6 Reasons Why Your Early Retirement Planning May Fail

We all look forward to our retirement days when we will have time on our hands and lazy days stretching ahead. We will finally live life on our own terms without the iron hand of a schedule to intimidate us and to fasten our pace. No more competing for that promotion or for the raise. No need to burn the midnight oil to meet deadlines of presentations. Retirement is the dream. Most of us manage to keep up with our lives because we know one day this hectic life will come to an end and it is this distant end in the horizon that manages to keep us on our toes.

While retirement might be the dream for which you invest and save in every possible way. Early retirement is that multimillion dollar lottery that all aspire for but very few achieve. Well, the good news is early retirement does not rest upon high degree of luck like a multimillion dollar lottery; hence, it is an achievable goal. However, the bad news is very few people manage to do this. While you hear your colleagues and elderly members retiring at the age of 60-65 you never hear anyone retiring at the age of 50. Why? It could be because it is a very unconventional move and definitely not the traditional age of putting a halt to your career. So what stops most of us from retiring early? Let us have a look.

You Didn't Start Early

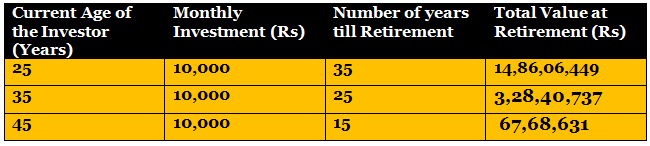

When you were in your 20s you thought retirement is too far a goal to start investing. When you were in your 30s buying that sedan or saving for a foreign holiday was higher up on your priority list because retirement seemed too far away to feel like a palpable goal. Suddenly in your 40s you were jolted with the realization that retirement is lurking in the corner and you started saving for retirement primarily because you started dreading that you will not be able to save enough. Now somewhere in your 50s even though your body and mind tells you to retire your financial condition restricts you from doing so. You do not have enough funds in your retirement corpus to create a monthly fixed payment for your expenses. Hence, the only option is to keep working and investing till the corpus reaches that magic number. It could still take as long as ten or fifteen years.

Calculations have been done using the Advisorkhoj SIP Calculator. Returns presumed @15% p.a.

From the table above it is clear which investor will be the winner in creating an early retirement corpus. You delayed your retirement planning by twenty odd years and now the same is delaying your retirement by ten to fifteen years. So if you are still wondering whether you should start retirement planning or not. Start planning! You delay the planning your planning delays you. Simple! Heard of the famous quote, 'what goes around comes around back again'?

You are Not a Disciplined Investor

Investments are not so much about the amounts you invest but rather about how disciplined you are. The level of discipline you show reflects upon your willingness to invest. The initial enthusiasm with which investors start their investing lives is often seen to fade followed by erratic investments and then none at all. The investing life ends as abruptly as it was started. As an investor you will be able to maintain the investment if that becomes an emotional priority. How concerned are you about your retirement? The answer to it is reflected in your retirement corpus. If there are too many missed SIP deadlines, then maybe retirement is not your top priority.

Discipline is also reflected by the attitude which you adopt while investing. Do you put aside your investment amount and then spend? Or investments play a secondary role to be put aside once you have spent? If it is the first one then perhaps you can hope for early retirement. If it is the second, then maybe you should start thinking if you will even retire at 60. Retirement investments have to be made a priority whether you plan to retire at 50 or 60. A disciplined investor will always put aside the investing money and then budget the rest for savings.

Too Much or Too Little Diversification

Scenario -1: One fine day your financial planner told you to diversify your portfolio. You listened to him and diversified your portfolio in all possible asset classes. The small pockets of investments scattered around all asset classes gathered returns but failed to give you the results which you had expected. You must be left feeling like jack of all trades and master of none. You are probably realizing that you should have invested in equities a little more as the returns have been fantastic or the real estate investment could have been better than the investment in gold. Too much diversification disrupted hefty returns from any one asset class.

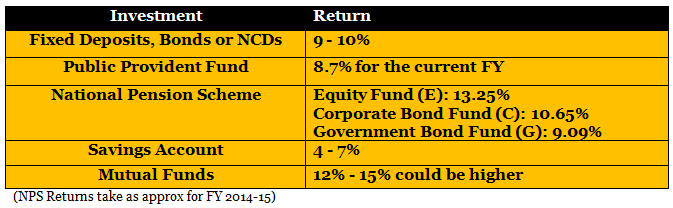

Scenario -2: One fine day your financial planner told you to diversify your portfolio. However, you did not follow his advice. Your investments primarily were in Debt funds and traditional means of investments such as savings account, fixed deposits and so on. Yes, you have been getting returns ranging anything between 4% and 10%. While you have been hearing that equities were generating 12%-15% return where you have negligible or no investments. Hence, in both scenarios it is clear that the closer you get to retirement the fund is probably not going to have enough.

Returns from Various Investments

It is time you started giving diversification a serious thought. Getting the diversification right could be instrumental for an early retirement. As you may have already guessed diversifying your portfolio is an ongoing process which changes as your investment needs keep on changing. If you are being dynamic about diversification then early retirement may not feel like an impossible goal anymore.

You are Fiddling with Your Funds

It is human nature to withdraw from bulk investments when we are in dire need of money. It is not uncommon for investors to keep withdrawing from their portfolio and making promises of replenishing the funds later. However, it remains just that, a hollow promise and a process of constant procrastination. Constant withdrawals from your portfolio upset the balance that either you or your financial adviser has created. The returns that it could have potentially generated will also decrease. During our early years investors have this tendency to withdraw from their retirement account. This goal unfortunately gets treated as a secondary goal since there is usually a time horizon of 40 years or so to build the corpus. We overestimate the time period and our ability to make up for withdrawn investments while underestimating the importance of the goal. A sum, when prematurely withdrawn from the total corpus not only potentially underfunds the goal but also loses out on all potential interest or growth earnings. Hence, if you are constantly moving around the funds then you are not being able to get advantage of compounded returns which only occurs during a long investment horizon.

Hence, if early retirement is what you are aiming for then your funds need stability. It is only when the funds stay invested for a long period of time can compounding show its magic. Being fickle minded with your money may solve your problems in the short term but it definitely will not yield results in the long term. For a goal like early retirement you need to stabilize your funds in the corpus.

Underestimating Inflation

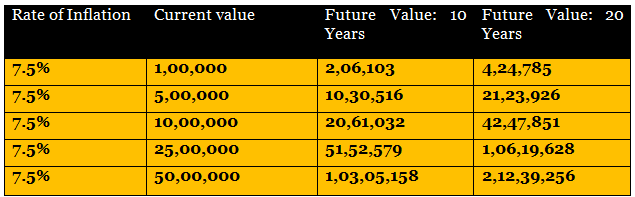

Underestimating this shark is a fatal mistake, the one that can leave you clinging to tatters. With every financial year the inflation increases and this affects the overall prices in the economy. The present cost of a commodity is different from that of the future cost because of the inflation. Hence, the sum that is enough to manage your household expenses is going to exponentially rise in the future. So when you are determining the future cost of your corpus and have underestimated the inflation it could land you in trouble. Big trouble! So if you think in the future the inflation is going to be 7% start investing assuming inflation will be 8%. This will ensure that you always have enough even if any sudden rises in price occurs.

Calculation has been done using the Advisorkhoj Future Value Calculator

In the table above you can see the future values after 10 and 20 years. If a lakh at present value is enough to current household expenses, it will certainly not be enough after 10 or 20 years from now on. Keeping the inflation and the probable future value in mind, the investments have to be carried out. If you want to retire early start investing aggressively because inflation is that shark that will eat into your retirement funds. Just the way you cannot predict future, inflation also might surprise you. Hence, beware and do not let inflation get the better of you.

The Right Avenues to Invest

Just investing is not enough. Investments are fruitful only when invested in the right avenues to gain maximum real returns. If an investment can potentially generate 15% but your avenue of investment generates a meager 4% then you are losing out on 11% excess returns which could given a huge boost to your investments. Equities are considered to be that avenue of investment which can generate returns as high as 15% or even more. In the long investment horizon the risk gets diversified thus keep your investments relatively safe. While traditional modes of investments give steady returns along with security it may not be enough to fulfill that long list of goals and also have a generous corpus for your retirement. Hence, investing in the right avenue of investment is crucial to the fulfillment of goals.

Conclusion

Financial planners and advisers stress on retirement planning because it is the only goal which if underfunded, you will not have any alternative source. You have alternative means of fulfilling education, housing and even personal expenses through credit borrowing, loans and credit cards. However, you manage your retirement on fixed income during a time when you cease to have a stable income. Retirement planning requires aggressive investment from an early age even if you want to retire at 60. Early retirement is not an impossible goal to achieve but it has to be made a priority for it to get fulfilled by the age of 50 - 55. A planning for early retirement should be done with the help of a financial advisor or retirement planner and should be reviewed yearly. So start early, start now while time is on your side and you may just finish early.

Queries

-

What is the benefit of mutual fund STP

Aug 29, 2019

-

How much to invest to meet target amount of Rs 2 Crores

Aug 26, 2019

-

Can I achieve my financial goals with my current mutual fund investments

Aug 24, 2019

-

Can you tell me return of various indices

Aug 19, 2019

-

What would be the post tax return on different investments

Aug 18, 2019

-

Which Principal Mutual Fund scheme will be suitable for my retirement corpus

Aug 16, 2019

-

What is the minimum holding period for availing NCD interest

Aug 4, 2019

Top Performing Mutual Funds

Recommended Reading

Fund News

-

Invesco Mutual Fund launches Invesco India Nifty Bank ETF

Jul 28, 2026 by Advisorkhoj Team

-

Invesco Mutual Fund launches Invesco India BSE Sensex ETF

Jul 28, 2026 by Advisorkhoj Team

-

DSP Mutual Fund launches DSP BSE MidSmall Private Banks ETF

Jul 28, 2026 by Advisorkhoj Team

-

SBI Mutual Fund launches SBI Nifty Midcap 150 Momentum 50 ETF FOF

Jul 27, 2026 by Advisorkhoj Team

-

Edelweiss Mutual Fund launches Edelweiss BSE LargeMid 60 40 Stable dividend 50 ETF

Jul 27, 2026 by Advisorkhoj Team