Financial Planning in Fantastic Fifties

Welcome back! Hope you enjoyed the last three articles of this 5 part series Financial Planning in the Tantalizing Twenties, Financial Planning in the Thrilling Thirties and Financial Planning in Formidable Forties.

Fifties is an interesting decade as you slow down and prepare for a life of retirement. This decade is the most fulfilling decade as you have amassed respectability in your profession. In your personal life your kids may have already set out on their own ways or are financially independent redeeming you of their responsibilities. Fifties also happens to be the last decade before you settle for your retirement. Hence, this is the last time you give a final push towards your retirement corpus. You maybe are dreading your retirement, apprehensive of the decade that follows the fifties marking the end of your job life. However, the pile of assets that you have created in your working life will be your pillar in your retired life cushioning you with the same sense of security. Here is how you can make the fantastic fifties work for you:

Have Adequate Life Insurance and Health Insurance Cover

In the earlier decades your life insurance covered your spouse, your kids and dependents. However, if you kids and dependents have become financially independent then financially you are no longer responsible for their well being. Hence, your life insurance cover should be adequate to cover you and your spouse in case of any unforeseen calamities. The reduction in the life insurance cover can be adjusted with the health insurance cover as with the age your health insurance cover should ideally increase. You are now prone to diseases because of ageing and medical bills which burn a hole in your pocket could be financially fatal. Hence, having adequate health insurance cover takes care of any health downfall without causing any financial stress.

Clear all Debts

You will not be able to utilize the assets fully if they are not debt free. Hence, by the end of this decade it would be an ideal scenario if all your debts are asset free. Home loan, car loan, personal and education loan should be totally paid off so that the last innings of your income is largely utilized consolidation of your savings and investments. Having a loan which might get carried forward to the next decade could eat into your retirement corpus which is meant for your living expenses.

Do Not Take Any New Loans

The concept of taking loan is borrowing money not just from any institution but from your future income as well. A loan when it is taken, it is with the assumption that the future income will be sufficient to cover the debt. Hence, a repayment of the loan usually occurs from a regular income. Post retirement one has to rely more on fixed income than on regular income. Taking a loan with in such a financial scenario erodes the fixed income and could be financially fatal.

Start Tapping Your Assets

To simply define, assets are those purchases or investments could provide a lump sum or steady income to the owners. In your 50s when you are planning for your retirement, it may not be a wise idea to manage all your expenses through fixed income. If you have a property which is lying empty then you are not utilizing your asset to the maximum possible extent. If the property could earn inflation adjusted returns then it could be a regular income in the future. If you are planning to make further investments, you are probably confused between a bungalow in the outskirts of the city and an apartment in the heart of the city. A bungalow in the outskirts of the city may have future value but to get immediate returns in the form of rent, an apartment in the heart of the city may be a wise investment. Any asset that might depreciate in the future like a car should be purchased while you were steadily earning.

Having a Moderate but not Indulgent Lifestyle

Lifestyle is the nitty-gritty of our personal living and largely entails how we treat ourselves, our family and people around us. A hefty part of your regular income is utilized in maintaining the embraced lifestyle. The retirement corpus that you have been creating has been done keeping in mind the future cost of such a lifestyle. In your 50s you have to maintain the same lifestyle. Suddenly, if you start living an indulgent lifestyle and plan to continue this then it puts extra pressure on your corpus. You need to start making extra provisions with your income to entail this sudden indulgence. Hence, it is best if you maintain the lifestyle that you have been following to manage within the current regular income and future fixed income.

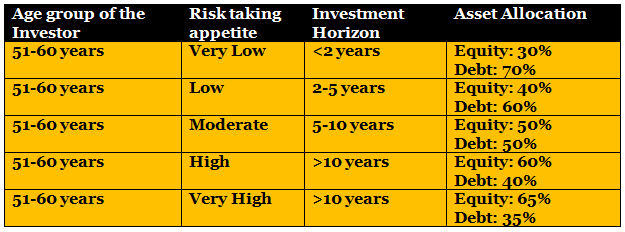

Balancing the Portfolio

With every passing decade it becomes essential to rebalance your investments. This ensures that your investments are attuned to your goals. The various goals in your 50s could be aggressively investing in retirement funds, investing in assets with steady returns, generating returns by avoiding volatility and so on. The closer you get to retirement you are looking for stability in your investments. Let us see some possible asset allocation for your investments.

Be Willing to Make Your Will

We all hope and pray for long lasting lives but you can save your family from a lot of trouble by drafting your will. Having a will gives you a comprehensive picture of all your assets and investments. In case you are incapable of making financial decision due to health reasons or sudden unavailability the nominees will be able to make financial decisions on your behalf. You will also be relieved that the beneficiaries will receive the assets that you have earmarked for them. You can keep making occasional changes to your will as and when assets are increased or due to the changing circumstances in your family.

Conclusion

You are about to embark in your fifties hoping to making it a fulfilling decade. Retirement which often felt like a goal far away in the horizon is palpably present now. Enjoy this decade as you will have more than enough time to pursue all the hobbies that you left behind to get ahead in life. So go ahead and enjoy this amazing decade because life from here on gets even better. Remember, the financial advisor, based on whose advise you have planned and achieved your financial goals so far, should continue to be your friend in your fifties as well.

Queries

-

What is the benefit of mutual fund STP

Aug 29, 2019

-

How much to invest to meet target amount of Rs 2 Crores

Aug 26, 2019

-

Can I achieve my financial goals with my current mutual fund investments

Aug 24, 2019

-

Can you tell me return of various indices

Aug 19, 2019

-

What would be the post tax return on different investments

Aug 18, 2019

-

Which Principal Mutual Fund scheme will be suitable for my retirement corpus

Aug 16, 2019

-

What is the minimum holding period for availing NCD interest

Aug 4, 2019

Top Performing Mutual Funds

Recommended Reading

Fund News

-

SBI Mutual Fund SIF launches Magnum Equity Ex Top 100 Long Short Fund

Aug 7, 2026 by Advisorkhoj Team

-

Axis Mutual Fund launches Axis Nifty Energy Index Fund

Aug 7, 2026 by Advisorkhoj Team

-

Kotak Mahindra Mutual Fund launches Kotak Diversified Equity All Cap Omni FOF

Aug 5, 2026 by Advisorkhoj Team

-

Franklin Templeton Mutual Fund launches Franklin India Short Term Fund

Aug 5, 2026 by Advisorkhoj Team

-

Edelweiss Mutual Fund launches Edelweiss Nifty REITs and Realty Index Fund

Aug 5, 2026 by Advisorkhoj Team