Mutual Fund ELSS Scheme investing facts you should be aware of

Mutual Fund ELSS (Equity Linked Saving Scheme) schemes are diversified equity funds which offer twin benefits of Tax deduction under section 80C of Income Tax Act and capital appreciation. Given below are some important facts you should know before investing in ELSS funds.

How much one can invest

You can start investing in Mutual Fund ELSS schemes with a minimum amount of Rs. 500. There are no upper limits, however, under Section 80C of Income Tax Act, the maximum amount that you can invest to avail the above tax benefit is Rs. 150,000 for the current financial year. Till last Financial year the tax benefit was restricted to upto Rs.100,000 only.

What is the taxability

Investment in ELSS funds fall under EEE category (exempt-exempt-exempt). As these funds get tax benefit under section 80C of the Income Tax Act, you need not pay any tax on the investment amount. Also, the dividends received from ELSS funds are totally tax free in the hands of the investors.

Similarly, the Capital gains arising out of these investments are totally tax free as it falls under long term capital gains tax as the holding period is more than one year. Please note all the investments in ELSS are locked-in for three years. EPF (Employees Provident Fund and PPF (Public Provident Fund) are the other two investment options where EEE tax is also applicable

Is there any lock-in period

All the tax saving investments by nature has lock-in periods. ELSS funds have a lock-in period of three years. Compared to EPF, PPF, NSC and other popular Section 80C investments, ELSS has the shortest lock-in period.

However, if you are investing through SIP (Systematic Investment Plan), remember that each SIP instalment is treated as a separate investment and therefore each is locked-in for next three years.

From the fund management perspective, however, this is a very big benefit as the fund manager can fully invest the amount received without worrying about the redemptions atleast for first three years of each investment. This also helps him take long term investment calls.

Should you opt for Growth or Dividend option

There are three options that you can opt for while investing in ELSS funds – Growth, Dividend payout and Dividend reinvestment. Growth option works like cumulative option under any investments and the full value can be realized only on redemption. Till you redeem the funds it keeps on growing under this option. If you are young, earning and have invested for long term financial planning objectives and therefore do not need any funds in between, this could be the best option for you.

However, under Dividend payout option the dividends received are totally tax free in the hands of the investors. If you are about to retire and invested in ELSS for availing Income Tax benefit under Section 80C only and also feels that some regular payouts may help you in your finances, then this could be a good option for you.

In my opinion Dividend reinvestment is not a very prudent option as each set of reinvested units get locked-in for further three years. So, you are always stuck with some lock-in units and can hardly get out of the funds fully. However, if your existing ELSS funds are in ‘Dividend Reinvestment’ option, you can change them to ‘Dividend Payout’ option by writing to the respective AMCs.

What is the risk

Being diversified equity funds, the corpus is invested in equity or equity related investments and therefore carry market risk. If you are a risk averse or conservative investor then ELSS is not the right product for you. You should look for investing in PPF – The best tax saving investment: Should you invest in PPF or ELSS

However, if you are ready to take a little amount of risk, this is the best tax saving investment option. Apart from the above tax benefits, ELSS investments help you achieve your long term financial planning objectives and also help you in wealth creation. Remember, in the longer term equities give much higher return than any other asset class. In the last ten years ELSS funds as a category (on an average) have given more than 19% trailing annualized returns. The chart below shows average historical returns of the ELSS funds category.

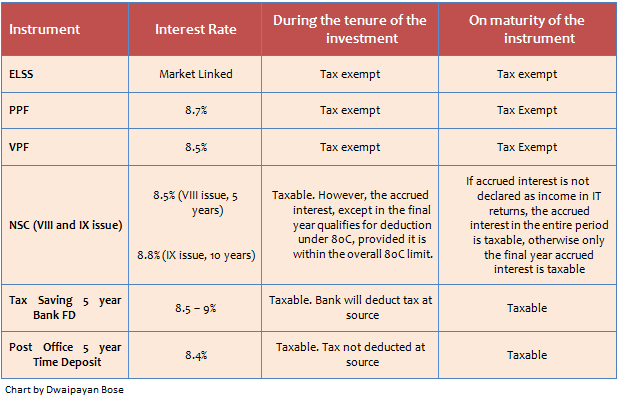

Can it can be compared with other tax saving options

ELSS offers market linked returns and is meant for investors who are ready to take little amount of risk. As fixed returns are not offered in ELSS it can not be compared with Tax saving options offering fixed interest/ returns. However, for the knowledge of our readers we have produced below a comparative chart

Please note the ELSS funds are long term investments and the ELSS as a category has a brilliant track record of past performance. In the last 10 years it has given more than 19% trailing annualized returns thus beating all other tax saving options.

Can ELSS BE considered over PPF

Yes, it can be considered! Depending upon your risk taking appetite, your age factor and the financial goal that you are trying to achieve through your tax saving investments. As mentioned earlier, PPF is the most popular tax saving option meant for risk averse investors. PPF also has a higher lock-in period of 15 years compared to three years in case of ELSS.

Even though the investments in PPF are not Equity market linked, the interest rates are not fixed. It kept on varying from 12% in year 2000 to 8.70% prevailing currently. On the other hand, investment in ELSS is totally market linked and gave much higher returns historically than PPF and other popular tax saving options.

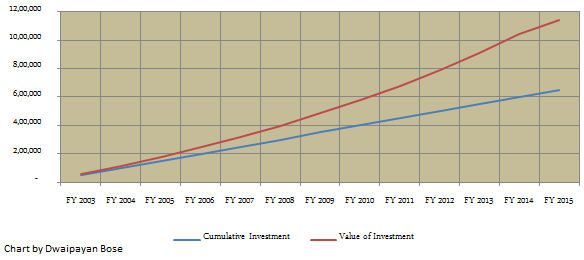

A chart produced below is self explanatory. An annual Rs 50,000 deposit in PPF started in 2002 will have a corpus of Rs. 11.40 Lacs as on September 1, 2014 against a cumulative investment of Rs 6.50 lacs. Whereas the same amount of investment in a popular ELSS fund will fetch you a corpus of Rs 37.5 lacs! The difference between the two is Rs. 26.10 Lacs.

Conclusion

ELSS has become a very popular tax saving investment option under Section 80C of Income Tax Act. If you are willing to take a little bit risk then it is the best tax saving option in this category. It is also ideal for your Retirement planning and wealth creation objectives. The ELSS has other benefits too – lower lock-in period, Tax free dividends, no capital gains tax, easy liquidity and small starting investment amount (Rs.500 only).

However, if you are against taking any risk and if your financial planning objectives does not support investing in ELSS then you should talk to your financial advisor before investing in ELSS.

RECOMMENDED READS

LATEST ARTICLES

- Why you need to have hybrid mutual funds in your portfolio: Different types of funds Part 2

- Why you need to have hybrid mutual funds in your portfolio: Misconceptions Part 1

- Which is the best time to invest in mutual funds

- Economic slowdown: Is it real and what should you do

- Importance of liquidity in investing: Mutual funds are ideal solutions

An Investor Education Initiative by ICICI Prudential Mutual Fund to help you make informed investment decisions.

Quick Links

Follow ICICI Pru MF

More About ICICI Pru MF

POST A QUERY