Is return from Real Estate really that high

Over the last ten years, real estate in India has given good returns. Enticed with the idea of owning a house and seeing their assets rapidly appreciate in value, countless Indians have invested a large part of their savings in real estate. Many cities and suburbs have seen a veritable real estate boom in the last decade. While some investors had bad experience with their real investment due to delayed possession, stalled projects and in some cases the projects never taking off, nevertheless, many investors got excellent returns from their real estate investments. However, there is a big difference between the real returns from real estate and what is apparent. Let us take the case of Akash, a resident of Gurgaon, a New Delhi suburb. Akash purchased an apartment 10 years back for Rs 40 lakhs. The market valuation of his apartment today is Rs 1.5 crores. So Akash’s profit is Rs 1.1 crore on his Rs 40 lakhs investment? Not quite so. Real estate is a very complex investment and there are a number of factors involved, which investors casually ignore. In this article, we will examine different factors that affect the returns of your real estate investment. At the end, we will compare investment in real estate with other investment options.

Let us revisit the case of Akash, with whom many of us will relate, in terms of our own real estate investment. Akash bought a 2000 square feet apartment in Gurgaon 10 years back at a purchase price of Rs 40 lakhs (Rs 2000/sq ft), the market value of which today is Rs 1.5 Crores (Rs 7500/sq ft). Now we will examine the various factors affecting the returns of Akash’s real estate investment.

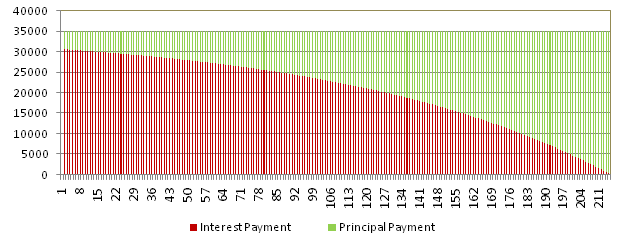

1. Home Loan: Akash took a home loan to purchase his house. As required by the housing finance company, he made a down payment of Rs 8 lakhs (20% of the house value) and took Rs 32 lakhs, 20 year floating rate home loan. The interest rate at the time of purchase was 12%. Accordingly his home loan EMI was set at Rs 35,235 per month. The home rate would have fluctuated both up and down over the past 10 years. Let us assume the average interest rate during this period was 11.5%. The chart below shows the interest and principal payments of Akash’s home loan EMI.

The red portion of the chart represents interest payment and the green portion of the chart represents the principal payment. The horizontal axis represents the number of months. As you can see, in the earlier part of the home loan term most of the EMI goes towards interest payment. In fact, for the first 7 to 8 years over 70% of his EMI goes to interest payment. Even after 10 years of his house purchase, after paying nearly Rs 41 lakhs in EMIs, nearly Rs 22 lakhs of the loan is still outstanding. After factoring in the EMI payments, the profit is no longer Rs 1 crore.

2. Stamp Duty: After Akash received possession of the property, he had to register it with the Government, as required by law. Akash bought the property in his own name. In the state of Haryana stamp duty charges at 8% for males, 6% for females, and 7% for jointly owned property. Stamp duties vary from state to state. Akash had to pay a stamp duty of Rs 320,000. He would have been better off, buying the property in the name of his wife, or jointly with his wife. Stamp duty and registration charges are additional costs that must be factored in a real estate purchase consideration.

3. Possession Delay: The possession of Akash’s apartment was delayed by 3 years. Possession delay, nowadays, is the norm not the exception. In fact, many will count Akash lucky, since his possession was delayed by only 3 years. Projects of many reputed developers have been delayed by 5 – 6 years. Nevertheless, there is a cost associated with possession delay. Mental aggravation aside, Akash had to pay both a monthly rent of Rs 10000 (with an annual escalation of 10% as per his rent agreement) and his home loan EMI for the three years. The total cost of his rent due to the possession delay was Rs 397,000. This must also be factored in.

4. Maintenance and Property Tax: After Akash got the possession of his apartment and moved in, he did not have to pay rent but he has to pay maintenance and property tax for his hose. His maintenance is Rs 3000 per month (at the rate of Rs 1.5 per square feet). Since possession was delayed by 3 years, Akash did not have pay maintenance in the first 3 years. Over the 7 year period Akash occupied the house, he paid maintenance of Rs 252,000. Akash also has to pay property tax, at average annual rate of Rs 10,000 over the 7 year period. His total cash outflow on property tax is Rs 70,000. This cost must also be factored in.

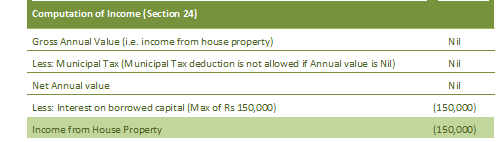

5. Income Tax: Akash could not claim any income tax deduction till he received possession of the apartment. After he received possession, Akash claimed deduction of Rs 90,000 – 100,000 for principal payment under Section 80C. However, the 80C deduction for principal payment is not relevant here since the same deduction can be claimed by investing in PPF or ELSS. Additionally, on receiving possession Akash claimed a deduction of Rs 1.5 lakhs from taxable income per annum on account of interest payment, under Section 24 of the Income Tax Act. Since Akash is in the highest tax bracket, Akash saved Rs 45,900 (Rs 1.5 lakhs @ 30.9% tax rate) in taxes on an annual basis. Over the 7 year period he saved Rs 324,450. The table below shows the calculation of income tax deduction for interest payment.

6. Broker Commission: If you buy property through a property dealer, you will have to pay a broker commission, usually a percentage of the total property value. The commission is usually around 3 - 5% of the property value, but can be negotiated. Luckily, Akash bought his apartment directly from the developer, as part of the initial allotment and therefore did not have to pay commission on purchase of the apartment. However, he will need a broker to sell the apartment. The commission paid to the broker will be Rs 4.2 lakhs (3% of the sale price, Rs 1.4 crores). This cost has to be factored in.

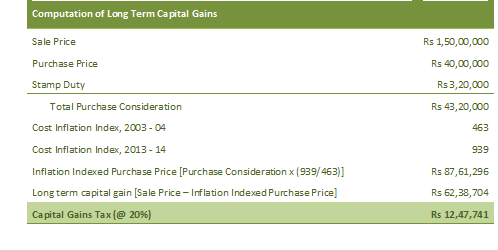

7. Capital Gains Tax: Since Akash has purchased the house 10 years back, long term capital gains will apply. Long term capital gains tax is 20% with indexation. The cost inflation index in 2003 – 04, when Akash purchased the house was 463. The cost inflation index in 2013 – 14 is 939. The total purchase consideration for Akash will be indexed for inflation by multiplying it with the ratio of Inflation Index in 2013 – 14 and Inflation Index in 2003 – 04 (939:463). The table below shows the calculation of the long term capital gains tax for Akash.

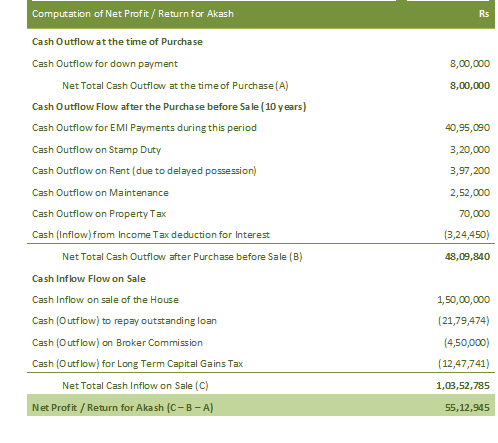

We have covered the major expenses for Akash. Now we can calculate Akash’s profit or loss.

Therefore, instead of the bumper Rs 1.1 crore profit, that was apparent earlier, the actual profit is much less at Rs 55 lakhs. Investors, who are planning to make real estate investments, must make a note of all the above factors in their financial plan, so that they have real sense of what to expect from their investments. Having said that, real return from Akash’s real estate investment is still very good compared to almost all other asset classes, with the exception of equity.

Alternative Investment Option: Equities

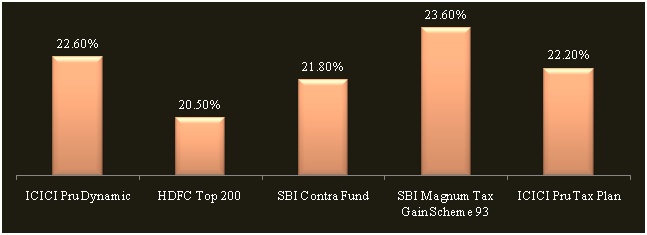

Now let us examine an alternative investment scenario. Akash’s colleague Sameer, who is in the same income bracket as Akash, decided not to buy a house and instead invested in equity oriented mutual funds, both through the lump sum and systematic investment plan route. For his investment he chose 5 top performing ELSS and large cap funds, to create a diversified equity investment portfolio. See the chart below for the annualized 10 year returns from these funds.

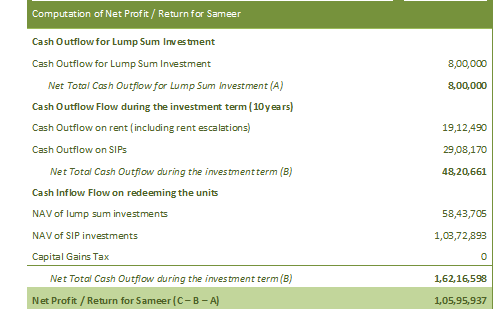

Just like Akash made Rs 8 lakhs down payment for his house, Sameer invested Rs 8 lakhs in equal lump sums in these five funds. Since Sameer did not own a house, he stayed in a rented apartment at a monthly rent of Rs 10,000 with an annual 10% escalation. In India rental yields for residential properties are in the range of 2 – 3.5% (in Gurgaon it is around 2.5%). Therefore, it can be safely assumed that Sameer’s rented house (Rs 10,000 rent) is of the same size and quality as Akash’s owned house (Rs 40 lakhs value). As discussed earlier, Akash and Sameer have the same disposable income. While Akash paid EMI of Rs 35,235 every month, Sameer invested his balance savings (Rs 24,235), after paying for rent and keeping a small buffer for future increases, in monthly SIPs of the 5 ELSS and large cap funds shown above. For his ELSS SIPs, Sameer claimed deduction of Rs 1 lakh under Section 80C. The average 10 year post tax return annualized return of Sameer’s investment portfolio is 22%. Long term capital gains from equity investments are tax exempt.

Net Profit / Return for Sameer (C – B – A) 1,05,95,937As you can see from the tables for both Akash and Sameer, both of them have almost the same cash outflow. (A) + (B) for both Akash and Sameer is almost same. But Sameer’s net return is over Rs 1 crore, is nearly double of Akash’s real return.

Why the huge difference in real returns?

• While 100% of Sameer’s SIPs were invested in units of mutual funds which gave more than 20% returns, more than 75% of Akash’s EMIs went to interest payments.

• Akash did save on rent, but the interest expense was several times more than the rent saving

• Sameer did not have to pay capital gains tax, while Akash had to long term capital gains tax

• While in the above example Sameer did not have any expense other than rent, Akash had a lot of small expenses, as discussed above, which together added up to quite a bit

• Compounded annual return of Akash’s property was 14%, whereas Sameer’s investments portfolio gave a compounded annual return of 22%

How much difference in returns can be attributed to outperformance by top funds?

A lot can be attributed to the outperformance by the top funds. If Sameer had picked up average performers (average 16% annualized returns) for his portfolio, his returns would not have been more than Akash’s. Therefore, it is very important to pick good performers as far mutual funds are concerned. A good financial adviser can help investors identify good performers.

How much appreciation is required for real estate to match the returns of top equity funds?

In the above example, Akash can match Sameer’s net returns, if the market value of his property is Rs 2.15 crores. This means a market price of Rs 10,750 / sq ft for the property he purchased at Rs 2,000 / sq ft ten years back. Can property prices appreciate from Rs 2,000 / sq ft to 10,750 / sq ft? Yes, there are examples of properties which have appreciated 5 to 6 times in value in 10 years or less. But there are not many such examples. As such, first time real estate investors should not expect such returns

Is Real Estate a good investment?

Yes. Real estate is very good investment. With interest rates peaking out, as evident in the RBI governor’s speech today, home loans will get cheaper in the medium term. There is plenty of supply in the real estate market right now and therefore prices are not increasing at the rate seen during the real estate boom years. Real estate is not as volatile as equities. In a sharp downturn, equities can lose 20 – 30% in value. However, in a real estate market downturn, prices either remain stagnant or at worst, drop by a few percentage points.

Conclusion

Real estate is good investment option. Investors should have both real estate and equities in their investment portfolio. However, it is important the investors should not over extend themselves, as they often do, when buying a house. Other financial goals like getting adequate insurance (both life and health), retirement planning, children’s education etc are equally important. Therefore, it is important that real estate investors understand their real cash flow in real estate investment, as described in this article, so that they can plan accordingly.

Queries

-

What is the benefit of mutual fund STP

Aug 29, 2019

-

How much to invest to meet target amount of Rs 2 Crores

Aug 26, 2019

-

Can I achieve my financial goals with my current mutual fund investments

Aug 24, 2019

-

Can you tell me return of various indices

Aug 19, 2019

-

What would be the post tax return on different investments

Aug 18, 2019

-

Which Principal Mutual Fund scheme will be suitable for my retirement corpus

Aug 16, 2019

-

What is the minimum holding period for availing NCD interest

Aug 4, 2019

Top Performing Mutual Funds

Recommended Reading

Fund News

-

SBI Mutual Fund launches SBI Nifty Midcap 150 Momentum 50 ETF FOF

Jul 27, 2026 by Advisorkhoj Team

-

Edelweiss Mutual Fund launches Edelweiss BSE LargeMid 60 40 Stable dividend 50 ETF

Jul 27, 2026 by Advisorkhoj Team

-

Edelweiss Mutual Fund launches Edelweiss BSE Top 10 Bank ETF

Jul 23, 2026 by Advisorkhoj Team

-

Aditya Birla Sun Life Mutual Fund launches Aditya Birla Sun Life Fixed Maturity Plan Series VA 821 Days

Jul 23, 2026 by Advisorkhoj Team

-

Gold's Recent Correction: Keeping the Long-Term Perspective

Jul 22, 2026 by Quantum Mutual Fund