Financial Glossary starting with Alphabet P

-

P&L statement and Cash Flow statement - Difference

Let us look at the following examples:-

1) A man trying to swim across a flooded river to grab a huge prize promised to him for doing the feat.

2) A person going hungry for 100 days to win a competition.

3) An employer promising his employee 24 times his monthly salary for a job. But the only catch being that the salary would be paid together at the end of the first year.

4) An organization spends a large sum of money in a brand campaign but does not have enough money left to pay the salaries of the employees.

5) A man buying the best car available but running out of money to buy fuel.

6) A person getting admitted into the best university but having money that would only fund half the course.

In the all the above examples, we have seen that somewhere there dangles an appetizing proposition but the path that is drawn up to make it to the goal is fraught with danger. For example, the man who is crossing the river has little probability to survive till the other end. If he cannot make it, then what is the use of the grand prize?

Similarly, the person going hungry for 100 days may not live to enjoy the fruits of his perseverance. The employer who promises double salary to the employee takes the thunder away when he places the condition before him that he'll get paid only at the end of the year. How would the employee survive the year without being paid?

Likewise, buying a great car but having little left to maintain and run it becomes a futile and meaningless act and so also would be the case when a person goes to the best university only to realize that he does not have enough to fund the entire course. An incomplete course, quite obviously has little value. There is no logical concept like half a doctor or half an engineer or three fourths a lawyer. You are either a professional or you are not.

The above examples have been explained to help one understand the difference between the Profit and Loss Statement and Cash Flow statement. While the profit and loss statement gives an indication of the operational efficiency of a business, it does not entirely reflect the cash flow of the business.

For example, if you are a sculpture and you invest 10K in materials to sculpt statues. You then sell those to a client for 20K, and make a profit of 10 K. In the P/L statement, you would record this 10 K profit even though you haven't received the money. Now the client may take up to an “X” number of days to pay you. This is one of the main differences between a P/L statement and Cash Flow statement. The P/L statement uses accrual accounting. This is when all revenues are recorded when earned, and expenses when incurred.

Now, in your sculpting business, the company may get a huge order and spend a lot of money in supplying the goods on credit, and this as a result would leave the company with inadequate amount of money for salaries. So even if the business opportunity is large, organizations should know how to manage their money. They have to understand that paying employees on time and maintenance of machines need to be given priority over simply chasing orders. This is why the cash flow statement is a reflection of a company's health, whether it is able to pay bills on time and its ability to finance growth. Simply looking at the P/L statement may not give the kind of insights, However, a P/L statement shows a thorough account of revenues and expenses and is helpful for a person to gauge the earnings per share and whether to invest in a company or not.

In the end, it is important to look at both of these statements together to get a better understanding of how the business is doing as a whole. Each statement gives vital information, and they work hand in hand. If the net income is low on the P/L statement, then invariably there is a weak cash flow and one will be able to see where the cash is being spent on the cash flow statement. Looking at these statements separately and drawing conclusions will only leave you will half the piece of the pie and leave you in situations like the ones mentioned above. (Source: Tata Mutual Fund) -

Price Band in a book built IPO

The prospectus may contain either the floor price for the securities or a price band within which the investors can bid. The spread between the floor and the cap of the price band shall not be more than 20%. In other words, it means that the cap should not be more than 120% of the floor price. The price band can have a revision and such a revision in the price band shall be widely disseminated by informing the stock exchanges, by issuing a press release and also indicating the change on the relevant website and the terminals of the trading members participating in the book building process.

In case the price band is revised, the bidding period shall be extended for a further period of three days, subject to the total bidding period not exceeding ten days. -

Prospectus

A large number of new companies float public issues. While a large number of these companies are genuine, quite a few may want to exploit the investors. Therefore, it is very important that an investor before applying for any issue identifies future potential of a company. A part of the guidelines issued by SEBI (Securities and Exchange Board of India) is the disclosure of information to the public. This disclosure includes information like the reason for raising the money, the way money is proposed to be spent, the returnexpected on the money etc. This information is in the form of ‘Prospectus’ which also includes information regarding the size of the issue, the registrars & Transfer Agents, the current status of the company, its equity capital, its current and past performance, the promoters, the project, cost of the project, means of financing, product and capacity etc. It also contains lot of mandatory information regarding underwriting and statutory compliances. This helps investors to evaluate short term and long term prospects of the company.

-

Passive Fund Management

When an investor invests in an actively managed mutual fund, he or she leaves the decision of investing to the fund manager. The fund manager is the decision maker as to which company or instrument to invest in. Sometimes such decisions may be right, rewarding the investor handsomely. However, chances are that the decisions might go wrong or may not be right all the time which can lead to substantial losses for the investor.

There are mutual funds that offer Index funds whose objective is to equal the return given by a select market index. Such funds follow a passive investment style. They do not analyse companies, markets, economic factors and then narrow down on stocks to invest in. Instead they prefer to invest in a portfolio of stocks that reflect a market index, such as the Nifty index. The returns generated by the index are the returns given by the fund. No attempt is made to try and beat the index. Research has shown that most fund managers are unable to constantly beat the market index year after year. Also it is not possible to identify which fund will beat the market index.

Therefore, there is an element of going wrong in selecting a fund to invest in. This has lead to a huge interest in passively managed funds such as Index Funds where the choice of investments is not left to the discretion of the fund manager. Index Funds hold a diversified basket of securities which represents the index while at the same time since there is not much active turnover of the portfolio the cost of managing the fund also remains low. This gives a dual advantage to the investor of having a diversified portfoliowhile at the same time having low expenses in fund. There are various passively managed funds in India today some of them are:

UTI Nifty Fund launched by Unit Trust of India in March 2000.

Franklin India Index Fund – BSE Sensex Plan launched by Franklin Templeton MutualFund in August 2001.

HDFC Index Fund - Nifty Plan launched by HDFC Mutual Fund in July 2002. -

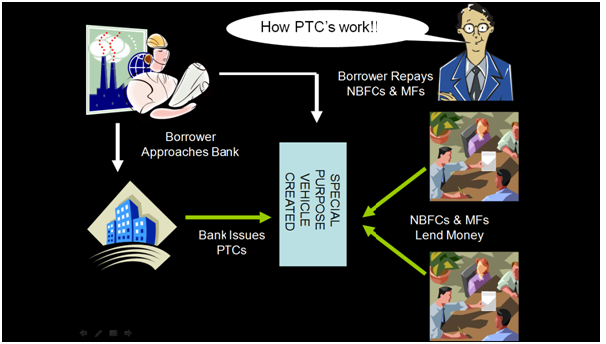

Pass through Certificates

While these are instruments for investment, there is yet another kind of paper known as ‘Pass Through Certificates’ or PTC that is issued by banks as another option.

Understanding Pass through Certificates - Pass Through Certificates (PTCs) are issued by banks as a safeguard against risks. Simply put, the banks, through PTCs, transfer some of their long term mortgaged assets (receivables) on to other investors like NBFCs and Mutual Funds.

Why do they do this? They do this because they want to share some of their risks with other players. They also do this to release capital & book profits. Investors get interested because they stand to earn more for sharing the risk.

Now, The transfer is done by means of a Special Purpose Vehicle or SPV which mediates between the investor and borrower. The PTC ensures that the loan re-payment is made to the investor instead of the bank. Thus, the borrower is accountable to the investor instead of the bank.

What happens when the borrower starts to default? If the borrower starts defaulting, the SPV sells off the mortgaged asset and recovers the money.

How PTC’s work!!

PTCs are also used to ensure that banks maintain their liquidity as per the statutory guidelines of the Reserve Bank and at the same time continue lending.

To Sum Up, Pass Through Certificates (PTCs) are instruments of investment issued by banks. It provides the bank a tool for hedging risks. They are issued when the bank feels it has too many risky assets to hold on to or when it needs additional capital for lending. The transfer is done by means of a Special Purpose Vehicle or SPV which mediates between the investor and borrower. (Source: Tata Mutual Fund) -

Price Discovery in the Stock Market

Let’s say a company makes Rs. 1000 as profit. Also, let’s assume the company has 100 shares

So earnings per share (EPS) i.e. profit/no. of shares = Rs. 1000/100 = 10. Let’s say the price per share in the market is Rs. 100. Then the P/E would be Price of share / Earnings per share 100/10 =10

Since P/E = 10, it means a buyer, Mr. Pickle is willing to pay 10 times the company’s annual earnings per share!

This means that the buyer would take 10 years to recover his cost of buying. However 10 yrs seems a long time to recover his investment. what’s his motivation for investing?

Let’s say there is a surge in the demand for the company’s product causing its profits to go up from Rs 1,000 to Rs 10,000! Now what’s interesting to observe is that while the profit went up from Rs 1000 to Rs 10,000 the number of shares remains the same at 100. Hence, by definition, earnings per share would be Rs.100.

Since Mr. Pickle invested Rs. 100 for a share whose EPS has increased from Rs 10. to Rs. 100, he is now able to recover his investment within a year.

Assuming the P/E remains at 10 and earnings per share has gone up to Rs. 100, the price of the share would then be Rs. 1000. Hence Mr Pickle who paid Rs 100 per share could sell the same for Rs. 1000 and make a profit of Rs 900.

But the story does not end here. When people see that a company, which was making Rs. 10 per share sometime back, is now making Rs. 100 per share, they all want to buy the shares of this company and thus the demand shoots up! And this demand causes the P/E to go up from 10 to let’s say 12.

When the P/E moves up from 10 to 12, the market price of the shares too moves up to Rs. 1200 from 1000.

Now Mr. Pickle, who had initially bought a share for Rs. 100, can now sell the same for Rs. 1200 and make a profit of Rs 1100!

Thus we have seen how the price of a share is discovered in the market. It is a function of both the earnings per share which is the profitability of the company as well as the sentiments, expectations of the market causing demand to rise which increases the P/E ratio!

Hopefully you’ve now understood the conceptual interpretation of the P/E ratio and how it changes depending on earnings of the company at one hand and demand on the other! (Source: Tata Mutual Fund)

Recent Articles

Top Performing Mutual Funds

Tools and Calculators