Financial Planning in Formidable Forties

This is our 3rd article in the 5 part series. In the earlier two parts, we discussed Financial Planning in the Tantalizing Twenties and Financial Planning in the Thrilling Thirties

You may have been repeatedly told that not having a financial plan is a bad plan. If you do not have a concrete plan lined up by your 40s then you may be preparing for a catastrophe. Now you are in your forties and you have seen a fair share of life. The last two decades have been tumultuous as you have been trying to carve your niche in both, professional world and personal life. The decade of forty brings with it a sense of stability as you are aware of where you stand in life. If you have played your last two crucial decades well then from 40 onwards you can start to relax. If you have been delaying the essentials of financial planning then panic alarms are already ringing. By this decade quite a few goals have been ticked off and a few more remains. The most important and crucial goal is retirement. In this decade your career reaches a peak and begins the preparation to retire. While the motto of the last two decades was to accumulate enough wealth to fulfill the financial goals, the motto for this decade is slightly different.

Retirement

The most important goal of this decade is the retirement planning. Before this you may have invested for retirement making it a secondary investment. However, you cannot afford to do that anymore. If you have not started retirement planning then it is time you started. Give importance to a corpus focused for retirement planning along with retirement solutions like National Pension Scheme. The purpose of a retirement corpus is to ensure you maintain the lifestyle while you do not have steady monthly income. However, in 15 to 20 years the cost of living is going to rise substantially making it necessary for you to create a corpus to sufficiently cover the future cost.

Source: https://www.advisorkhoj.com/tools-and-calculators/future-value-calculator

Given above are approximate figures of present and future cost. The inflation for calculation has been assumed to be 7.5% and the time period is 20 years assuming the investor is currently 40 and will retire at 60. While preparing for your retirement you will have to save approximately four times the amount required in present.

Increase Investment when Income Increases

By the time you have reached the age of forty you probably hold a senior position in an organization or established in your business etc. Along with the seniority comes a steep salary hike or more income. Increase in income could possibly mean availability of funds. Even though your portfolio might be on track with your goals, it is wiser to make additional or fresh investments. There is no harm if you reach your goals a little early or you have excess funds. You could also add the extra fund to your retirement account because that is the goal you should focus on more than anything else. It would be fatal if you let the extra funds lie idle or spend the entire amount because you feel secured about the retirement portfolio. If you are pumping in extra funds you are preparing for possible shortages in future. Hence, use the extra income as boon and channelize them in your portfolio to get maximum returns.

Have an Emergency Fund

Emergency funds are usually created to financially support during a situation that you were not expecting but have to take the financial burden nonetheless. In your 40s you need to start getting more careful about your health since we live in hazardous times medical emergencies are best prepared for. Emergency fund also ensures that you are adequately funded without disturbing the funds for the various goals. In your 40s you and your spouse both are ageing and your parents may need immediate medical attention. An emergency fund should have at least six times your monthly income. While your income increases the corpus in emergency fund should increases as well.

Focusing on Creating Assets

To simply define assets are items that generate current or future cash flow. As the income increases instead of investing in items that maybe subjected to depreciation like car it is wiser to invest in items that appreciates. With excess funds available, as a result of your rising income, it makes sense that you invest in these assets. If you have been planning to buy a second home it may be a good idea with the current rise in your income as it is an asset investment and scope for appreciation is higher. An asset like property can also create income at regular intervals in the form of a rent. The closer you get to retirement it is better to reduce your debts. Either pay off your home loan or keep it to the minimum loan payment so that you can continue to get the tax exemptions U/S 8oC. Tangible assets along with the corpus created are what you have to rely on when the regular income stops after retirement.

Asset Allocation

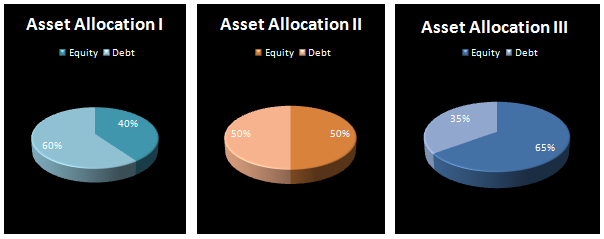

Asset Allocation is that aspect of your portfolio that you have to keep revisiting continuously to get maximum returns. The new decade of 40s marks that time that you have to revisit and rearrange your asset allocation. It is needless to say that the asset allocation that worked in your 30s may not work in your 40s. Hence, given below are some illustrations of possible asset allocation strategies that you can employ.

In ‘Asset Allocation I’ the risk has been taken to be low and investment horizon is 2-5 years. The shorter is the horizon the lesser is the emphasis on equities and higher on debts. In ‘Asset Allocation II’ risk is medium and investment horizon is 5-10 years. These prerequisites portray asset allocation as 50% in Equities and 50% in Debts. In ‘Asset Allocation III’ the investment horizon is above 10 years and hence the focus is on equity investments and lesser on debt investments. The variables of asset allocation are bound to change with a change in your risk taking appetite and investment horizon. To find out more about Asset Allocation use this calculator. To get your asset allocation right and review of your existing portfolio, a advice from a qualified financial advisor is always recommended.

Conclusion

Your forties are that decade that provides security and brings you a decade closer to your retirement. It is that decade that should gear you up to take your retirement goal seriously. Forties allows you to lead a fulfilling life both professionally and personally without the uncertainties that characterize your twenties and thirties. So gear up for this decade and walk another decade by financially securing your life.

Queries

-

What is the benefit of mutual fund STP

Aug 29, 2019

-

How much to invest to meet target amount of Rs 2 Crores

Aug 26, 2019

-

Can I achieve my financial goals with my current mutual fund investments

Aug 24, 2019

-

Can you tell me return of various indices

Aug 19, 2019

-

What would be the post tax return on different investments

Aug 18, 2019

-

Which Principal Mutual Fund scheme will be suitable for my retirement corpus

Aug 16, 2019

-

What is the minimum holding period for availing NCD interest

Aug 4, 2019

Top Performing Mutual Funds

Recommended Reading

Fund News

-

SBI Mutual Fund SIF launches Magnum Equity Ex Top 100 Long Short Fund

Aug 7, 2026 by Advisorkhoj Team

-

Axis Mutual Fund launches Axis Nifty Energy Index Fund

Aug 7, 2026 by Advisorkhoj Team

-

Kotak Mahindra Mutual Fund launches Kotak Diversified Equity All Cap Omni FOF

Aug 5, 2026 by Advisorkhoj Team

-

Franklin Templeton Mutual Fund launches Franklin India Short Term Fund

Aug 5, 2026 by Advisorkhoj Team

-

Edelweiss Mutual Fund launches Edelweiss Nifty REITs and Realty Index Fund

Aug 5, 2026 by Advisorkhoj Team