ABC of Financial Freedom

Myth about Financial Freedom

You might have read or heard a lot about Financial Planning or Financial Freedom planning. What does Financial Freedom Planning (FFP) mean? When can one claim that one is financially free? Many times we misunderstand "being Debt Free" to "Financial Freedom". But it’s not true. Being debt free is just one aspect of achieving Financial Freedom. Being Debt free requires you to repay all your current liability like Home Loan, Auto Loan, Personal Loan, while Achieving financial Freedom involves being free from working for money.

In one’s life when a person is earning enough to cover his household expenses, insurance premiums and EMIs, we believe that the person is enjoying the financial freedom. While the fact is that, when a person requires working or putting daily efforts to earn the required amount of money to fulfill all the commitments as mentioned above he/she cannot be said to have achieved the financial freedom. So if you are into the job paying you handsome salary or into the business giving you big profits which are enough to take care of all your expenses and pay for liability, you might feel that you are Financially Free. But it’s the biggest "MYTH".

What is Financial Freedom

How can one say whether if he is financially free or not? It’s very easy and simple. While you wake up in to the morning from your bed, ask yourself, is it necessary to go for job or doing business to earn the money you need to survive and to pay for the debt? If your answer is YES, then you are not financially free. But if your answer is NO, then you are undoubtedly financially free.

When we say "Mr. X works for XYZ ltd." who do you think is the employer and who is the employee? Obviously Mr. X is employee and working for his employer which is XYZ Ltd. Similarly when we say "I work for Money" who is the master and who is the employee. In the given situation "I" is the employee working for the "Money" (employer). So unless in your life Money starts working for you, you can’t claim to be financially free.

Passion Vs Profession

In majority case, people often have to sacrifice their passion for their profession. Someone loving a painting or photography or dancing, are not into the profession or being painter, photographer or dancer. Some people are very much interested in doing the social work or want to spend time doing some charity. But all of these people are not able to follow their dream and they work as a job man or business man into the area where they are not much passionate about. Why? Because they are not financially free and that’s why their first priority by force is to "work for Money".

Financial Freedom is the stage which if achieved will allow you to do all those things which you actually wanted to do. So financial freedom is not only about being free from the work but it is allowing yourself to do only those things which you love to do.

Simply putting, you need to build enough assets which can give you regular cash flow for your recurring expenses and periodic requirement of cash for your future goals for life time.

For example, if you need on an average Rs. 600,000 a year for your household and all other expenses. So you need to create an asset which gives you this required sum of Rs. 600,000 to you in terms of interest or rent or royalty or dividend. So if, you build up the corpus of 1 crore and invest in to the bank fixed deposit fetching you 6% per annum interest, then irrespective of you going on job or doing any business you will get the regular income.

Another example is, you try and create the corpus which is enough to buy some property generating the rental income of Rs. 600,000 for you.

In nutshell you need to create a mix of assets weather it is debt, equity, real estate etc. which can give you the required income of Rs. 600,000 in total in form of regular cash flow.

Financial Freedom Fund

For achieving the financial freedom you need to first find out how much corpus you need to build to be able to generate the cash flow which can take care of your current and future requirements for household expenses and other financial goals. We can call that fund the Financial Freedom Fund. The amount of Financial Freedom Fund would vary from person to person based on the different financial requirements of the person.

Mathematically, Financial Freedom Fund is the sum total of the present value of all the current and future expenses and EMIs you are suppose to pay till the life time. Seeking help of the Professional Financial planner is advisable for finding out the required financial freedom fund for you. Once the Financial Freedom Fund is calculated, then you can adapt the most suitable investment strategy to achieve that targeted Financial Freedom Fund at earliest. By doing a little bit of maths with the help of some financial advisor, you will get an idea about the time which is required to build the financial freedom fund.

There are 3 steps to achieve the financial freedom at earliest. It’s called ABC of Financial Freedom.

Assuring

Financial Freedom is not the individual goal or dream it’s a dream for the family. This is the stage where in absence of you, your family also enjoys the same financial freedom.

So, before achieving the Financial Freedom it is very important that you assure the achievement of financial freedom irrespective of you being there or not. Assurance is the stage where an earning person ensures that even in case of the unfortunate demise of himself/herself, the family of his/her will get the Financial Freedom Fund.

As building the Financial Freedom fund is a process which requires the disciplined investment over period of few years, it requires man to work for money till the financial freedom fund is build up. Meanwhile one needs to protect and assure the achieving of financial freedom fund for family against any unforeseen event like the unforeseen demise of the earning member.

Once the Financial freedom fund is calculated we need to find out the gap which is required to bridge between the Financial Freedom Fund and your current assets and investments. And, whatever gap needs to be bridged by the life Insurance for assuring the financial freedom before it’s achieved should be done.

Financial Freedom Fund – your current assets – current life insurance sum assured = Buy Term Plan

Let’s take an example -

In this example to make it simple, I would ignore the inflation and time value of money for the sake of simplicity. Mr. Prem is a family man having wife and a daughter in the family. Some of the data regarding his expense liability and investments are as below.

| Monthly House hold expense: | Rs. 25,000 |

| Amount needed for the higher education of Daughter: | Rs. 500,000 |

| Amount needed for the marriage of Daughter: | Rs 700,000 |

| Current Outstanding Home Loan: | Rs.120,000 |

| Current total investment value: | Rs. 700,000 |

| Life Insurance Sum Assured: | Rs. 300,000 |

In above case, let’s first find out the required Financial Freedom Fund.

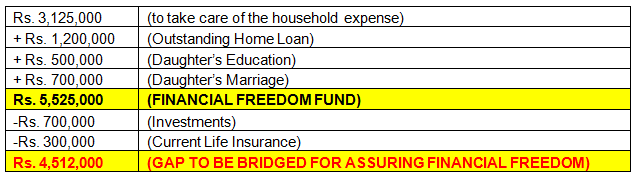

Assuming 8% risk free rate of return, Mr. Prem needs around Rs. 3,125,000 for taking care of his household expenses. Rs. 3,125,000 if invested in FD then it would fetch Rs. 300,000 as yearly interest at 8% rate of the return which is around Rs. 25,000 a month. So, total financial freedom fund is the sum total of Rs. 3,125,000 plus the current and future liability. Once we find out the required amount of financial freedom fund we need to deduct the current value of Investments and existing sum assured from various insurance policies.

In case of Mr. Prem, the Financial Freedom Fund requirement is Rs. 5,525,000 and the value of the investments and the current life insurance is 10.00 lacs. So there is a gap of Rs. 4,525,000 which he needs to build up through regular investments.

Mr. Prem needs to buy additional life insurance policy giving the Sum Assured equal to Rs. 4,525,000. The best choice for assuring the financial freedom through life insurance is to buy the Pure Risk cover also known as the Term Plan. As the term plan is the cheapest way to get the big risk cover which is ideal incase of assuring the financial freedom.

Building Financial Freedom Fund

Once you have assured that your family would certainly get financial freedom even in your absence then we need to take the second and most important step. The step towards achieving the financial freedom is 'Building the Financial Freedom Fund'. The gap between the Financial Freedom Fund and your current value of your investment is the corpus required to be build up over period of time through wise investment strategy.

Continuing with the earlier example, the required Financial Freedom Fund was Rs. 5,525,000 for Mr. Prem, while the value of his current investments was Rs. 700,000. So in case of Mr. Prem we need to add Rs. 4,825,000 in his investment basket. Targeted corpus or Rs. 48.25 Lacs is to be achieved through various investments.

If Mr. Prem’s monthly income is Rs. 36,000 then he would left with the surplus of around 12,000 per month as the household expenses of Mr. Prem is Rs. 25,000/- p.m. Assuming Rs. 4000/- p.m. is the premium he pays for the life insurance policies. Then he will be left with Rs. 8000/- p.m. and existing investment of Rs 700,000 as a investible surplus. Mr. Prem wants to get the Financial Freedom in 12 years.

Based on above details, we need to find out how much rate of return is required on investment to generate the corpus of Rs. 48.25 lacs on existing investment of Rs 7 lacs and additionally investing Rs. 8000/- p.m. in 12 years. Required rate of return in this case would be approx 12.5% CAGR (Compounded Annual Growth Rate).

If Mr. Prem opts to invest into postal recurring deposit giving 8% CAGR return or any other instrument which gives the rate of return lesser than 12.5% CAGR, he would not be able to achieve his financial freedom in 12 years. It would take 16 years instead of desired 12 years to achieve the financial freedom if investments fetch the return of 8%.

Selecting the right asset class based on the required rate of return is very important. A small mistake in opting for the wrong choice might lead to wastage of some of the very important years of one’s life in the slavery of Money, which otherwise could have been spent doing what one actually loves to do the most.

Instead, had Mr. Prem been able to generate the 20% CAGR on his investments, he would have achieved the financial freedom in just around 9 years only.

Best way to build the financial freedom fund is by investing regularly through the Systematic Investment Plan (SIP) route into the Diversified Equity Mutual Funds having a long track record. Investment into the Mutual Funds and that through SIP is considered to be the most ideal way of creating the wealth for any investor. It can generate the better inflation adjusted returns with much lesser risk.

Cashing out

This is the final stage of achieving and enjoying the financial freedom. In the beginning of this stage the Financial Freedom Fund is already built through various investment strategies. One need to re allocate his Financial Freedom Fund into the various investment from which he would get required cash flow on regular basis for one’s needs.

In this stage of life one need to move out his money from the assets which are considered more risky and buy those assets which are less risky and can generate the stable income flow. One can look at the SWP (Systematic Withdrawal Plan) for the need of recurring expenses like household expense, once the financial freedom is built. SWP gives the flexibility to choose the amount of monthly withdrawal according to one’s need.

Have you planned for your financial freedom? If the answer is NO, do it now. Remember, most people don’t achieve the financial freedom because they fail to plan rather than plan to fail.

Conclusion

It’s always advisable to take the help of qualified and experienced financial advisor for creating a roadmap for achieving the Financial Freedom. This article is simplified with the simplest examples to explain the concept and give the overall idea about the process to be followed in brief. While doing it in real life there could be many more things which might need the attention. Qualified and experience financial advisors can help in guiding you to achieve the financial freedom at earliest possible time, based on your current situation and requirement.

Queries

-

What is the benefit of mutual fund STP

Aug 29, 2019

-

How much to invest to meet target amount of Rs 2 Crores

Aug 26, 2019

-

Can I achieve my financial goals with my current mutual fund investments

Aug 24, 2019

-

Can you tell me return of various indices

Aug 19, 2019

-

What would be the post tax return on different investments

Aug 18, 2019

-

Which Principal Mutual Fund scheme will be suitable for my retirement corpus

Aug 16, 2019

-

What is the minimum holding period for availing NCD interest

Aug 4, 2019

Top Performing Mutual Funds

Recommended Reading

Fund News

-

Invesco Mutual Fund launches Invesco India Nifty Bank ETF

Jul 28, 2026 by Advisorkhoj Team

-

Invesco Mutual Fund launches Invesco India BSE Sensex ETF

Jul 28, 2026 by Advisorkhoj Team

-

DSP Mutual Fund launches DSP BSE MidSmall Private Banks ETF

Jul 28, 2026 by Advisorkhoj Team

-

SBI Mutual Fund launches SBI Nifty Midcap 150 Momentum 50 ETF FOF

Jul 27, 2026 by Advisorkhoj Team

-

Edelweiss Mutual Fund launches Edelweiss BSE LargeMid 60 40 Stable dividend 50 ETF

Jul 27, 2026 by Advisorkhoj Team