Choosing the Best Term Life Insurance Plan in 2014

Term insurance policies are becoming increasingly popular in India, and for a very good reason. A term plan is the purest form of insurance and is a straightforward protection policy. The premium of term insurance plans is much less than traditional insurance cum savings products like endowment and money back plans, and it leaves the policy holders with a much larger investible surplus that they can invest in investment products like mutual funds that give much higher returns in the long term. The first step in buying a term insurance plan is to determine the amount of cover. The insurance cover, also known as sum assured, should be adequate to cover the following:-

- Repayment of the entire outstanding debt (e.g. home loan, car loan etc.) of the insured

- After debt repayment, the insurance cover should have surplus funds to generate enough monthly income to cover all the living expenses of the dependents of the insured, after factoring in inflation

- After debt repayment and generating monthly income, the insurance cover should also be adequate to meet future obligations of the insured, like children’s education, marriage etc.

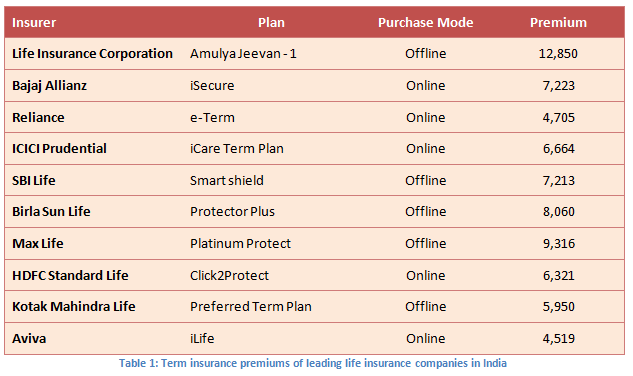

For more details on determining the amount of life insurance cover, please refer to our article, How much life insurance is adequate. Once we have determined how much cover is required the next step is to select the right term insurance plans. Normally, as insurance buyers, we give a lot of importance to lowest premiums, but there are other important factors in choosing the right term insurance plan. In this article, we will review the term plan premiums and some other important metrics of the top life insurers in India. For our analysis, we have assumed that the insured is a 30 year old non smoker male. The table shows the approximate term insurance premiums for a sum assured of Rs 50 lakhs and a policy term of 20 years. For our analysis we have considered a mix of offline and online term plans.

We can see in the above table that Life Insurance Corporation of India (LIC) has the highest premium, while some of the private insurers have much lower premiums. Also you can see that the offline plans have higher premiums than online plans. So, should one buy a term insurance policy that has the lowest premium? A cheaper policy is no good, if the life insurance company for some reason or another cannot fulfil the claim of the insured in the event of an untimely death. It defeats the very purpose to buying life insurance. Even if the life insurer fulfils the claim, if it takes a very long time to fulfil the claim it is certainly not a desirable situation for family of the insured to be in. There are two important metrics, which insurance buyers must evaluate while selecting a life insurer:-

Claims Settlement Ratio:

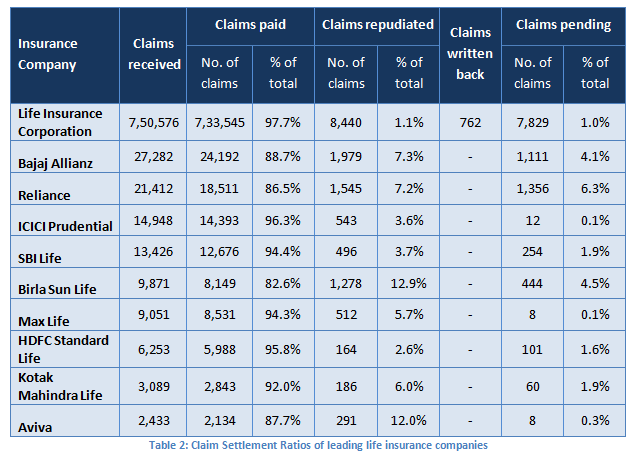

This is the single most important metric to consider when choosing a life insurance provider. The metric tells us how many insurance claims were made to the insurer in a financial year and how many were fulfilled or paid, and gives you a broad sense of the probability that your insurance claim will be paid. This metric is critical in determining the reliability of the life insurance company. The table below shows the claims settlement ratios for the some of the biggest life insurers in FY 2012 – 2013. You can find the same information for all insurers in the death claims table in the IRDA annual report or on the website of some of the life insurance companies.

We can see from the table above that while LIC had the highest term insurance premium (refer to Table 1), it also has the highest claim settlement ratio (97.7%). ICICI Prudential and HDFC Standard also have claim settlement ratios higher than 95%. You can see from Tables 1 and 2 that, while Aviva has the lowest term insurance premium among the insurers in consideration, its claims settlement ratio is also one of the lowest. What is a good claims settlement ratio? There is no straightforward answer. However, it suffices to say that, a repudiations percentage of more than 10% warrants further analysis. There may be genuine reasons for repudiations to be high. Therefore, one needs to look at this data over a 4 to 5 year period. If repudiations are generally low over a 4 to 5 year, with occasional spikes, one may treat the spike as an outlier. However, if the repudiations are consistently high, then it is a cause of concern. In my opinion, as far as term insurance is concerned, claim settlement track record is more important than cheaper premiums. One should always select a life insurer with an excellent record of claims settlement.

Duration wise settlement of death claims:

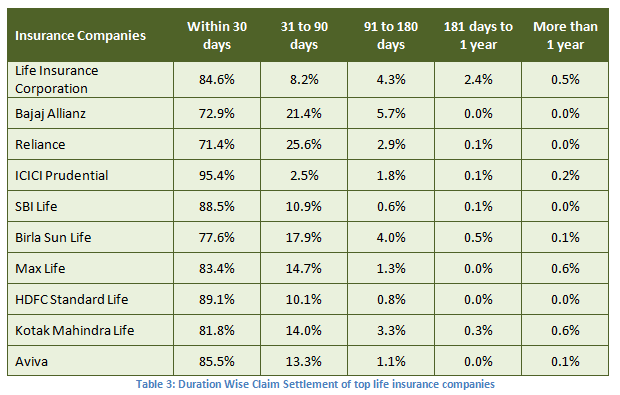

This is the second most important metric in choosing a life insurance provider. Duration wise settlements of death claims help insurance buyers evaluate the efficiency of the claims settlement process. Higher the percentage of claims settled in the quickest possible time, the better is the experience for the family of the insured, in the event of an untimely death of the insured. The table below shows the percentage of claims settled in less than 30 days, between 31 to 90 days, between 90 days and 180 days, between 181 days and one year, and more than one year by some of the biggest life insurers in FY 2012 – 13 (you can find the same for all insurers in the duration wise settlement of death claims table in the IRDA annual report, available for download on the IRDA website)

Conclusion

Choosing the right term insurance plan is an important step in your financial planning process. You should compare various policies and insurers before selecting a term policy. You should select a plan with the lowest premium from an insurer with an excellent track record of settling claims. It is important here to reiterate the purpose of life insurance. Life insurance should always been seen as protection for your family, in the event of untimely death. In this article, we have discussed some important considerations for choosing the right term plan. You should engage your insurance adviser to help you select the best term plan, based on these considerations.

Queries

-

What is the benefit of mutual fund STP

Aug 29, 2019

-

How much to invest to meet target amount of Rs 2 Crores

Aug 26, 2019

-

Can I achieve my financial goals with my current mutual fund investments

Aug 24, 2019

-

Can you tell me return of various indices

Aug 19, 2019

-

What would be the post tax return on different investments

Aug 18, 2019

-

Which Principal Mutual Fund scheme will be suitable for my retirement corpus

Aug 16, 2019

-

What is the minimum holding period for availing NCD interest

Aug 4, 2019

Top Performing Mutual Funds

Recommended Reading

Fund News

-

Motilal Oswal Mutual Fund launches Motilal Oswal Nifty Metal ETF

Aug 3, 2026 by Advisorkhoj Team

-

Motilal Oswal Mutual Fund launches Motilal Oswal Nifty Oil and Gas ETF

Aug 3, 2026 by Advisorkhoj Team

-

Kotak Mahindra Mutual Fund launches Kotak Nifty Bank Index Fund

Aug 3, 2026 by Advisorkhoj Team

-

Invesco Mutual Fund launches Invesco India Nifty Bank ETF

Jul 28, 2026 by Advisorkhoj Team

-

Invesco Mutual Fund launches Invesco India BSE Sensex ETF

Jul 28, 2026 by Advisorkhoj Team