How to avoid rejection of life insurance claims

Life insurance is essential for the financial protection of your family in the event of an unfortunate death. However, insurance buyers often focus on other considerations like tax savings, premiums or investment returns, and ignore this important objective. If death claim of the insured is rejected, then the whole purpose of life insurance is defeated. In this article, we will discuss some important steps that you should be diligent about, when buying your life insurance policy. There are several reasons why life insurance companies reject death claims. We will discuss them in our article today. It is also a fact that, some life insurance companies have a better track record of settling death claims than others. Here are some important steps that insurance buyers should be diligent about, when buying their life insurance policies and even during the policy term:-

Fill out the policy proposal form yourself:

Insurance buyers are sometime too busy to fill out the proposal form themselves. They just sign the form and ask their insurance agent to fill out the form. This is a mistake. After all, life insurance is a critical requirement in our lives. If the agent does not fill out correct details about you, then the claim, in the event of an untimely death may get rejected, if the insurance company determines that the information in the form is incorrect. You should always ensure that you fill the proposal form yourself. You should make sure that, you fill in correct information like your age, height, weight, occupation, income, existing policy details and other details. If you have not taken your weight for some time, it is always a good idea to know what your actual weight is and fill it our correctly in the proposal form. Sometimes we do not reveal the details of other life insurance policies we hold because it takes a bit of an effort to collate all the details about these policies. However, we should furnish all these details in our proposal form. If you need clarifications then you should consult with your insurance adviser. Even if the insurance agent fills out the proposal form for you, you should peruse the form to verify that all the details are correctly filled out in the form. You should pay careful attention to the medical history section in the proposal form and ensure that all the information is correctly stated. Even if we exercise adequate diligence in filling the proposal form, errors are still possible. You should take a photocopy of the proposal form submitted to the insurance company, and verify the details again. If you come across any discrepancy, you should immediately notify the insurance company for rectification.Do not hide medical history:

Sometimes the insurance buyer or proposer does not disclose correct information about the medical conditions of the proposer and his or her family. Medical conditions like heart disease, diabetes, asthma, chronic kidney disease etc of both the proposer and his or her family must be disclosed. Sometimes we do not disclose the correct information because we fear that the premiums may go up. It is true that, the insurance company will compute the premium based on the medical history of the proposer and / or his or her family. If the medical history is unfavourable, it is quite likely that the premium will go up. But isn’t it better to pay a slightly higher premium, than have your claim arising from an untimely death, rejected. If the insurance company determines that the medical history is not disclosed correctly, then it may reject the claim. If you have a habit of consuming of alcohol or tobacco or both, you should declare it honestly, otherwise your claim may be rejectedDo not avoid medical tests:

Some life insurance companies may require the insurance buyers or proposers to undergo medical test for certain policies, like for example, term insurance plans. The proposers sometimes try to avoid medical test, either because they do not want to spare the time, or they fear that the tests may uncover a medical condition which may be both emotionally distressful and may cause the insurance company to raise the premium. However, it is not wise to avoid medical tests. Probably everything will be fine in the medical tests, and even if some medical conditions are identified, it will be prudent from a health perspective to undergo treatment for such conditions. From a life insurance perspective, the possibility of claims being rejected on account of pre-existing medical conditions reduces, if the proposer undergoes the medical test.Select an insurance company with good claims settlement track record:

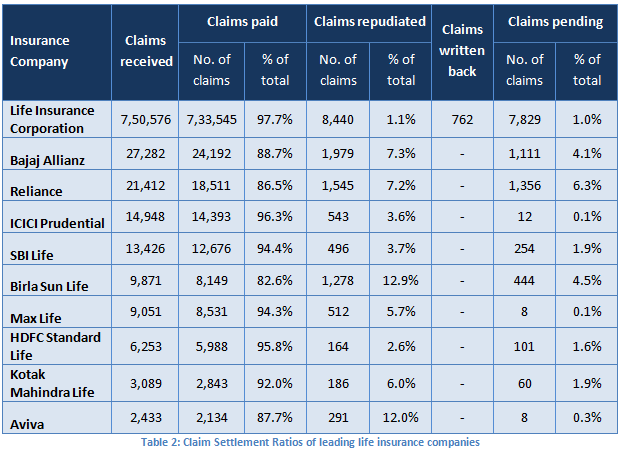

Claims settlement ratio is an important metric to consider when choosing a life insurance provider. The metric tells us how many insurance claims were made to the insurer in a financial year and how many were fulfilled or paid, and gives you a broad sense of the probability that your insurance claim will be paid. This metric is critical in determining the reliability of the life insurance company. The table below shows the claims settlement ratios for the some of the biggest life insurers in FY 2012 – 2013. You can find the same information for all insurers in the death claims table in the IRDA annual report or on the website of some of the life insurance companies.Make sure your nominees are updated in your policy:

Another reason from problems in realization of death claims is that, the beneficiary of your life insurance policy may not be updated in the records of the insurance company. Often we buy our life insurance policy, when we are single and name our parents as nominee. If, however, your personal situation changes and you want your spouse or child to be the beneficiary of your life insurance policy, you should make a written application, as per the procedures of the insurance company to ensure that the correct nominee is updated in the records of the insurance company. If your nominee passes away before a death claim arising, a lot of legal processes need to completed, which consume both time and effort, before your legal heir can receive the claim. Therefore, it is very important that you make sure that your nominee is updated in the records of the insurance companyDo not let your policy lapse:

The insurance company will reject your claim, if your life insurance policy has lapsed before the claim. Therefore, you should always pay your premiums on time, so that your policy does not lapse. Usually insurance companies allow a grace period in which the premium must be paid, if not paid within the due date. If you fail to pay your premium within the grace period, your policy will lapse. The consequence of a policy lapsing is even more grave, if you have a term insurance policy, because your nominee or beneficiary will not get anything if your term insurance policy lapses. Pay careful attention to premium payment. Do not just rely on your insurance agent to tell you when your premium is due. Make a note in your personal calendar to remind you when your life insurance premium is due and make sure you pay the premium promptly, whenever it is due.

We can see from the table above that while LIC has the highest claim settlement ratio (97.7%). ICICI Prudential and HDFC Standard also have claim settlement ratios higher than 95%. You can see from Tables 1 and 2 that, while Aviva has the lowest term insurance premium among the insurers in consideration, its claims settlement ratio is also one of the lowest. What is a good claims settlement ratio? There is no straightforward answer. However, it suffices to say that, a repudiations percentage of more than 10% warrants further analysis. There may be genuine reasons for repudiations to be high. Therefore, one needs to look at this data over a 4 to 5 year period. If repudiations are generally low over a 4 to 5 year, with occasional spikes, one may treat the spike as an outlier. However, if the repudiations are consistently high, then it is a cause of concern. In my opinion, as far as term insurance is concerned, claim settlement track record is more important than cheaper premiums. One should always select a life insurer with an excellent record of claims settlement.

Conclusion

Life insurance is one of the most important elements of your financial plan. We must remember the essential purpose of life insurance. Life insurance is first and foremost a protection for your family, in the event of untimely death. Tax saving, return on investment and premium rate (as a percentage of sum assured) are only secondary considerations. In this article, we have discussed some important, but simple steps that insurance buyers should be diligent about when buying their life insurance policies, in order to ensure that the claim in the event of an untimely death is fulfilled by the insurance company. If you pay due attention to these steps, then you will be able to provide your family adequate financial security, even in an unfortunate event.

Queries

-

What is the benefit of mutual fund STP

Aug 29, 2019

-

How much to invest to meet target amount of Rs 2 Crores

Aug 26, 2019

-

Can I achieve my financial goals with my current mutual fund investments

Aug 24, 2019

-

Can you tell me return of various indices

Aug 19, 2019

-

What would be the post tax return on different investments

Aug 18, 2019

-

Which Principal Mutual Fund scheme will be suitable for my retirement corpus

Aug 16, 2019

-

What is the minimum holding period for availing NCD interest

Aug 4, 2019

Top Performing Mutual Funds

Recommended Reading

Fund News

-

Invesco Mutual Fund launches Invesco India Nifty Bank ETF

Jul 28, 2026 by Advisorkhoj Team

-

Invesco Mutual Fund launches Invesco India BSE Sensex ETF

Jul 28, 2026 by Advisorkhoj Team

-

DSP Mutual Fund launches DSP BSE MidSmall Private Banks ETF

Jul 28, 2026 by Advisorkhoj Team

-

SBI Mutual Fund launches SBI Nifty Midcap 150 Momentum 50 ETF FOF

Jul 27, 2026 by Advisorkhoj Team

-

Edelweiss Mutual Fund launches Edelweiss BSE LargeMid 60 40 Stable dividend 50 ETF

Jul 27, 2026 by Advisorkhoj Team