We would focus on select dominant players in their sectors and preferably companies which are gaining market share

BFSI Industry Interview

Neelotpal Sahai is currently Head of Equities since September 2017. He has been a Senior Vice President and Portfolio Manager in the Onshore India Equity team in Mumbai since 2013, when he joined HSBC. Neelotpal is responsible for managing three HSBC Mutual Fund equity funds. Neelotpal has been working in the industry since 1991. Previously, Neelotpal was Director at IDFC Asset Management Company Ltd in Mumbai, responsible for equity fund management, and held a variety of positions at Motilal Oswal Securities Ltd. in Mumbai, Infosys Technologies in Mumbai, Vickers Ballas Securities Ltd. in Mumbai, SBC Warburg in Mumbai, UTI Securities Ltd. in Mumbai and HCL HP Ltd. in Mumbai. Neelotpal holds a Bachelor’s degree in Engineering from IIT BHU – Varanasi and a Post-Graduate Diploma in Business Management from IIM Kolkata, both in India.

With the COVID-19 pandemic likely to cause significant impact on corporate earnings, what is your outlook on earnings recovery over the next 2 – 3 years?

FY21 will be a challenging year for the Indian economy on several counts. India is estimated to see a contraction in real GDP during this financial year after 40 years. Despite reopening of the economy, the second order impact of the lockdown could be felt through several segments of the real economy, post lockdown. These are in the form of disruption in household incomes, employment losses especially in the unorganised sector (which is roughly 88% of India’s labour force), deteriorating asset quality of corporates (leading to default risk, lower capex, growth as well as hiring moderation), among others. Additionally, the fiscal deficit for FY21 (both Central as well as combined deficit including that of states) is likely to surge. This will constrain government’s ability in providing continued direct fiscal support to revive flagging demand. The investment cycle will likely be pushed back further. Since the global growth is also going to take a beating, the external demand is also likely to remain challenging. All these factors will indeed have significant impact on corporate earnings.

Currently, full clarity about the lockdown as well as re-opening doesn’t exist. That is because the coronavirus pandemic is still ongoing and there is no drug or vaccine in the vicinity. So, in order to estimate impact on economy as well as corporate earnings, we need to make assumptions. We are assuming that the current pandemic will slowly wean away (like in rest of the world) in another 30-40 days. Also, like the rest of the world, there won’t be a second wave of the virus outbreak. And even if there is one, it would be localized one and economic impact would be limited. Normalcy should return by 2HFY21 and thus FY22 would be a normal year. From a growth perspective the numbers would look strong as they would come on the back of weak FY21. Risks to these assumptions shouldn’t be underestimated but if these assumptions were right then FY21 corporate earnings would be similar to FY20 with sectors like Consumer Staples, Telecom, Healthcare, select Financials showing growth and sectors like Auto, Industrials, Metals, Real Estate, Technology showing decline. If normalcy were to return by 2HFY21 then FY22 would be a normal year. Both economy as well as corporate earnings will show robust growth in FY22. In this scenario, the sectors that would be meaningful growth in FY22 would sectors like Consumer Discretionary, Financials, and Industrials. Long term themes like increase in digital adoption and higher expenditure on healthcare will continue in the next year too.

What in your view will be the nature of recovery in earnings? Will it be broad-based across companies and sectors or will some companies be able to grow their earnings much faster than the others?

The impact of the Pandemic and the resultant lockdown of the economy on different sectors wouldn’t have been uniform. Same is true for earnings recovery too. We have observed the trend of big becoming bigger for some time. But, we believe this will only accelerate further from here on due to current pandemic crisis coupled with previous events like NBFC crisis and recent reforms measure like GST.

From a medium to long term perspective, the current phase of disruption shall pave way for accelerated digital adoption by consumers as well as enterprises. We see telecom, internet economy, ecommerce, technology vendors etc to benefit from this disruption. On the contrary, this disruption could rewrite the business and operating models of some of the disrupted industries such as retail, real estate etc. and as portfolio managers, we are cognizant of the risks of disruption as well. Another long term theme is that of diversification of the global supply chain due to ‘China + 1’ strategy which could be adopted by corporates as well as economies. Over medium to long term many sectors could benefit if global investments could be wooed in. We believe that Specialty chemicals to be one of the winners as this sector is already a part of global supply chain and it could grow by winning more orders.

As mentioned earlier, we believe that the theme of the strong becoming stronger will continue to evolve and the disruption will provide a fillip and also likely accelerate this theme. So dominant companies in sectors such as financials, staples, discretionary, telecom, technology etc are likely to gain disproportionately as a result of this disruption. In financials we reckon it will be the large private banks and select NBFCs could gain (due to strong capital position, granular liability franchise, diversified asset base and digital adoption etc) while in technology, the tier-1 players shall benefit owing to vendor consolidation trends and superior digital capabilities. In sectors that are prone to maximum disruption, it would be the market leaders who would benefit disproportionately due to market consolidation, balance sheet strength and technological investments. This will be visible in sectors retail (QSR, multi-brand and single brand retail), travel / hospitality, multiplex and to a large extent in the real estate segment.

What are the broad characteristics of the companies which are able to grow their profits / earnings much faster than other companies?

- Ability to create niche for themselves even in the competitive industry

- Ability to create strong distribution network

- Management Quality with focus on sustainable earnings growth

- Efficient allocation of capital and other resources

- Strong Balance sheet

- Sector Consolidation and dominance in the sector

A typical good investable company will have many of the above characteristics.

We have seen that equity schemes with concentrated portfolios delivered superior returns during recoveries from deep market correction (e.g. Apr 2009 to Apr 2012). Do you think that focused schemes have the potential of generating superior alphas compared to more diversified schemes this time also?

The nature of crisis in FY08-09 (GFC) vs current time (Coronavirus Pandemic) is different. The impact on sectors/companies would be different then and now. In the post recovery phase too, the impact on sectors/stocks would be different. So, just having a concentrated portfolio may or may not generate superior return.

But what is the common that the impact of these disruptions is large and widespread and has the power to dislocate the economy as well as corporate sectors meaningfully. We, therefore, believe that the polarisation trend which we have been witnessing for some time will become stronger. A concentrated portfolio of companies which are dominant in their sectors and/or gaining market share and has sustainable profitability and if available at reasonable valuations, will have potential to generate better return.

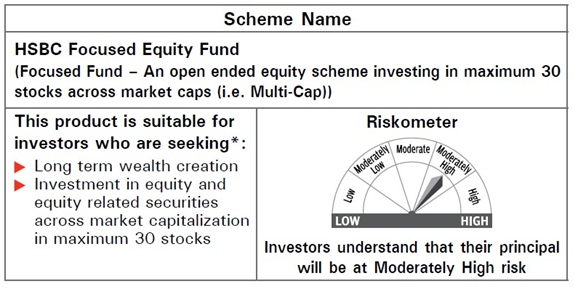

You are launching HSBC Focused Equity Fund NFO shortly. What is the investment strategy of this scheme?

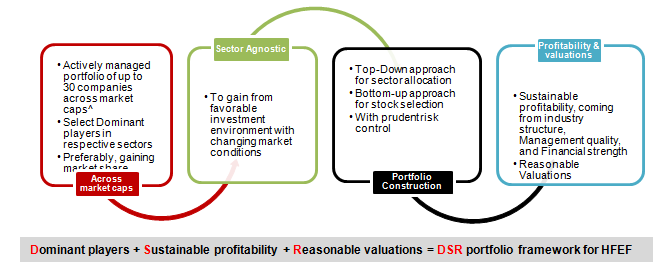

HSBC Focused Equity Fund (HFEF) is all about investing in dominant players with sustainable profitability available at reasonable valuations. As the name suggests, Focus theme is essentially investing in limited number of high conviction companies. Maximum no. of stocks in the portfolio would be limited to 30 stocks but they would be spread across sectors as well as market capitalization.

We would focus on select dominant players in their sectors and preferably companies which are gaining market share. We believe that these companies can grow faster than the market and hence can show better growth.

Apart from above, we may also look for companies that is expected to demonstrate resilience in their earnings leading to lesser cut in earnings in the current crisis.

In addition, we are moderately positive on companies which would be beneficiaries of a benign crude oil price environment as well as on the beneficiaries of the global supply chain diversification.

HSBC Focused Equity Fund: Investment Strategy

What will be the stock selection criteria in this scheme? What is the investment process?

We have a process oriented investment approach and we will be using the same investment process in managing the fund.

We look at the universe for potential outliers. We generate ideas based on above and also based on the current dynamics of the market. Those ideas are then analyzed through the lens of our profitability vs valuation framework. Post that we construct the portfolio based on both Bottom-up implementation of stock ideas and Top-down use for prudent risk control. Then we have a very strong risk management framework where portfolios are continuous monitored and risk are reassessment at the stock and portfolio level.

However, it is not a quant model. Fund manager’s skills are complementary to the process oriented approach. It would the fund manager skills that would be useful in identifying the stocks and sizing them to create a portfolio. But then, again, having a process oriented approach to investment keeps a good discipline and mitigates risks.

Will you invest across market cap segments and industry sectors? Which sectors in your view are likely to outperform over the next 3 – 5 year investment horizon?

Focus Fund aims to invest across market cap and across industry sector. There are companies who are leaders in their respective market or has been gaining market share but since the market itself is smaller they do not fall into large cap category. But that does not make them any less attractive.

Currently we are positive on Consumer staples, Healthcare and Communication services.

Consumer staples

We believe that earnings of the sector would be resilient. The impact of the lock-down will be felt relatively less compared to other sectors given that it is serving basic and essential needs and this would lead to lesser cut in earnings for FY21. Impact of down trading on margins would be partly mitigated due to lower raw material (crude linkage) prices.

From a medium term perspective, the sector is a beneficiary of the corporate tax reform as it will boost earnings and provide additional cushion for the companies to invest back in the business and gain market share.

Healthcare

We are positive on account of the expected resilience in earnings and also ability to retain the demand in the current environment compared to other sectors. Recent approval of facilities by the US FDA will improve the prospects of US business of investee companies.

Domestic business will see a modest growth as chronic segment will be stable but acute segment will show a decline. Stabilisation of raw material supplies from China has eased pressure on raw material sourcing.

Communication Services

Telecom is one sector that will see very limited impact of the lock-down in the country owing to the essential nature of the service. Looking beyond this crisis period, the telecom sector continues to be a beneficiary of consolidation and tariff improvement.

We see profitability of the sector coming back strongly and the post consolidation phase would benefit players who are better positioned on network / spectrum and also with better access and ability to deploy future capital. Our preference is for players with relatively stronger balance sheet and showing better execution on the ground.

Who should invest in this scheme? What should be minimum recommended investment horizon for this scheme? What is your general advice to investors?

Any investor who is not averse to investing in equities and is willing to bear the current short term volatility for reasonablereturnsin medium to long term.

Being a concentrated portfolio, the fund would have moderately higher risk but will also aim to deliver better than benchmark returns by investing in quality companies across market capitalisation. The fund will follow a sector agnostic approach and aims to invest in companies which have potential to deliver higher long term growth.

Investors with moderately high risk appetite looking to benefit from long term wealth creation potential of equities with focused approach can consider this fund.

Looking at the potential upside is like looking at one side of the coin only. Any investor should also look at possibility of losing it principle. By looking at last 39 year of BSE Sensex data, we have observed that longer the investment horizon, lower is the risk of losing money in equity market. Hence, we recommend investor in to invest in equities with at least 5 year of investment horizon.

Source: BSE, CRISIL Research, past performance may or may not sustain, past performance does not guarantee future performance. Data as at May 2020

Daily rolling returns for respective holding periods since 1979. For instance, in case of 15-year monthly rolling returns, there will be 9468 return periods. The first return period will be June 1979 to June 1994 and last return period will be May 2005 to May 2020.

* Positive returns – The number of investment periods during which returns have been positive. For example, where investment returns have been computed for a 15-year rolling period, 9468 out of 9468 days offered positive returns.

We generally advise investor to invest through SIP as these takes away the risk of daily / monthly volatility in the market. However, there are times like current pandemic crisis, which result into sharp downward market movement. And these are very opportune time to make lump-sum investment in the market.

Mutual fund investments are subject to market risks, read all scheme-related documents carefully.

Recent Interviews

-

In Conversation by Advisorkhoj with Ms Saloni Kapadia Fund Manager The Wealth Company Mutual Fund

Jul 23, 2026

-

In conversation with Mr Gautam Kaul Senior Fund Manager Fixed Income with Bandhan Mutual Fund

Jul 23, 2026

-

Partner Connect by Advisorkhoj with Mr Suresh Royal Rupee MFS Pvt Ltd Tirupathi

Jul 20, 2026

-

In Conversation with Mr Ritesh Pathak Deputy CBO Retail Sales & Passive with Motilal Oswal MF

Jul 13, 2026

-

Partner Connect by Advisorkhoj with Mr Ramu Chellimilla & Mr B G Srinivas Invictus FinServ LLP Secunderabad

Jul 1, 2026

Fund News

-

SBI Mutual Fund launches SBI Balanced Hybrid Fund

Aug 10, 2026 by Advisorkhoj Team

-

Mirae Asset Mutual Fund launches Mirae Asset BSE LargeMid 60 40 Stable Dividend 50 ETF

Aug 10, 2026 by Advisorkhoj Team

-

DSP Mutual Fund launches DSP Nifty 10 Yr Benchmark G SEC ETF

Aug 10, 2026 by Advisorkhoj Team

-

Bandhan Mutual Fund launches Bandhan Contra Fund

Aug 10, 2026 by Advisorkhoj Team

-

Aditya Birla Sun Life Mutual Fund SIF launches Apex Equity Long Short Fund

Aug 10, 2026 by Advisorkhoj Team