How much health insurance is adequate

With the rising cost of healthcare in our country, health insurance is an essential investment in ensuring our family’s critical healthcare needs. Healthcare costs in India are increasing at a distressing rate. Based on some estimates, the annual healthcare inflation is in range of 15 – 25%. A hospitalization for a serious illness can cost Rs 5 lakhs or above. In the absence of health insurance, a serious illness in your family can cause financial distress or leave a big hole in your hard earned savings, at a time when you least expect it. However, an important question as far as health insurance is, like how much health insurance or Mediclaim cover, do you need? I have seen some financial advisers suggesting Rs 3 lakhs Mediclaim cover, others suggesting Rs 5 lakhs and some others suggesting even more, up to Rs 10 lakhs Mediclaim cover. While all of them may be right, it is almost next to impossible to generalize how much health insurance cover you need. Health is a very personal aspect of our lives, and it is very difficult to apply a rule of thumb, as to how much health insurance you need. However, there are several factors that can help you determine, how much Mediclaim cover you need. We will discuss these factors in this article.

How much can you afford:

This is the most important consideration. How much you can afford, depends on your income. Your health insurance adviser may suggest Rs 10 lakhs Mediclaim cover based on a variety of factors, but if you cannot afford to pay the premium for that amount of Mediclaim cover based on your annual income then, you will simply have to settle for a lower Mediclaim cover. Life insurance, retirement planning, children’s education and other long term financial goals, are all important financial planning objectives. What you need to have, is a balanced approach towards all these important objectives, including health insurance or Mediclaim. However, health is the most important aspect of life. Nothing is more important. Therefore, you should give it the due importance as far financial planning is concerned. But how do you deal with conflicting priorities? You need to exercise prudence based on your past experience and take a well informed decision, after comprehensively factoring in various considerations. This is where a financial planner or adviser, who evaluates and manages the entire spectrum of your insurance and investment needs, is more useful.Where do you live:

If you live in a small or mid-sized town, then the hospitalization for a major illness can cost you up to Rs 2 – 3 lakhs. If you live in a large city, then hospitalization costs for a major illness can go up to Rs 4 – 5 lakhs. You should choose your Mediclaim cover, based on estimated expenses for major illness. Where you live, is obviously an important consideration.How much cover does your employer’s group health insurance plan provide:

It is quite common for employees, covered under their employer’s group health insurance plan, not to buy additional individual Mediclaim. But is the cover provided under your employer’s group health insurance plan adequate? The group health insurance plans of many companies provide a cover of Rs 2 lakhs. But it may not be enough. As discussed above, if you are living in a metro city, a major illness in your family can cost you Rs 4 – 5 lakhs. You should check what kind of benefits your employer’s group insurance policy offers. Check, what is the total amount and nature of illnesses that your company’s group insurance covers. Does the policy cover your spouse, children, parents and other dependents? If your company’s group insurance is not adequate for your needs, then you should buy additional Mediclaim to protect your family’s healthcare needs.What is your family situation:

If you have a family or dependents to take care of, your health insurance needs will go up. You should always ensure that your entire family is covered in your health insurance policy. If you are newly wed or have dependent parents, make sure that your spouse and your parents also have Mediclaim cover. However, if you have dependents it does not mean that you have to buy Mediclaim policies for each one of your dependents. The probability of all your family members getting hospitalized in the same year is low. Therefore, if you have a family, it makes more sense to buy a family floater plan. In this type of plan, the entire family is covered for the amount they share and the benefit is that, per person premium is lower compared to the scenario if they would have taken individual plans. Please read our article, Which health insurance plan makes more sense: Individual Mediclaim or Family Floater. Having said that, there is no denying that, your healthcare costs will go up, once you have family and dependents. Therefore, you should increase your Mediclaim cover once you have a family. How much you need to increase, depends from situation to situation. For example, if you are planning to start a family, the cost of maternity and childcare should be estimated and added to your cover. If your dependents have pre-existing medical conditions, then you should estimate the associated costs and include it in your cover as well. As we had earlier discussed, the amount of cover that you should buy, depends from situation to situation. You are the best judge.Your past experience on healthcare cost:

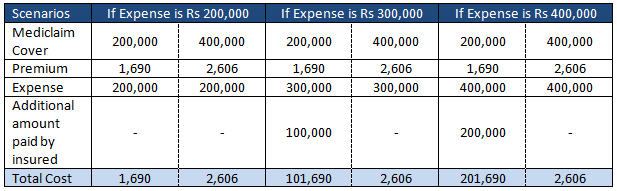

Last but not the least, your past experience on medical costs for you and your family, is one of the most important basis of determining your Mediclaim cover. For example, if you have been spending Rs 4 lakhs every year, for the past few years, on medical expenses like tests, procedures, medications etc for your family, you should opt for a Mediclaim cover of at least Rs 4 Lakhs, if not higher. You should not try to save on Mediclaim premium by opting for a lower cover, because Mediclaim does lower the cost of your family’s healthcare. Let us assume you are 30 years old. We will take two scenarios, one where you take a Mediclaim cover of Rs 2 lakhs and another, where you take a cover of Rs 4 lakhs. Let us now, examine what your cost will be in either scenario, if your medical expense was Rs 2 lakhs, Rs 3 lakhs and Rs 4 lakhs respectively. The table below shows the economics if you opt for a lower cover or higher cover (Rs 2 lakhs versus Rs 4 lakhs Mediclaim cover). Please note that, the premiums in this example are based on Max Bupa Mediclaim plans (premiums of other Mediclaim plans may be different).

Therefore, by paying only Rs 1,000 extra in premium every year, you can save almost Rs 1 – 2 lakhs, as seen in the example above. You should determine your cover, based on your past experience with medical conditions and expenses in your family. You should always err on the side of caution, when making such a determination.

Conclusion

In this article, we had discussed several factors that will help you determine, how much health insurance or Mediclaim cover you need. You should consult with an experienced financial adviser, who will work with you, to determine your health insurance cover and help you select the plan that is most suitable for your needs. If you have adequate health insurance that meets a wide variety of medical needs of your family, you will be free from health related financial concerns and focus on other important financial goals.

Queries

-

What is the benefit of mutual fund STP

Aug 29, 2019

-

How much to invest to meet target amount of Rs 2 Crores

Aug 26, 2019

-

Can I achieve my financial goals with my current mutual fund investments

Aug 24, 2019

-

Can you tell me return of various indices

Aug 19, 2019

-

What would be the post tax return on different investments

Aug 18, 2019

-

Which Principal Mutual Fund scheme will be suitable for my retirement corpus

Aug 16, 2019

-

What is the minimum holding period for availing NCD interest

Aug 4, 2019

Top Performing Mutual Funds

Recommended Reading

Fund News

-

Motilal Oswal Mutual Fund launches Motilal Oswal Nifty Metal ETF

Aug 3, 2026 by Advisorkhoj Team

-

Motilal Oswal Mutual Fund launches Motilal Oswal Nifty Oil and Gas ETF

Aug 3, 2026 by Advisorkhoj Team

-

Kotak Mahindra Mutual Fund launches Kotak Nifty Bank Index Fund

Aug 3, 2026 by Advisorkhoj Team

-

Invesco Mutual Fund launches Invesco India Nifty Bank ETF

Jul 28, 2026 by Advisorkhoj Team

-

Invesco Mutual Fund launches Invesco India BSE Sensex ETF

Jul 28, 2026 by Advisorkhoj Team