a large variety of options to meet the needs of investors with different risk tolerance levels and financial goals. There are growth funds that provide capital appreciation and income funds that help the investors meet their income needs. Balanced funds can help the investors optimize their asset allocation requirements, while monthly income plans can provide regular income with growing the capital of the investor at the same time.Systematic Transfer Plan:

Asset allocation of investors is a dynamic process, since it changes with the change in the risk profile of the investors (please refer to our article, Asset Allocation strategies for different age groups). Young investors should have a large portion of their portfolio invested in equities. As you approach retirement, you should rebalance your portfolio mix to have a greater allocation to debt investments to protect your accumulated capital. A Systematic Transfer Plan (STP) allows you to systematically move specific amounts from one scheme to another of the same Asset Management Company (AMC). Investors can use STP to switch funds from equity funds to balanced funds to debt funds or monthly income plans, as they approach retirement.Systematic Withdrawal Plan:

In order to meet your monthly income needs after retirement, you can opt for Systematic Withdrawal Plan. SWP allows you redeem withdraw specific number of units on a regular (e.g. monthly, quarterly etc) basis. It provides you with a regular income without attracting income tax.

Mutual funds are subject to market risks

Equity oriented mutual funds are market linked investments. As such they are subject to market risks and volatilities. However, short term volatility of NAVs should not concern investors with a long time horizon. SIPs take advantage of short term volatility by accumulating units at a lower cost, thereby generating higher returns. If you have sufficiently a long time horizon, you should be able to ride out volatility and grow your capital to meet your retirement needs.

Conclusion

In this article we have seen that mutual funds are ideal investment options for retirement planning. The key to successful retirement planning is to start early, stay disciplined and make the right investment as you progress through your working lives. You should consult with your financial advisors to identify the mutual fund schemes suitable for your risk profile that can help you meet your retirement goals.

RECOMMENDED READS

LATEST ARTICLES

- Why you need to have hybrid mutual funds in your portfolio: Different types of funds Part 2

- Why you need to have hybrid mutual funds in your portfolio: Misconceptions Part 1

- Which is the best time to invest in mutual funds

- Economic slowdown: Is it real and what should you do

- Importance of liquidity in investing: Mutual funds are ideal solutions

An Investor Education Initiative by ICICI Prudential Mutual Fund to help you make informed investment decisions.

Quick Links

Follow ICICI Pru MF

More About ICICI Pru MF

POST A QUERY