Financial Glossary starting with Alphabet E

-

External Commercial Borrowing

Let’s assume you suddenly have a guest at home and you are running short of milk to prepare tea. In such a scenario you will have no option but to borrow some from your neighbors, which you can replace later.

Likewise, external means non-Indian / foreign source, commercial would mean engaged in commerce and borrowing means acquire temporarily with a promise to return along with interest.

The concept of this strange sounding term is just as simple.

ECB has become a major source for raising money by large Indian companies in recent years. In comparison with India, interest rates are a lot lower abroad. Therefore, this is the single biggest incentive for companies raising money from overseas. For example, even if a company borrows in the international market at 4% for one year; the cost of borrowing for a similar tenor may be close to 10% in the domestic market.

Companies in India are allowed to borrow from overseas, under certain conditions, through different instruments, with a minimum average maturity of 3 years.

The main objective is to provide companies with an option of low-cost capital.

However, it is not that ECB is always beneficial to a company and the country and does not carry any risk. There is a definite risk involved and those reading newspapers these days should be able to guess easily.

The depreciation of the rupee is the biggest hurdle to this kind of borrowing.

Let’s assume, I have borrowed $100 at 4% and converted it into rupees at Rs. 50 per dollar. Now effectively I have borrowed Rs. 5,000 at 4%. Under normal circumstances, I will have to pay $104 after a year.

So, if the currency were to remain stable, I would have added the interest amount (4% of Rs. 5,000 which is Rs. 200) to the principal to make it Rs. 5,200 and buy US dollars at the rate of Rs. 50 per dollar. This would fetch me Rs. 5,200/Rs. 50 = $104. So far this makes complete business sense. Isn’t it?

But what if the rupee depreciates to Rs. 60? As far as the overseas party is concerned the liability of the Indian company is clearly $104. At $1 = Rs. 60, Rs. 5,200 would only fetch me Rs. 5,200/ Rs. 60 = $ 86.67. There is thus a shortfall of $17.33 ($104 - $86.67).

Now, the cost of buying additional $17.33 at Rs. 60 per dollar turns out to ($17.33 x Rs.60) = Rs. 1,040. Thus, the interest which was planned as Rs. 200 turns out to be (Rs. 200 + Rs. 1,040) Rs. 1,240. Now if you were to calculate the rate of interest the business enterprise in India lands up paying turns out to be (Rs. 1,240 / Rs.5,000) x 100 % which works out as 24.80% which is much more than the 10% interest rates prevailing in the local market. Thus, in this case the borrower would surely feel short changed.

The opposite will be the scenario in case rupee appreciates against the dollar. (Source: Tata Mutual Fund) -

European Woes

Italy recently had its election and quite expectedly the people voted against “austerity” measures. The party who spoke of austerity was vanquished. Unemployment rates have been soaring. The economy is shrinking. Their debt is 150% of their GDP. At such times one of the tools available with government is to tinker with the currency. Unfortunately the Italians cannot do so because they share their currency with other nations of the EURO region.

To understand their predicament one needs to imagine the EURO ZONE as a train.

Now imagine the various countries as the bogies (compartments) of this train. Let’s say the train is trudging along smoothly and all seems well. Suddenly a few of the passengers in the “Italy” bogie fall sick. So, they send a request to the engine driver, via a telecommunication contraption that is fitted in the bogie, to speed up. They need to reach their destination fast as they are feeling unwell.

The engine driver then sends a message to all the other bogies that they have received a “speed up” request from the Italians due to an emergency. On hearing this announcement, the German passengers seated in the German bogie take serious objection. They want to enjoy the journey at a leisurely pace and vehemently object to the “speed-up” suggestion. Their contention being that they had paid a premium for enjoying this leisurely journey and were not prepared to get short-changed. They caution the engine driver that if he were to “speed up”, then they would demand a refund.

The engine driver finding himself in an “impossible” situation is left with no choice but to maintain status quo. The poor Italians are left with no choice but to suffer their ordeal.

One of the Italians regrets his decision to have travelled by train. He feels that had they travelled by their own car, the decision of speeding up would have been theirs. But now since they are a part of the train, they can do little to influence its speed.

The situation in Europe is similar to the story of the Euro train. The common currency, “EURO” is like the train. Some countries like Greece, Italy, Spain, Portugal, and Ireland are not comfortable with the valuation of the EURO (it is exactly how the Italians were not comfortable with the speed of the Euro train). These countries are facing a slow down and need to revive their economy. One of the best ways to do that is to sell more products to the world and reduce debt. And in order to do that, it is vital to devalue the currency. But since the currency (EURO) is common for all the countries, just a handful countries cannot decide about changing the valuation of the EURO all by themselves. This is just like how the Italians in the EURO train failed to “Speed- Up” the train. For countries like Germany and France who are not in a “debt” problem like the Italians and Greeks, a reduction in the value of the EURO works against their interest because it unnecessarily makes their imports more expensive and prices of commodities in general increases. Basically the tinkering of the currency works in opposite ways for two sets of countries. Had Greece or Italy had their own currency, they could have easily devalued their currency to make their exports more attractive. This would have boosted their economy by creating demand and thereby jobs. This would be like their having to travel in their own car instead of being part of a larger train.

Hope the above example would have helped you to understand the currency dilemma that is causing concern to several European countries like Greece, Italy, Spain, Portugal and Ireland who find themselves sinking in debt.

Also, hope this article has also clarified why some other countries of the European Union like Germany do not share the needs of the weaker nations and hence their currency strategy runs opposite to that of the troubled nations. (Source: Tata Mutual Fund). -

Equity/Share

Total equity capital of a company is divided into equal units of small denominations, each called a share. For example, in a company the total equity capital of Rs 2,00,00,000 is divided into 20,00,000 units of Rs. 10 each. Each such unit of Rs. 10 is called a Share. Thus, the company then is said to have 20,00,000 equity shares of Rs. 10 each. The holders of such shares are members of the company and called share holders and have voting rights.

Commonly, you can think of equity as ownership in any asset or Company after all debts associated with that asset or company are paid off. -

Equity Linked Debentures

Equity Linked Debentures

With the high volatility in the equity markets, investors are increasingly looking at financial products which provide stability along with decent returns. ‘Equity-Linked Debentures’ (or ELDs) are products that provide:

Capital protection and a slice of the stock market based returns. So what are ELD’s?

• An ELD is a form of a fixed income product.

• It differs from standard fixed-income product as the final payout is also based on the return of the underlying equity, which can be a set of stocks, basket of stocks or an equity index (all pre-defined)

• It is structured so as to give 100% capital protection with a provision for equity participation.

• Bonds are rated by an accredited rating agency.

Simply put… ‘Equity Linked Debentures’ are popularly known as capital protection funds & give you the upside of equities and protect the downside!

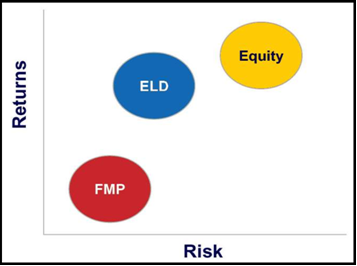

As per the risk return chart above, ELDs offer better returns than FMP at a lower risk than equities.

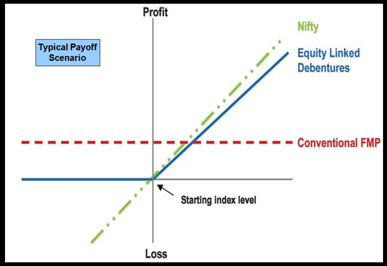

In a typical payoff scenario, as illustrated above, ELDs, on an avarage, offer better retruns than FMPs and even when the Nifty goes down, you recover your principal amount.

The actual terms of these products may vary slightly, but the broad theme of ELD works in this manner…

These bonds are linked to an index like the Nifty or any/group of equity shares. The issuer of bonds invests a pre-determined part of the principal amount collected in fixed income securities like bonds, which provide principal protection.

The balance is invested in call options which provide the exposure to equity or stock index.

For example - The returns are calculated in this manner:

Say, the fund house comes to an initial value of the Nifty, which is often the average of the first three months. Also suppose, the Nifty’s value has been 3,800, 4,000 and 4,200 at the end of months 1, 2 & 3: Their average is worked out to be 3800+ 4000 + 4200/3 = 4,000.

Therefore, the final value is also calculated as the average of the last three months.

Now, if the Nifty’s value closes at 5,000, 5,200, 5,500 in months 34, 35 and 36 respectively, we can calculate the average to 5,233. So, the final Nifty returns come out to 5,233 -4,000/4,000*100 = 30.82 per cent over the three-year period.

The Nifty return, multiplied by the participation ratio (that is pre-decided by the fund) is the final return.

Here’s a new term for you to know - Participation Ratio - is the ratio at which ELD participates in the appreciation of the underlying equity index (say the Nifty). Example - Participation Ratio of 100% implies that a 10% increase in the Nifty will result in a final equity-linked coupon of 10%.

To finally illustrate – Principal remains intact + Equity Market participation = ELD (Equity linked Debentures)

But remember Equity linked debenture schemes do not allow premature exits. All benefits are subject to investment being held till redemption date.

These products, though listed on the exchanges, are a bit illiquid and hence difficult to sell or transfer. In certain cases, the issuer or arranger of the notes may offer to buy back the notes at a certain cut-off.

To Sum Up If investors model and balance their portfolio in a disciplined manner and then hold it long term, they will derive the same benefits as that of an equity linked plan. By investing in these schemes, on the upside, they may get a return related to the appreciation of the Nifty. At worse, the Investor won't lose their capital. (Source: Tata Mutual Fund) -

Exchange Traded Funds

An exchange-traded fund (or ETF) is an investment vehicle traded on stock exchanges, much like stocks. An ETF holds assets such as stocks or bonds and trades at approximately the same price as the net asset value of its underlying assets over the course of the trading day.

Most ETFs track an index, such as the S&P 500 or MSCI EAFE.

By tracking an index, we mean the fund managers attempt to track the performance of the index itself. The value of the investment thus will go up and down in line with the index which it is matching.

ETFs are close cousins of mutual funds. In many respects, ETFs work like mutual funds. For instance, an ETF may provide you with an opportunity to invest in a basket of stocks that reflects an index just like an index-based mutual fund.

Or you may find an ETF that represents a basket of stocks consisting of a particular sector just like a sector-specific mutual fund. Or an ETF based on a specific commodity such as gold just like any gold-oriented mutual fund.

You can make investments in an ETF by buying shares of that particular ETF, which gives you an opportunity to make an ‘indirect’ investment in the basket of stocks or commodities constituting that particular ETF.

But, you may ask, why is it called indirect? That’s because you do not directly own stocks of any company. You just own shares of the ETF which, in turn, holds shares of different companies as your trustee. Investment in just one share of an ETF can give you exposure to an index or a particular sector.

So, if you are investing in a share of an ETF representing a stock market index, then your return would depend upon the rise or fall of that particular index.

Similarly,iIf you are investing in a share of an ETF representing gold, then your return would depend upon the rise or fall in the price of gold.

You should keep in mind that investments in ETFs, in many respects, look like investments in mutual funds but, despite many similarities, ETFs and mutual funds are not one and the same thing.

So how are they different? Mutual funds offer either open-end or closed-end schemes.

ETFs differ from both open-end and closed-end mutual funds in many ways. For example, the shares of ETFs are listed on the stock exchanges, which you can trade at any time, just like any other stock.

But the units of open-end mutual funds are not listed on the stock exchanges. Such units can only be redeemed at the end of the day at their net asset value, or NAV, as disclosed by the mutual fund.

But what about closed ended funds? Sometimes, their units are listed on stock exchanges…

That’s true… but here’s the difference! ETF shares are, in many ways, traded like any other stock listed on stock exchanges. But closed-end funds sometimes trade at a premium to their present NAV and sometimes they trade at a discount, which means that the trading prices may not be fully aligned with their actual worth.

Shares of ETFs, however, trade at a price closer to the price of stocks or commodities represented by them.

To Sum Up - ETFs provide opportunities for indirect investments in a basket of stocks or a commodity. The shares of ETFs represent fractional interest in a basket of stocks or a commodity which that particular ETF holds as a trustee. ETFs are becoming popular because they can be traded like stocks at a lower transaction cost while retaining most of the benefits of mutual funds. (Source: Tata Mutual Fund)

Recent Articles

Top Performing Mutual Funds

Tools and Calculators