Financial Glossary starting with Alphabet O

-

Opportunity Cost

Let's consider that an organization is throwing a party to celebrate the launch of a product. The organization decides that they will invite a celebrity to perform. She quotes Rs 5 lacs for the evening.

The boss is livid with the organizers chiding them for their poor negotiation skills. His contention is that if the cost of the party is Rs 5 lacs, how can the celebrity alone demand an equal amount? To refute the boss's allegation, the organizer explains that the celebrity charges Rs 6 lacs for a weekend performance charges Rs 6 lacs.

He also claims that he could make the boss talk to some of the organizations who have had to cough up such amounts for the services of the celebrity in question.

So in keeping with this explanation, the organizer explains that the celebrity is actually forgoing Rs 1 lac by choosing to perform with them and letting go of other opportunities that would fetch the celebrity Rs 6 lacs instead of the Rs 5 lacs that she has quoted to perform in this party.

Thus the opportunity cost is the difference in the amount that she could earn had she taken up another assignment against the one that she has chosen. In short, the celebrity is letting go an opportunity that could earn her an extra Rs 1 lac. The boss kept mulling over what was said and it was not easy to gather whether he was convinced with the argument.

Whether the boss was satisfied or not is hard to say but we hope you have understood the concept of “Opportunity Cost” by way of this explanation. (Source: Tata Mutual Fund) -

Options Contract

Let’s look at the same example for the farmer & bread manufacturer as we did in our lesson on “Futures”.

So let’s say there’s a farmer who cultivates wheat And a bread manufacturer who needs wheat as an input for making bread.

The farmer thinks that the price of wheat which is currently trading at Rs. 100 could fall to Rs. 90 in 3 months. The bread manufacturer on the other hand feels that the price of wheat on the other hand might become Rs. 120 in 3 months.

In such a case both of them get together and sign a contract which says that at the end of 3 months the farmer would sell wheat to the bread manufacturer at Rs. 110. Thus the farmer is protected against possible fall in prices. And the bread manufacturer is protected against the price of wheat, a key ingredient in bread manufacturing to go up beyond Rs. 110.

Such a contract is called a Futures contract as we saw in our lesson on “Futures”. In a Futures contract both parties are obliged to honor the contract and there is no escape route for either party

But what if the contract gives the farmer the “option” of either 1) Selling his produce to the bread manufacturer at the pre-agreed price of Rs. 110 or 2) Choosing to exit the contract and selling the produce in the open market or wherever he deems fit.

Thus, he would not be obliged to honor the contract made with the bread manufacturer on the date of settlement.

Such a contract which gives the farmer the option of either executing the contract or exiting it is known as an “Options” contract

But the farmer obviously cannot get this privilege just like that. He obviously has to pay a premium for exercising this facility. Now, let’s say that after 3 months the price of wheat reaches Rs. 120

In this case the farmer quite obviously will want to exit the contract so that he is free to sell his produce in the open market for Rs. 120. Thus while the farmer gets away the bread manufacturer is left high and dry and has no other option but to buy from the open market at Rs 120.

But it is not such a bad situation for the bread manufacturer as it appears as he gets compensated by the farmer for having been a party to the “Options” contract. This compensation * in the form of price is called the “Option premium” that the farmer has to pay for the Options contract and quite evidently it would be a small amount.

Let’s say in our case the amount is Rs 2. So the farmer is obliged to pay the bread manufacturer Rs 2 as he has chosen to opt out of the contract.

Thus although the bread manufacturer has no other option left but to go to the open market and purchase wheat at Rs. 120, he does get the benefit of Rs 2 as compensation for being a party to the “Options” contract. So even if the price is Rs. 120 in the open market, for him the effective price turns out to be Rs. (120 -2) = Rs 118.

So by simply participating in the contract he too stands to gain something. As far as the farmer is concerned it is a win – win scenario for him by participating in the contract.

Had the prices fallen to Rs 90 as he had anticipated he would have executed the Options contract. But since prices rose to Rs 120 he chose to exit the contract. Thus he is blessed with the “Option” by signing such a contract.

It is important to understand that in an “Options” contract only one party gets the privilege to exercise the option while the other party is obliged to honor the option chosen.

Thus in our case the farmer has the option to either execute or exit the contract whereas the bread manufacturer is obliged to honor the decision of the farmer. A contract such as this where only the seller of the commodity gets the option to either exercise or exit the contract is known as “Put” option.

There is another option which is called a “Call” option and we will explain that concept later.

Even in an Options contract both parties land up achieving their goals and their interest is protected. The farmer stands to gain the most by getting to exercise a choice that benefits him the most.

The bread manufacturer too benefits by being a party to the contract due to the compensation he receives from the farmer for not honoring the contract. The bread manufacturer due to the compensation receives wheat from the open market at an effective price of Rs 118.

And hence is better off than the ordinary or spot buyer who would have to pay Rs 120. Thus in a sense both parties landed up getting some gains by being parties to the “options contract”.

However unlike in a “Futures” contract, in the “Options” contract one party gains more than the other party. (Source: Tata Mutual Fund) -

Open Market Operations

If one were to read articles in ET on monetary policy and macro-economic development, one often comes across a term called ‘OMO’. So what is ‘OMO’?

While OMO is a famous detergent brand from Unilever, the ‘OMO’ we are talking about is something very different.

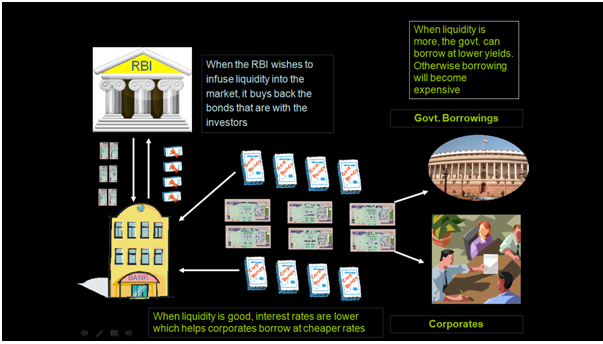

First of all One must understand that when there is excess liquidity in the market, the RBI intervenes and sucks it by issuing bonds, among other means. At the same time, if the liquidity starts to dry up in the markets, the RBI intervenes once again and infuses liquidity by buying back the bonds that are with the investors.

What’s ‘OMO’ then? This interaction of the RBI with the market is termed ‘OMO’ or ‘Open Market Operations’.

What is the outcome on account of OMO?

When the RBI buys bonds from the market and infuses liquidity, the consequences are:

• It tends to soften the interest rates

• Fresh bonds can be issued at lower yields and the government can thus borrow at a reasonable cost

• It enables corporates to borrow at favorable interest rates

• It prevents the rupee from strengthening unnecessarily and thereby protects the interest of exporters

• It may tend to increase inflation

Consequently If the RBI were to sell bonds instead and suck in liquidity, the effect would exactly be the opposite!! Thus OMOs’ are an important instrument of credit control through which the Reserve Bank of India purchases and sells securities.

To Sum Up, Open Market Operations (OMOs) are the means of implementing monetary policy by which a central bank controls the nation’s money supply by buying and selling government securities, or other financial instruments. It helps regulate interest rates and foreign exchange rates. (Source: Tata Mutual Fund) -

Off-Balance Sheets

An Off-Balance Sheet (OBS) usually means an asset or debt or financing activity that is not reflecting on a company's balance sheet. In other words, it is a form of financing in which large capital expenditures are kept off a company's balance sheet through various classification methods.

Companies will often use off-balance sheet financing to keep their debt to equity (D/E) ratios low, especially if the inclusion of a large expenditure would give them a negative debt to equity ratio.

So what is the difference between an on & off balance sheet?

The formal accounting distinction between on and off-balance sheet items can be quite detailed and will depend to some degree on management judgments.

But in general terms, an item should appear on the company's balance sheet if it is an asset or liability formally owned by the company or if the company is legally responsible for it. Uncertain assets or liabilities must also meet tests of being probable, measurable and meaningful.

For Example, Say Company A has a subsidiary company B & it offloads all its risky investments in it. Now, any potential losses of the subsidiary company do not reflect in the books of records of the parent company. This helps A to appear financially more stable in the eyes of the public.

But it also becomes responsible for any losses that arise in company B. This however is something the public doesn’t know.

What company A does is that it puts the risky ventures of its subsidiary company B & any resulting payment/ expenses/losses out of its balance sheet and appears more healthy.

Companies have used off-balance sheet entities responsibly and irresponsibly for some time. These separate legal entities were permissible under tax laws so that companies could finance business ventures by transferring the risk of these ventures from the parent to the off-balance-sheet subsidiary.

Now, this was also helpful to investors who did not want to invest in these other ventures. Since the Enron scandal, however, General Accepted Accounting Principles (GAAP) allow these items, whether justifiable or not, to be excluded from the parent's financial statements but usually they must be described in footnotes.

Giving you another example of Oil Bonds. Oil bonds are paid by the Govt. to oil companies to fund the subsidy on petroleum products. Now, a bond is a promise to pay at a later date. Thus, although the oil cos. are paying money upfront for purchases, they are being compensated by means of oil bonds which are a deferred payment.

Also, Besides the oil companies’ losses, the Govt. too has to pay up the money at the end of the stipulated time period which often could be a few years later. Thus, what these bonds are doing is just postponing the losses, which have to be repaid some day. And somewhere, at some point in time, the promised doles met out earlier will also eat into the Govt’s revenues, thus adding to the fiscal deficit.

But here’s the catch, did you know that the Govt. does NOT incorporate oil bonds in its balance sheets?

What this means is that while the Govt. is liable to pay oil companies at some point in time but this is not reflected in its books of accounts. Simply put, in contrast to loans, debt and equity; the oil bonds do not appear on the balance sheet for the current year as they are future liabilities. This makes the balance sheet appear healthier.

To Sum Up, An Off Balance Sheet (OBS) usually means an asset or debt or financing activity that is not reflecting on a company's balance sheet. It was permissible under tax laws so that companies could finance business ventures by transferring the risk of these ventures from the parent to the off-balance-sheet subsidiary. Tax laws allow these items to be excluded from the parent's financial statements but usually they must be described in footnotes. -

Off-Balance Sheets

An Off-Balance Sheet (OBS) usually means an asset or debt or financing activity that is not reflecting on a company's balance sheet. In other words, it is a form of financing in which large capital expenditures are kept off a company's balance sheet through various classification methods.

Companies will often use off-balance sheet financing to keep their debt to equity (D/E) ratios low, especially if the inclusion of a large expenditure would give them a negative debt to equity ratio.

So what is the difference between an on & off balance sheet?

The formal accounting distinction between on and off-balance sheet items can be quite detailed and will depend to some degree on management judgments.

But in general terms, an item should appear on the company's balance sheet if it is an asset or liability formally owned by the company or if the company is legally responsible for it. Uncertain assets or liabilities must also meet tests of being probable, measurable and meaningful.

For Example, Say Company A has a subsidiary company B & it offloads all its risky investments in it. Now, any potential losses of the subsidiary company do not reflect in the books of records of the parent company. This helps A to appear financially more stable in the eyes of the public.

But it also becomes responsible for any losses that arise in company B. This however is something the public doesn’t know.

What company A does is that it puts the risky ventures of its subsidiary company B & any resulting payment/ expenses/losses out of its balance sheet and appears more healthy.

Companies have used off-balance sheet entities responsibly and irresponsibly for some time. These separate legal entities were permissible under tax laws so that companies could finance business ventures by transferring the risk of these ventures from the parent to the off-balance-sheet subsidiary.

Now, this was also helpful to investors who did not want to invest in these other ventures. Since the Enron scandal, however, General Accepted Accounting Principles (GAAP) allow these items, whether justifiable or not, to be excluded from the parent's financial statements but usually they must be described in footnotes.

Giving you another example of Oil Bonds. Oil bonds are paid by the Govt. to oil companies to fund the subsidy on petroleum products. Now, a bond is a promise to pay at a later date. Thus, although the oil cos. are paying money upfront for purchases, they are being compensated by means of oil bonds which are a deferred payment.

Also, Besides the oil companies’ losses, the Govt. too has to pay up the money at the end of the stipulated time period which often could be a few years later. Thus, what these bonds are doing is just postponing the losses, which have to be repaid some day. And somewhere, at some point in time, the promised doles met out earlier will also eat into the Govt’s revenues, thus adding to the fiscal deficit.

But here’s the catch, did you know that the Govt. does NOT incorporate oil bonds in its balance sheets?

What this means is that while the Govt. is liable to pay oil companies at some point in time but this is not reflected in its books of accounts. Simply put, in contrast to loans, debt and equity; the oil bonds do not appear on the balance sheet for the current year as they are future liabilities. This makes the balance sheet appear healthier. -

Organic Growth & Inorganic Growth

Let’s imagine there is a “bhelpuriwala” who has a stall in a famous market place. He has been in this business for long and has quite a reputation. He sells “Bhel” under the brand “Golden Snacks”

With time as his business starts growing. He soon has money to stock other products. So he introduces Sev Puri, Dahi Puri, Delhi Chaat etc under the “Golden Snacks” banner. The addition of new products gives further impetus to his business. This kind of growth is what we typically call, “Organic” growth. It is growth that comes from within the same business

As time goes by and his business grows further, he starts accumulating a lot of money. With all the money at his disposal, he gets more ambitious and wants to invest the money in his business to make it grow even faster. But he realizes that even if he invests the money it would not be possible to grow the business from within in short time span. So he starts to think of another approach to attain quick growth

He hits upon another idea. He purchases four new snack shops in the same area lock stock and barrel and brings them all under the “Golden Snacks” banner. Such growth which can be purchased and which is essentially from the outside is known as “inorganic” growth.

Hope this lesson has succeeded in clarifying the difference between Organic and Inorganic Growth (Source: TATA Mutual Fund)

Recent Articles

Top Performing Mutual Funds

Tools and Calculators