Tax saving beyond the Section 80C limit

Section 80C of Income Tax Act allows tax payers to claim deductions from their taxable income (up to Rs 1 Lakh) by investing in certain instruments. However, many tax payers are not aware that, there are other sections of the Income Tax Act that allows tax payers to claim further deductions from their taxable income, beyond the 80C limit of Rs 1 lakh. In this article, we will discuss ways to save taxes beyond the Rs 1 lakh of Section 80C.

Interest Paid on Home Loan:

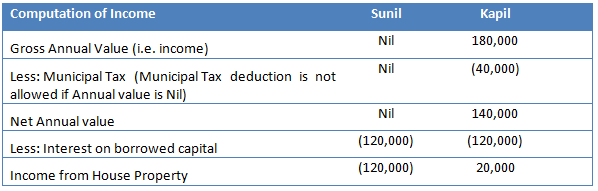

Under Section 24, up to Rs 1.5 lakhs per annum can be claimed as deduction from your taxable income, on account of interest paid on home loan, for a self occupied property. If the property is rented out, then there is no limit and the total interest paid can be claimed as deduction. However the rental income will be added to the “Income from other sources” in your Income Tax return, for the purpose of tax calculations. To illustrate this with an example, let us assume Sunil and Kapil have both bought identical apartments on loans. Annual interest on home loan, for both, is Rs 120,000. Sunil occupies the apartment, while Kapil has rented it out at Rs 15,000 per month. Sunil pays municipal taxes of Rs 15,000 per annum, while Kapil pays municipal taxes of Rs 40,000. Let us now examine the tax consequence for Sunil and Kapil

We should reiterate that, the deduction for interest paid on home loan is over and above the deduction claimed for principal payment under 80C provisions.![]()

Premium paid for Medical Insurance:

Medical insurance premium for self, spouse, dependent children and parents are eligible for deduction under Section 80D of the Income Tax Act. The maximum allowable deduction is Rs 15,000 for self, spouse and dependent children. The applicable deduction for senior citizens is Rs 20,000. If an individual pays for medical insurance of parents who are senior citizens, then he or she can claim an “additional” maximum deduction of Rs 20,000. However, if the parents are not senior citizens, then a maximum of Rs 15,000 can be claimed as additional deduction. Therefore the total amount of the deduction the individual claim for medical insurance for self, spouse, dependent children and senior citizen parents is Rs 35,000.Treatment of specified diseases:

Medical treatments for specified serious diseases, like cancer, AIDS, Parkinson’s disease, chronic kidney failure etc, either for self or dependents are eligible for deduction under Section 80DDB. For clarification on specified diseases, you should refer to the relevant section (80DDB) of the Income Tax Act or consult your tax consultant. Actual expenses or Rs 40,000, whichever is lower, is eligible for deduction under this section. For senior citizens the upper limit is Rs 60,000.House Rent Allowance:

If you are paying rent for your accommodation, you should claim house rent allowance from your employer, if allowed under your company’s policy. This will reduce your taxable income and your tax obligation. If you are self employed or a salaried individual who does not receive House Rent Allowance (HRA) from the employer, do not despair. You can still claim deduction for rent paid in respect of the property occupied for residential use, under Section 80GG of the Income Tax Act. Maximum allowable deduction is the least of the following:-- 25% of your total income

- Rs 2,000 per month

- Rent paid in excess of 10% of total your income

However in order to avail of this benefit, the tax payer should satisfy three conditions:-

- The tax payer must pay the rent for the house he or she lives in

- He or she should not own or occupy any other residential accommodation

- The tax payer’s spouse or children should not own any residential accommodation in the city where the tax payer resides

Leave Travel Allowance:

If allowed within your company’s policies, use your Leave Travel Allowance for your holidays, which is available twice in a block of four years. If you do not avail of the Leave Travel Allowance, your employer will be pay it to you in your monthly pay cheque as part of your salary, after deducting tax at source at your applicable income tax slab rate. To claim deduction on taxes, you will be required to furnish copies of tickets as proof to claim the tax deduction. If you are been unable to claim the benefit in a particular four year block, you could carry forward one trip to the succeeding block of 4 years, but make sure you claim it in the first calendar year of that block.Repayment of Loan taken for higher education:

Interest paid on educational loan for higher studies qualifies as deduction under Section 80E of the Income Tax Act. The entire amount of interest paid in the year is eligible for deduction. There is no upper limit. However, there is no tax benefit for principal repayment. One should note that this benefit not only extends to the loan taken by the tax assessee, but also towards loans for higher education of spouse and children. Higher education is defined as means any course of study pursued after passing the Senior Secondary Examination or its equivalent from any school, board or university recognized by the Central Government or State Government or local authority or by any other authority authorized by the Central Government or State Government or local authority to do so. The deduction is available for a maximum of 8 years or till the interest is paid, whichever is earlier.Deduction for Charitable Donations:

Section 80G of the Income Tax Act, allows 50% or 100% of donations, depending on the clauses specified in this section, for deduction from taxable income. For details you should refer to the relevant section of Income Tax Act or consult your tax consultant. Please note that donation made in kind is not eligible for deduction under Section 80G. In order to claim this deduction, the donor needs to furnish stamped receipt issued by the trust, mentioning the name of the donor, name and address of the trust, the amount donated (in figures and words) and the registration number of the trust.Wait for a few more days:

This is a special year. The Union Budget is just around the corner. The Government may announce new tax amendments, new tax deductions and exemptions. You should plan your tax savings after the Budget is presented in the Parliament, to take advantage of any new tax benefit announced by the Government

Conclusion

In this article, we have discussed various tax-saving opportunities beyond the 80C limit of Rs 1 lakh. You should ensure that you understand the different provisions of tax saving in the Income Tax Act, and see if these provisions apply to you. If the Government announces new tax benefits in the upcoming Budget, you should go through them carefully, so that you can maximize your tax savings. Maximising tax savings puts more cash in our hands that we can use to invest in our future. However, we should be careful in interpreting the various provisions under the different sections of the Income Tax Act and in case of any confusion consult a chartered accountant or tax consultant.

Queries

-

What is the benefit of mutual fund STP

Aug 29, 2019

-

How much to invest to meet target amount of Rs 2 Crores

Aug 26, 2019

-

Can I achieve my financial goals with my current mutual fund investments

Aug 24, 2019

-

Can you tell me return of various indices

Aug 19, 2019

-

What would be the post tax return on different investments

Aug 18, 2019

-

Which Principal Mutual Fund scheme will be suitable for my retirement corpus

Aug 16, 2019

-

What is the minimum holding period for availing NCD interest

Aug 4, 2019

Top Performing Mutual Funds

Recommended Reading

Fund News

-

Gold's Recent Correction: Keeping the Long-Term Perspective

Jul 22, 2026 by Quantum Mutual Fund

-

AlphaGrep Mutual Fund launches AlphaGrep Flexi Cap Fund

Jul 21, 2026 by Advisorkhoj Team

-

ICICI Prudential Mutual Fund launches ICICI Prudential BSE Insurance ETF

Jul 20, 2026 by Advisorkhoj Team

-

HDFC Mutual Fund launches HDFC Nifty Metal ETF FOF

Jul 20, 2026 by Advisorkhoj Team

-

HDFC Mutual Fund launches HDFC Nifty Metal ETF

Jul 20, 2026 by Advisorkhoj Team