Financial Glossary starting with Alphabet I

-

Imported Inflation

We have often heard our parents or grandparents saying that they used to manage the entire house for 100 rupees a month in those days. We usually smirk, and say Gone are those days. Today we can’t even have one full meal in 100 rupees.

Blame it on inflation. Inflation erodes the purchasing power of money such that Rs. 100 today is no longer Rs. 100 tomorrow. We understand inflation, but what does imported inflation mean?

When the general price level rises in a country because of the rise in prices of imported commodities, inflation is termed as imported.

No country in the world is self-sufficient by itself. Each country depends on other countries for goods and services which are not produced domestically.For Instance, India imports about three quarters of its total crude oil consumption. Therefore, if oil prices go up in the international market, inflation in India will also go up due to higher prices of the petroleum products as fuel and power have 14.91% weightage in the Wholesale Price Index (WPI) in India.

However, it is not necessary that only rise in the price of a traded commodity in the international market fuels imported inflation. Inflation may also rise because of depreciation of the domestic currency.

For example, if the rupee depreciates by 15% against the US dollar in a particular period, the landed rupee cost of oil will also go up by a similar proportion and will affect the price and inflation numbers.

Let us consider an example. Suppose we import Petrol at $100 a unit. And the exchange rate is Rs. 50 per dollar. This means we actually need Rs. 5,000 to first buy $100, and then pay for the Petrol purchase of one unit. Therefore the price of Petrol depends on two factors:

1) Price of Petrol (in dollar terms) 2) Price of the dollar.

As explained above, price of petrol in India is directly proportional to the price of petrol in dollars, but also is impacted by the price of the dollar. Let’s understand how.

Suppose the price of the dollar goes up to Rs. 60 per dollar. This means that we will have to cough up Rs. 6,000 to buy $100 for the purchase of one unit of Petrol. So despite the fact that the price of Petrol continues to be stable in the international market at $100, the price of Petrol in India goes up from Rs. 5000 per unit to Rs. 6000 per unit. So while there is 0% increase in the price of petrol in the international market, the price of petrol in India increases by 20%.

Therefore one often reads that the devaluation of the rupee will bring in imported inflation.

Hope the above explanation helped you to understand the concept of imported inflation as against domestic inflation. (Source: Tata Mutual Fund) -

Income & Spending : From the Keynesian perspective

- An individual can choose to increase his savings by curbing his spending. This would certainly make his finances appear better. But when it comes to the economy, the scenario changes - “My spending is Your income and Your spending is My income”. If we BOTH slash spending, BOTH our incomes will fall. Therefore a carte blanche “austerity” order often fails to provide expected results. Let us see how and why this happens.

- In an austerity drive, people have to cut spending, either because they chose to or because their creditors force them to. The willingness of people to spend starts to wane. For the economy, every consumer is also a producer (working in some place or perhaps running his own business). Therefore while he may spend less and save more, he may earn less because others like him are too not willing to spend to buy his produce. The result is depressed incomes and a depressed economy, with millions of willing workers unable to find jobs.

- Under such circumstances, “government spending” can bail the economy out of a tight spot. The government is not in competition with the private sector. Government borrowing doesn’t crowd out private borrowing; it puts idle funds to work. If the government cuts spending, the economy will shrink and unemployment will rise. In fact, even private spending will shrink, because of falling incomes.

- This is perhaps the reason why budget deficits have not led to soaring interest rates and the Fed's money-printing hasn’t led to inflation;

- Austerity policies have greatly deepened economic slumps almost everywhere they have been tried.

- Yes, the government must pay its bills in the long run. But spending cuts and/or tax increases should wait until the economy is no longer depressed, and the private sector is willing to spend enough to produce full employment.

- Let us take an example. It is not right to drive a Mercedes or BMW if you cannot afford it. Buying the same on borrowed money may send you into a debt trap. Perhaps buying a Maruti Alto or a Hyundai i20 might be a better solution. But it is necessary that you drive a car, burn petrol while travelling to different places, shop for goods or spend at restaurants and buy gifts for those who we visit. However if the car “stalls”, the demand for petrol and consumables falls along with other goods and services. Hence it is important that the car keeps moving.

- You can’t kill a slowdown by another slowdown. So get up and move on. This is the only medicine for reversing the detrimental effects of a slowdown. (Source: Tata Mutual Fund)

-

Inflation - Core and Headline Inflation

John is assigned the job of a coach of the school cricket team. For the next few days, he ascertains the strength and weakness of each player. He realizes that there is one player in the team called Sam whose performance is very erratic. Though talented, he experiences severe mood swings. On certain days when he is charged up, his performance is exceptional and he can change the outcome of a match. However, on other days when his game is lackluster, the team’s performance is markedly mediocre.

While John does not like the mood swings of his key player, he has to select him most of the time because of his exceptional skills. However, when asked by the school board about the overall performance of the team, he chooses to exclude Sam while calculating team’s performance as a whole. This is because the volatility of his performance would paint an incorrect picture about the performance of the team as a whole. In a good quarter when Sam has been at his best, the overall performance of the team would look brilliant while in another quarter where Sam was lackluster, it could look dismal.

Headline inflation and Core inflation are two concepts which are very similar to the above situation. While Headline inflation judges the increase in prices over a year of a basket of goods, this basket contains products which are like Sam i.e. volatile in terms of their individual prices. So to get a better understanding of inflation, just as John removed Sam for the purpose of calculating team’s performance, similarly, volatile products are removed from the basket that determines Headline Inflation. And once these volatile products are removed, the remaining products give a better estimate of the overall inflation trend in the country. This is known as Core Inflation. Crude oil is one such product which displays price swings based on global economic conditions that are beyond the control of local policymakers. (Source: Tata Mutual Fund) -

Inflation why it is not always bad

Why would somebody want inflation?

Ask an Indian and he will want to stare you into ashes.

But ask a Japanese and he is all likely to smile back at you and seek suggestions.

Thus inflation may be a bad word for us in India where everybody seems to be fighting inflation. We call it all sorts of names like ghost or monster.

But elsewhere inflation is not necessarily a bad omen.

In fact “inflation” is the rally cry in Japan to reverse the economy from the brink of coming to a standstill and going nowhere.

To understand this it is imperative to see “inflation” as a dividing wall between consumers on one side and manufacturer on the other side.

The consumers always want the wall to be short so that they can easily climb up and enter the manufacturing side and use the goods and services without much effort. For the sake of analogy consider “effort” equal to “money” & “wall” to “inflation”, let us use it interchangeably. Therefore for consumers a shorter wall means lower prices.

But the manufacturers on the other side think exactly the opposite. They would like the consumer to spend more money in climbing the wall before they can enter the manufacturing side and consume goods and services. Thus a taller wall for the manufacturer means more money and profits. Thus high inflation or a tall wall is more acceptable to the manufacturer as compared to the consumer while low inflation or negative inflation might be acceptable to the consumer but is a worrying sign for the manufacturer.

However the story does not end there.

One needs to also understand that every consumer is also a producer or connected with a producer somewhere or the other. So while cheap goods makes him happy when he goes for shopping with his family, the same low cost of products that his company produces has become a pain for him at work.

Because of less demand for the products that his company makes, the prices are low and so are the profits.

As a result the company makes less money, gives a small salary and defers increments and bonus. In the absence of less money even low prices in the market does not entice him to spend much. This further impact the market and prices keep falling because of weak demand.

This is how the situation in Japan has been for some time. However, now the government wants to change the mood of the people by providing easy money in their hands.

This is called Quantitative Easing which is similar to say printing money.

What is the effect of this move?

1. It brings the value of the Yen down. This immediately makes Japanese exports more lucrative and creates demands for Japanese goods in the international market.

2. As consumers have more money and willingness to spend on goods and services, inflation rises resulting into depreciated purchasing power of money. This will also lead the consumers to prepone their purchases.

3. More demand for the goods will mean that factories will invest more in capacity building which itself is a demand engine for raw material and labor.

4. Companies will hire more people to meet the increased demand.

5. The companies would pay higher wages to ensure that people work hard and keep pace with demand.

6. Money in the hands of the people through better increments and bonus etc means more domestic demand.

This is what the Japanese PM Shinzo Abe would like to believe and is hence formulating policies accordingly.

He believes that if parents were to increase the pocket money of children, then surely the children will start consuming more of all the goodies like ice cream, candies, toys, books etc. And the manufacturers of these goods would make more of these products, buy raw material and hire more people to make them. The raw material maker too would hire more people to supply more raw material and so on and so forth.

The increased domestic and international demand would increase the share prices of the manufacturing companies and we are seeing this play out in Japan.

More international money would move into Japan to take advantage of this growth opportunity. We are seeing this as well today.

Investors would sell out other asset classes in favor of Japanese equity. The drop in gold and commodity prices is a symptomatic of these policy changes.

All this activity is expected to re-invigorate the Japanese economy and propel it to a growth trajectory.

However the downside of this initiative is to ensure that inflation does not spiral out of control and begin the dampening the demand cycle.

Shinzo Abe believes he can ensure a smooth take off for the Japanese economy through his actions and policy decisions.

This mechanism is known as Abenomics, a term coined after the name of the Prime Minister Mr. Shinzo Abe.

In economics such an activity whereby the government tries to re-energize the economy by inducing inflation is known as “reflation”. (Source: Tata Mutual Fund) -

Investment

The money you earn is partly spent and the rest saved for meeting future expenses. Instead of keeping the savings idle you may like to use savings in order to get return on it in the future. This is called Investment.

One needs to invest to:- earn return on your idle resources

- generate a specified sum of money for a specific goal in life

- make a provision for an uncertain future

One of the important reasons why one needs to invest wisely is to meet the cost of Inflation. Inflation is the rate at which the cost of living increases. The cost of living is simply what it costs to buy the goods and services you need to live. Inflation causes money to lose value because it will not buy the same amount of a goods or a service in the future as it does now or did in the past. For example, if there was a 6% inflation rate for the next 20 years, a Rs. 100 purchase today would cost Rs. 321 in 20 years. This is why it is important to consider inflation as a factor in any long-term investment

strategy. Remember to look at an investment\'s \'real\' rate of return, which is the return after inflation. The aim of investments should be to provide a return above the inflation rate to ensure that the investment does not decrease in value. For example, if the annual inflation rate is 6%, then the investment will need to earn more than 6% to ensure it increases in value. If the after-tax return on your investment is less than the inflation rate, then your assets have actually decreased in value; that is, they won\'t buy as much today as they did last year.

-

Interest

When we borrow money, we are expected to pay for using it – this is known as Interest. Interest is an amount charged to the borrower for the privilege of using the lender’s money. Similarly we receive Interest when we invest some money in a fixed instrument.

Interest is usually calculated as a percentage of the principal balance (the amount of money borrowed or invested) using one of the two methods: Simple Interest or Compound Interest. The percentage rate could either be fixed may be fixed for the life of the loan, or it may be variable or floating, depending on the terms of the loan or Investment.

Interest can also be defined as ‘significant’ etc. For Example – If someone who holds more than 5% of the shares in a company could be said to have holding ‘significant interest’ in that company. -

ISIN

ISIN (International Securities Identification Number) is a unique identification number for a security. The ISIN standard is used worldwide to identify specific securities such as bonds, stocks (common and preferred), futures, warrant, rights, trusts, commercial paper and options. ISINs are assigned to securities to facilitate unambiguous clearing and settlement procedures. They are composed of a 12-digit alphanumeric code. For example the ISIN No. of TATA STEEL LTD. is INE081A01012.

To See complete directory of ISIN numbers of Listed Indian Securities, click http://www.sebi.gov.in/isin/isin.html And for International Securities click http://www.isin.org/ -

Interest Rates - How it Works

You're watching the news and they're talking about a recent announcement from RBI, in which it is hinted that the interest rates may be raised in the next week. The stock market drops the next day. Why?

How Do Interest Rates Work?

Before you get all worked up, you should know that interest rates aren't evil. They're the price of living in a world that relies heavily on credit and debt. If interest rates didn't exist, lenders would have no reason to let you borrow money.

And if you couldn't borrow money, you could never buy a house or a car, or enjoy many of the other advantages of life with credit, like buying air tickets and paying bills online with a credit card.

So if interest rates are so important, how do they work?

An interest rate is the cost of borrowing money. A borrower pays interest for the ability to spend money now, rather than wait until he's saved the same amount.

For example, if you borrow `100 at an annual interest rate of five percent, at the end of the year you'll owe `105. But interest rates aren't just random punishments for borrowing money. The interest a lender receives is his compensation for taking a risk.

How? With every loan, there's a risk that the borrower won't be able to pay it back. The higher the risk that the borrower might default (or fail to repay the loan), the higher the interest rate.

That's why maintaining a good credit score will help lower the interest rates offered to you by lenders.

The nice thing is that interest rates work both ways. Banks, governments and other large financial institutions need cash too, and they're willing to pay for it.

If you put money into a savings account at a bank, the bank will pay you interest for the temporary use of that money.

Governments sell bonds and other securities for the same reason. In this case, you're the lender to the government and the interest rate is your compensation for temporarily giving up the ability to spend your cash.

But remember, savings accounts and government-issued bonds pay relatively low interest rates because the risk of their defaulting is close to zero.

You should also know that interest rates for unsecured credit will always be higher than secured credit. Secured credit is backed by collateral. A home loan is a classic example of secured credit, because if the borrower defaults on the loan, the bank can always take the house.

Credit cards are unsecured credit, because there's no collateral backing the loan, only the cardholder's credit score.

Long-term loans also carry higher interest rates than short-term loans, because the more time a borrower has to pay back a loan, the more time there is for things to possibly go bad financially, causing the borrower to default.

Another factor that makes long-term loans less attractive to lenders -- and therefore raises long-term interest rates -- is inflation.

In a healthy economy, inflation almost always rises, meaning the same rupee amount today is worth less five years from now. Lenders know that the longer it takes the borrower to pay back a loan, the less that money is going to be worth.

That's why interest rates are actually calculated as two different values: the nominal rate and the real rate.

The nominal rate is the interest rate set by the lending institution. The real rate is the nominal rate minus the rate of inflation.

For example, if you take out a home loan with a nominal interest rate of 10 percent, but the annual rate of inflation is four percent, then the bank is only really collecting six percent on the loan.

So how do interest rates affect the rise and fall of inflation? Well, lower interest rates put more borrowing power in the hands of consumers. And when consumers spend more, the economy grows, naturally creating inflation.

If the RBI decides that the economy is growing too fast-that demand will greatly outpace supply-then it can raise interest rates, slowing the amount of cash entering the economy. So there must be enough economic growth to keep wages up and unemployment low, but not too much growth that it leads to dangerously high inflation. (Source: Tata Mutual Fund) -

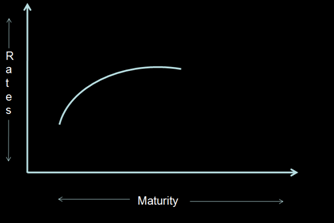

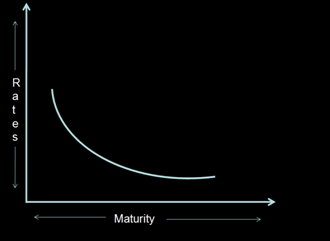

Inverted Yield Curve

The "Yield Curve” is a graphical representation of interest rates on securities of different maturities ranging from short to longest tenure bonds as presented in the next slide

This is how the “Normal Yield Curve” typically looks like.

In a typical yield curve scenario a lender would charge lesser interest if he lends for a smaller time period and higher interest for a longer term loan. Naturally if he is lending for a longer period he is taking a bigger risk because he is not too sure what would be the state of the borrower over a longer term.

However over the shorter term he would not mind charging a smaller rate of interest because he would feel more confident of the state of the borrower in the short run.

So what is an “Inverted Yield curve”?

As seen in the diagram, an inverted Yield Curve is nothing but a representation of a specific scenario in the market where the short term interest rates are higher than the long term interest rates. But then why does this happen?

This happens due to a tight liquidity environment when money supply is inadequate. For example - Sometimes organizations have to borrow at a high cost to meet their working capital needs to support their operating expenses which is vital for the day to day running of an organization.

Hence in moments of tight liquidity when companies need money badly to run their operations they are open to pay higher in the short run than what is prevailing for long term borrowing. It is the urgent need of the hour that prevails of long term strategic need.

Another reason that can be attributed to the inverted shape of the Yield Curve is the pessimistic expectation of the economy in the medium to long term. If people feel that the policies of the government will be unable to push growth then the propensity for long term investments reduce which brings down the demand for long term borrowing which in turn brings down the long term rate of interest.

However these kind of situations ease out over a period of time as liquidity and expectations improve and the “Inverted Yield Curve” reverts to its original state to become a ‘Normal Yield Curve’. This is known as “Steepening” of the Yield Curve. (Source: Tata Mutual Fund) -

Index Funds

An index fund is a portfolio constituted of stocks belonging to some market index such as the Sensex or Nifty. You can invest in an index fund either through a mutual fund or an exchange-traded fund (ETF).

Now the Sensex, as you may be aware, consists of 30 stocks in proportion to their free-float market capitalization. Likewise, the Nifty consists of 50 stocks in proportion to their free-float market capitalization.

These stock market indices help us in gauging the overall mood of the market because they capture the price movements of the majority of stocks by market capitalization belonging to different sectors. An index fund tries to track a particular index by including all stocks belonging to that index in its portfolio in exactly the same proportion as used by that index.

Okay, but how does it work?

Say, for instance, if one particular stock has a weightage of 10.86% on the Nifty, then an index fund tracking the Nifty would use 10.86% of its funds to buy that particular stock.

If another stock has a weightage of 8%, then the index fund would allocate 8% of its funds for buying that stock. The end result is that you have a diversified portfolio, consisting of some of the best known firms, and your portfolio mimics the rise or fall of the chosen index.

What are the other advantages of an index fund?

The main advantage of an index fund lies in its cost.

Since index funds require only passive fund management, they are much cheaper than more actively managed funds in which portfolio managers make an effort to choose the right stock.

The expense ratio, which represents the value of total expenses as a percentage of the value of total assets under management, of most of the index funds in India is usually less than that of more actively managed funds.

What about its disadvantages?

One of the drawback which some of the index funds suffer is in the form of tracking errors. Theoretically, the return produced by an index fund should closely mimic the rise or fall of the concerned index.

But in reality, due to what we call tracking errors, the fund may sometimes generate a return higher or lower than the actual movement in the index. Tracking errors could happen due to a variety of reasons. Let me quickly tell you about some of them…

First, some discrepancies might creep in at the time of allocation of funds itself, leading to greater or lower allocation of funds in different stocks.

Second, any change in the composition or weightage of the index requires rebalancing of the portfolio by the fund manager, which increases further the scope for discrepancies.

Third, it is often difficult for fund managers to trade at the market closing price, which means that the final value of the index and the value of the index fund portfolio on that day might show some difference.

Finally, the fund managers may have to keep some cash ready to take care of redemptions by investors. Spare cash reduces the overall return of the fund.

To Sum Up, an index fund tries to track a particular index so that its returns mimic the rise or fall of that specific index. An index fund includes all the stocks of a particular index in its portfolio in exactly the same proportion as used by the index. Index funds are popular due to lower expenses and better performance. (Source: Tata Mutual Fund)

Recent Articles

Top Performing Mutual Funds

Tools and Calculators